ANZ Macro Daily(Beta Mode)

RBA Minutes Leave Hike Option Open

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,778.70 | -0.51% |

| NZX 50 | 13,610.50 | -0.08% |

| AUD/USD | 0.69 | +0.20% |

| NZD/USD | 0.57 | +0.40% |

| AUD/NZD | 1.22 | -0.22% |

| BHP | 60.26 | +1.44% |

| Gold | 4,063.50 | +1.01% |

| Brent Crude | 71.19 | -2.37% |

| Bitcoin | 59,944.24 | +2.37% |

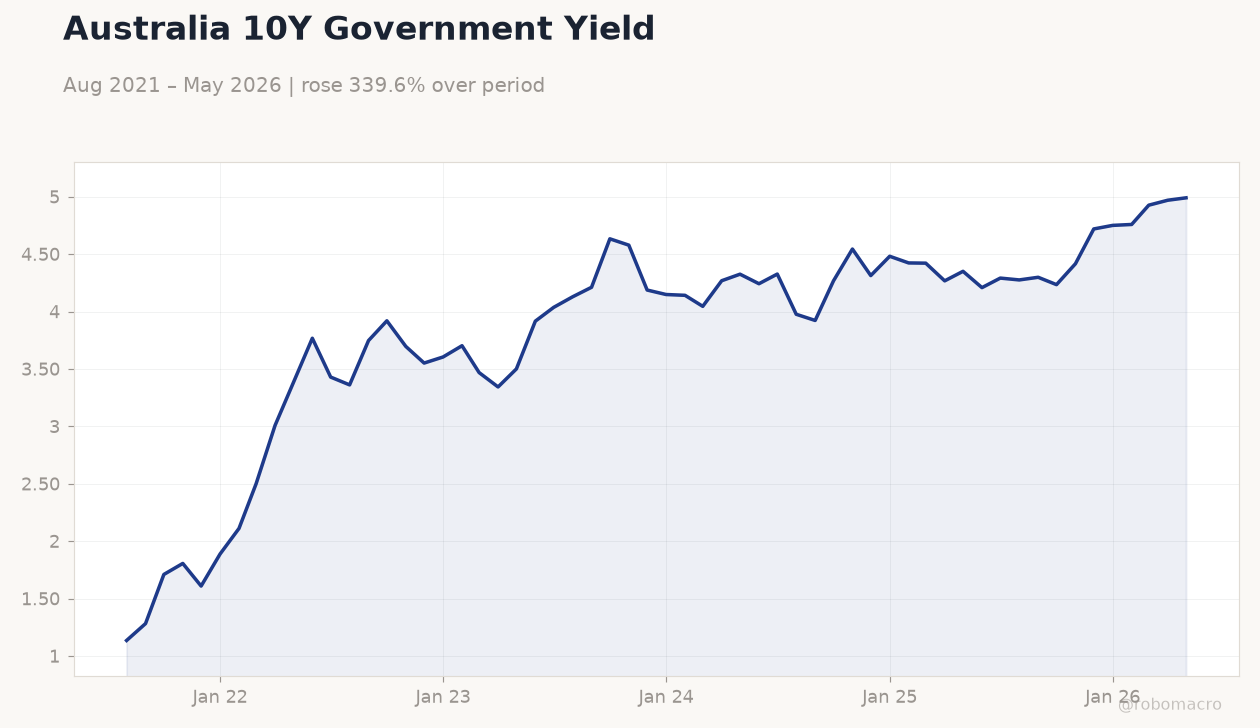

| Australia 10Y Govt Yield | 4.99% | +0.42% |

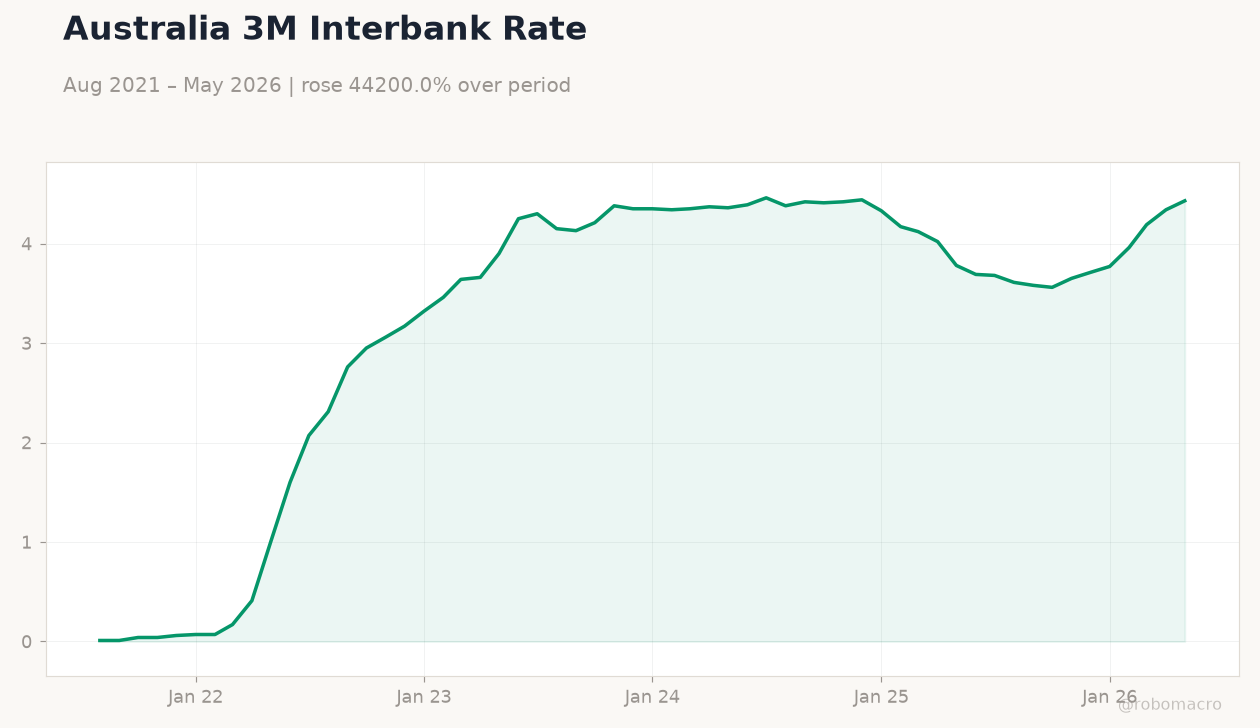

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBA Kent Speech | - | - | - |

| ANZ Business Confidence | 10 | - | 36.60 |

| RBA Meeting Minutes | - | - | - |

| Ai Group Industry Index | -30.50 | - | -30 |

| Building Permits Month-over-Month Prel | -0.20 | 1 | -1.10 |

Australia 10Y Government Yield | Type: macro_line | 10Y Yield %: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.135,3.919,4.187,4.423,4.969,4.99

Australia 10Y Government Yield | Type: macro_line | 10Y Yield %: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.135,3.919,4.187,4.423,4.969,4.99

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | 1,791m | 2,300m | 17:30 |

- NZ ANZ Business Confidence surged to 36.6 from 10.0, signalling stronger sentiment.

- Australian building permits fell 1.1% MoM while Ai Group index edged to -30.0.

- RBA minutes highlighted persistent inflation risks above target, keeping hike option open.

Yesterday's Recap

