ANZ Macro Daily(Beta Mode)

RBA Minutes Flag Persistent Inflation Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,823.40 | +0.68% |

| NZX 50 | 13,621.66 | +0.56% |

| AUD/USD | 0.69 | +0.43% |

| NZD/USD | 0.57 | +0.72% |

| AUD/NZD | 1.22 | -0.29% |

| BHP | 59.39 | -0.72% |

| Gold | 4,033.20 | +0.27% |

| Brent Crude | 73.42 | +0.37% |

| Bitcoin | 58,658.60 | -2.46% |

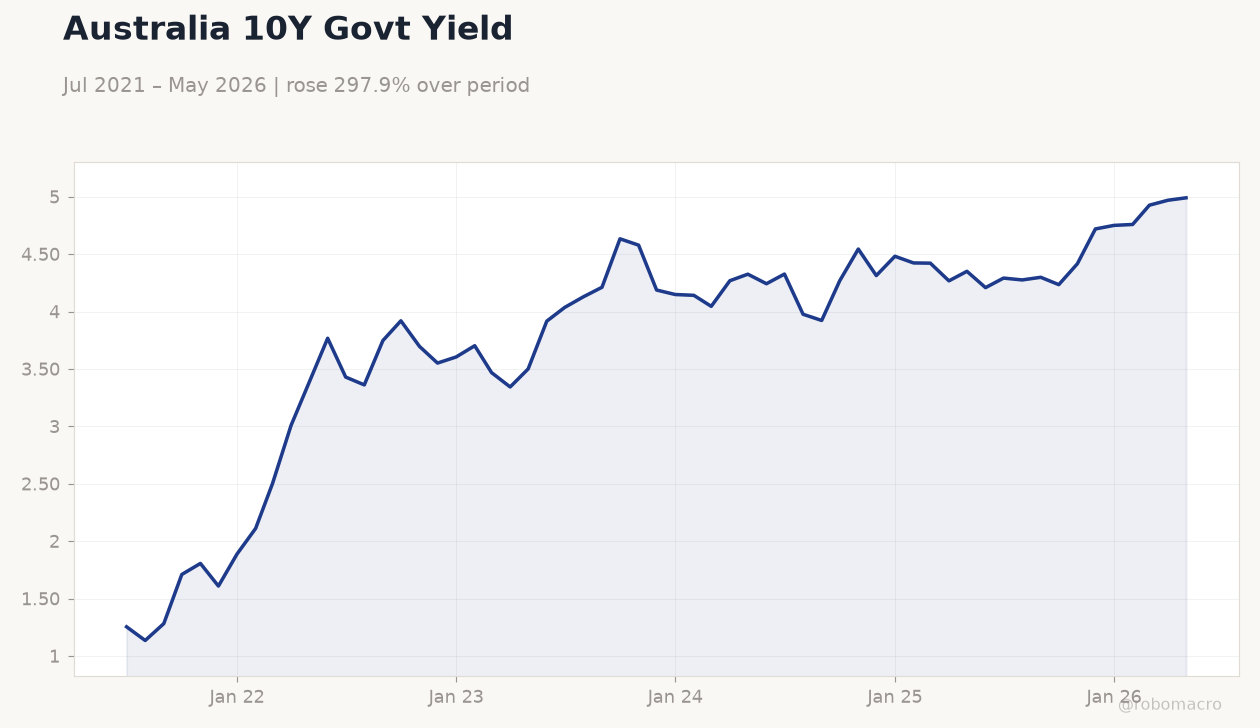

| Australia 10Y Govt Yield | 4.99% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBA Kent Speech | - | - | - |

| ANZ Business Confidence | 10 | - | 36.60 |

| RBA Meeting Minutes | - | - | - |

Australia 10Y Govt Yield | Type: macro_line | Yield %: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.99

Australia 10Y Govt Yield | Type: macro_line | Yield %: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.99

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Ai Group Industry Index | -26.50 | - | 19:00 |

