ANZ Macro Daily(Beta Mode)

AUD Slides Ahead of RBA Minutes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,764.20 | +0.18% |

| NZX 50 | 13,495.24 | +0.02% |

| AUD/USD | 0.69 | -0.13% |

| NZD/USD | 0.57 | +0.19% |

| AUD/NZD | 1.22 | -0.35% |

| BHP | 58.99 | +0.80% |

| Gold | 4,030.50 | -1.18% |

| Brent Crude | 73.64 | +2.29% |

| Bitcoin | 60,393.96 | +1.45% |

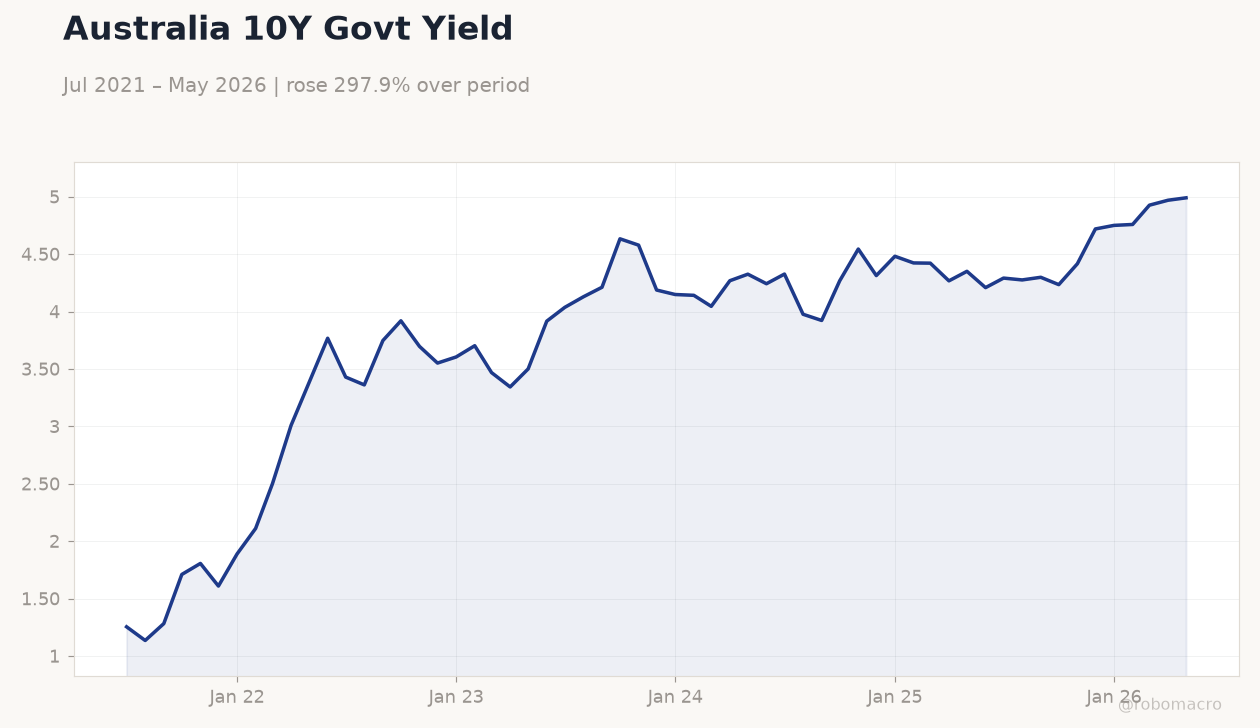

| Australia 10Y Govt Yield | 4.99% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBA Kent Speech | - | - | - |

Australia 10Y Govt Yield | Type: macro_line | Percent: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.99

Australia 10Y Govt Yield | Type: macro_line | Percent: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.99