Australian markets saw the ASX 200 decline 0.51% to 8,778.70 as RBA minutes reinforced concerns over inflation remaining materially above target. The RBA Kent speech and released minutes stressed that rates are hurting activity yet further tightening may still be required, with unions cited as a contributing factor. New Zealand data showed a sharp rebound in ANZ Business Confidence to 36.6, though the NZX 50 slipped 0.08% to 13,610.50.

AUD/USD rose 0.20% to 0.69 while NZD/USD gained 0.40% to 0.57, supported by firmer commodity prices including gold at 4,063.50. Australian 10-year yields climbed 0.42% to 4.99% and NZ short-term rates eased 9.60% to 4.33%. Building permits printed weaker than expected at -1.1% MoM and the Ai Group Industry Index improved only marginally to -30.0.

Overall risk sentiment remained cautious ahead of today’s Australian trade balance release.

The Day Ahead

Markets focus on Australia’s June trade balance, forecast at A$2.3 bn versus A$1.79 bn prior, with China demand signals likely to dominate the print. No major New Zealand data are scheduled. RBA and RBNZ speakers are quiet, leaving commodity prices and US dollar moves as the main drivers for AUD and NZD.

Iron ore and gold strength should continue to underpin Australian export values. Any surprise widening in the surplus would reinforce AUD outperformance versus NZD.

Other Economic Notes

Australia’s commodity export base remains tightly linked to China steel output and stimulus signals, with BHP rising 1.44% on firmer iron ore. Housing markets face pressure from higher rates, as RBA minutes flagged budget measures influencing loan demand. New Zealand’s dairy and tourism sectors benefit from the business confidence lift but still face delayed recovery per IMF commentary.

Both economies continue to show inflation above target, limiting near-term easing prospects.