| Building Permits Month-over-Month Prel | -3.40 | 1 | 21:30 |

| Trade Balance | 1,791m | 2,300m | 21:30 |

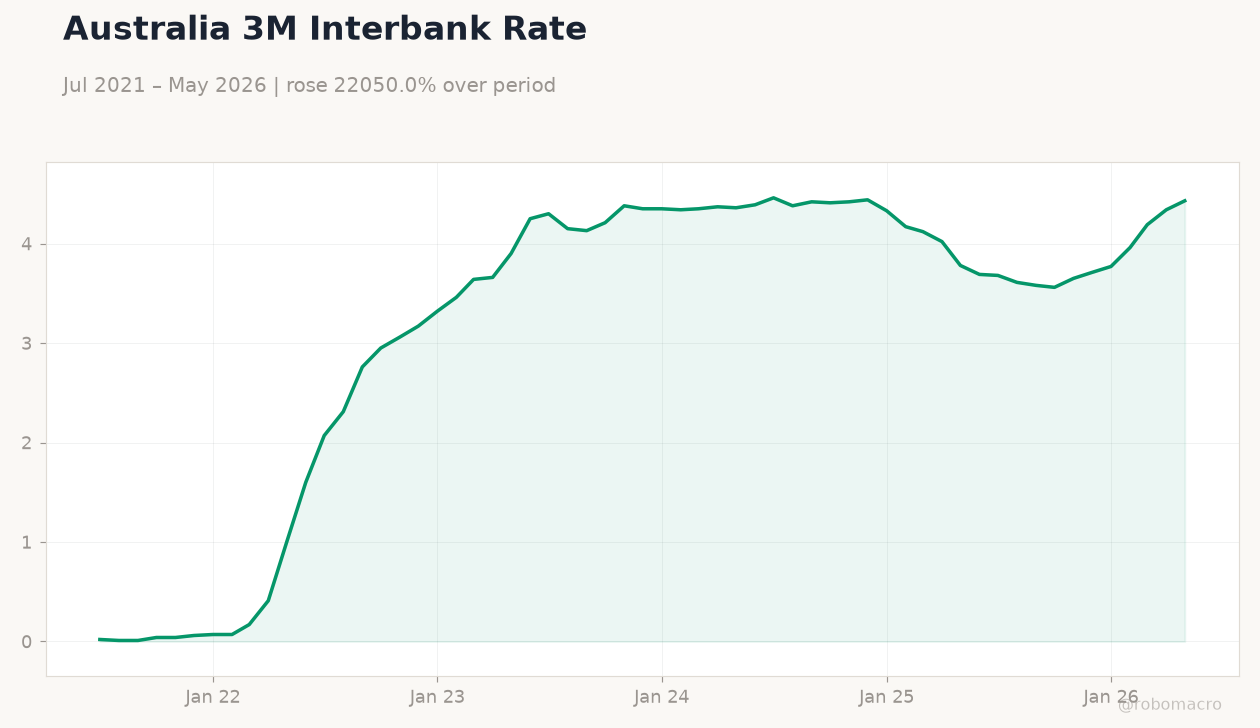

- RBA minutes and Kent speech underscore persistent inflation above target, keeping further hikes in play despite June hold at 4.31%.

- New Zealand ANZ Business Confidence surged to 36.6, signalling improving sentiment, while Australian equities and AUD posted solid gains.

- ASX 200 rose 0.68% to 8,823.40 and AUD/USD climbed to 0.69 as commodity prices edged higher on China demand signals.

Yesterday's Recap

Australian markets digested the RBA June meeting minutes and Governor Kent’s speech, both of which stressed that inflation remains materially above the 2–3% target and that policy must stay restrictive. The committee voted to hold the cash rate at 4.31%, citing slowing growth yet flagging upside risks from wages and energy prices. In New Zealand, ANZ Business Confidence jumped sharply to 36.6 from 10.0, reflecting stronger business optimism.

The ASX 200 advanced 0.68% to 8,823.40 while the NZX 50 gained 0.56% to 13,621.66. AUD/USD rose 0.43% to 0.69 and NZD/USD added 0.72% to 0.57, supported by firmer commodity prices. Australian 10-year yields lifted 0.42% to 4.99% as markets priced a higher probability of additional RBA tightening later this year.

The Day Ahead

Australia releases the Ai Group Industry Index at 19:00, expected to show continued contraction in manufacturing conditions. Building Permits month-over-month preliminary data follow at 21:30, with consensus pointing to a 1% rebound after last month’s 3.4% drop. The June Trade Balance print, due tomorrow evening, is forecast to widen to A$2.3 bn from A$1.79 bn, reflecting resilient commodity exports.

No major New Zealand data are scheduled, leaving markets focused on Australian housing and external trade metrics. RBNZ speakers remain quiet ahead of next week’s policy decision.

Other Economic Notes

Weak productivity growth continues to concern the RBA, limiting the economy’s speed limit to around 1% annual GDP expansion. Housing approvals in both countries remain soft, keeping mortgage-rate sensitivity high for households. Commodity receipts, especially iron ore and dairy, continue to underpin fiscal and current-account balances, with China stimulus expectations providing the dominant external tailwind.

Union wage pressures and geopolitical oil risks are cited by the RBA as key inflation upside factors that could delay any easing cycle.