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| ANZ Business Confidence | 10 | - | 17:00 |

| RBA Meeting Minutes | - | - | 17:30 |

| Ai Group Industry Index | -26.50 | - | 15:00 |

| Building Permits Month-over-Month Prel | -3.40 | 1 | 17:30 |

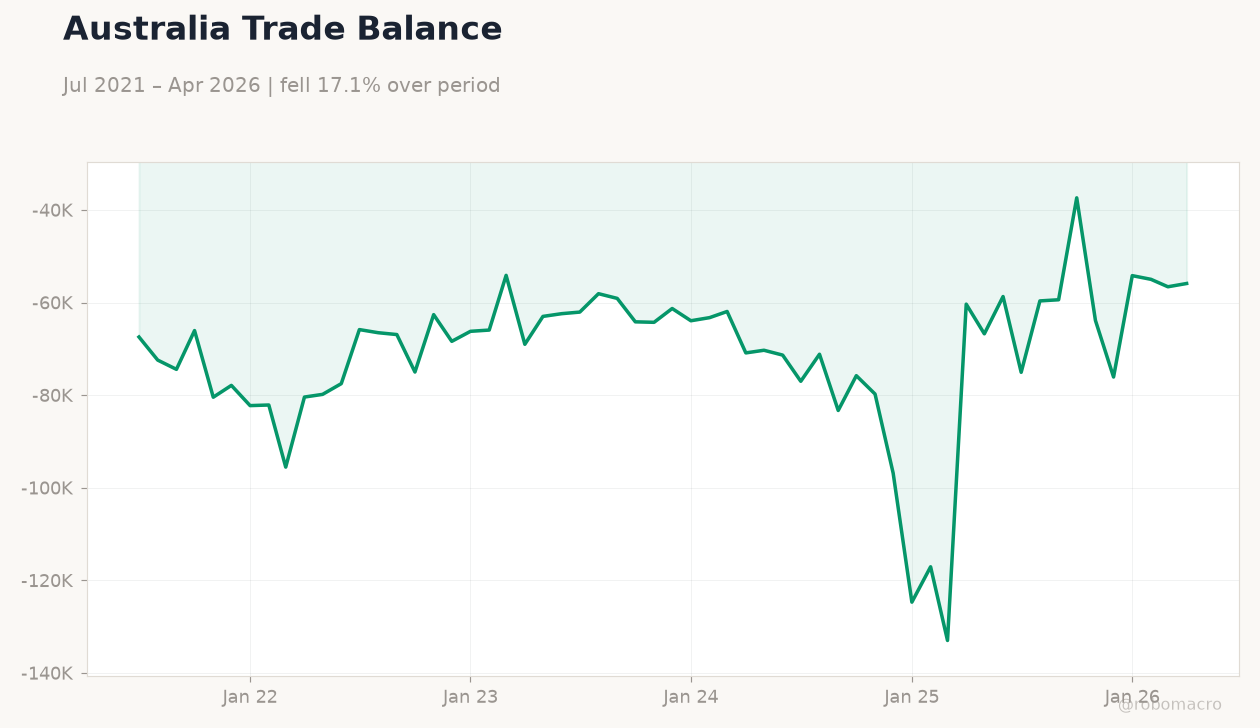

| Trade Balance | 1,791m | 2,300m | 17:30 |

- RBA minutes and NZ business confidence due today as AUD nears three-month lows.

- ASX 200 rises 0.18% while AUD/USD falls to 0.69 on cooling growth signals.

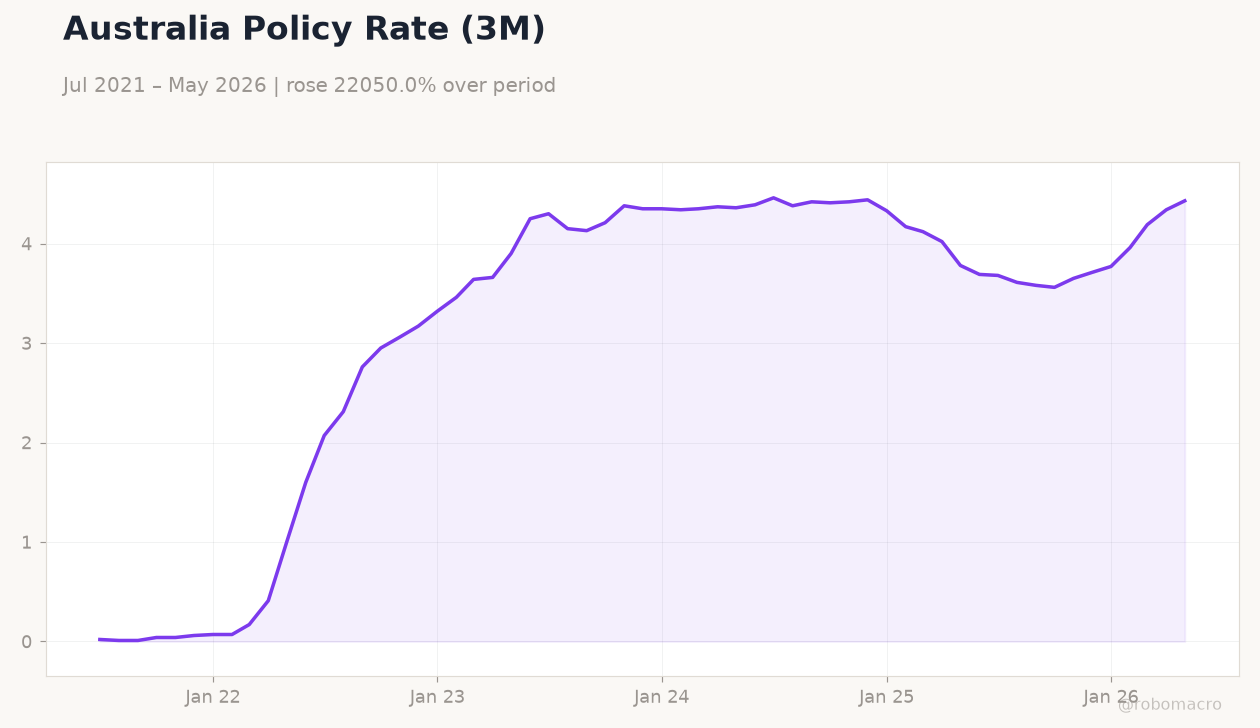

- RBA holds cash rate at 4.31% with both central banks signalling steady policy near term.

Yesterday's Recap

RBA Deputy Governor Kent stated the bank is better prepared for future crises after reviewing pandemic-era bond purchases that delivered only marginal effects. The ASX 200 advanced 0.18% to 8,764.20, led by BHP which gained 0.80% to 58.99 on firmer iron-ore futures. NZX 50 edged 0.02% higher to 13,495.24.

AUD/USD slipped 0.13% to 0.69 while NZD/USD rose 0.19% to 0.57, narrowing AUD/NZD 0.35% to 1.22. Australian 10-year yields climbed 0.42% to 4.99% and NZ short-term rates fell 9.60% to 4.33%. Gold dropped 1.18% to 4,030.50 while Brent crude rose 2.29% to 73.64.

Bitcoin gained 1.45% to 60,393.96.

The Day Ahead

RBA meeting minutes at 17:30 AEST will clarify the board’s assessment of cooling domestic demand and inflation trajectory. New Zealand ANZ Business Confidence prints at 17:00 NZT, offering an early read on Q3 sentiment after dairy prices weakened. Tomorrow’s Ai Group Industry Index and preliminary building permits data will test whether Australia’s construction sector is stabilising.

Australia’s June trade balance on 1 July is expected to widen to A$2.3 bn on sustained commodity exports to China.

Other Economic Notes

Australia’s housing market is cooling in Sydney and Melbourne as higher rates and new tax rules curb investor demand. Early signs of economic softness have emerged, with retail sales and employment prints showing modest downside surprises relative to prior strength. Inflation is projected to peak near 4.25% before moderating, supporting the RBA’s decision to remain on hold.

RBA research continues to explore additional monetary tools for future downturns while acknowledging near-zero rates may return sooner than markets anticipate.

Global Macro News

US dollar strength after hotter US inflation data has weighed on both AUD and NZD, with the yen also hitting 40-year lows. China liquidity measures lifted iron-ore prices, supporting Australian terms of trade and widening the monthly trade surplus toward A$7 bn. <i>↓ p.2</i>