ANZ Macro Daily(Beta Mode)

Australian Trade Deficit Widens, Weighs on AUD

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,722.90 | -0.64% |

| NZX 50 | 13,582.19 | -0.21% |

| AUD/USD | 0.69 | +0.44% |

| NZD/USD | 0.57 | +0.39% |

| AUD/NZD | 1.21 | -0.25% |

| BHP | 59.57 | -0.58% |

| Gold | 4,130.80 | +1.54% |

| Brent Crude | 71.61 | +0.06% |

| Bitcoin | 61,361.29 | +2.26% |

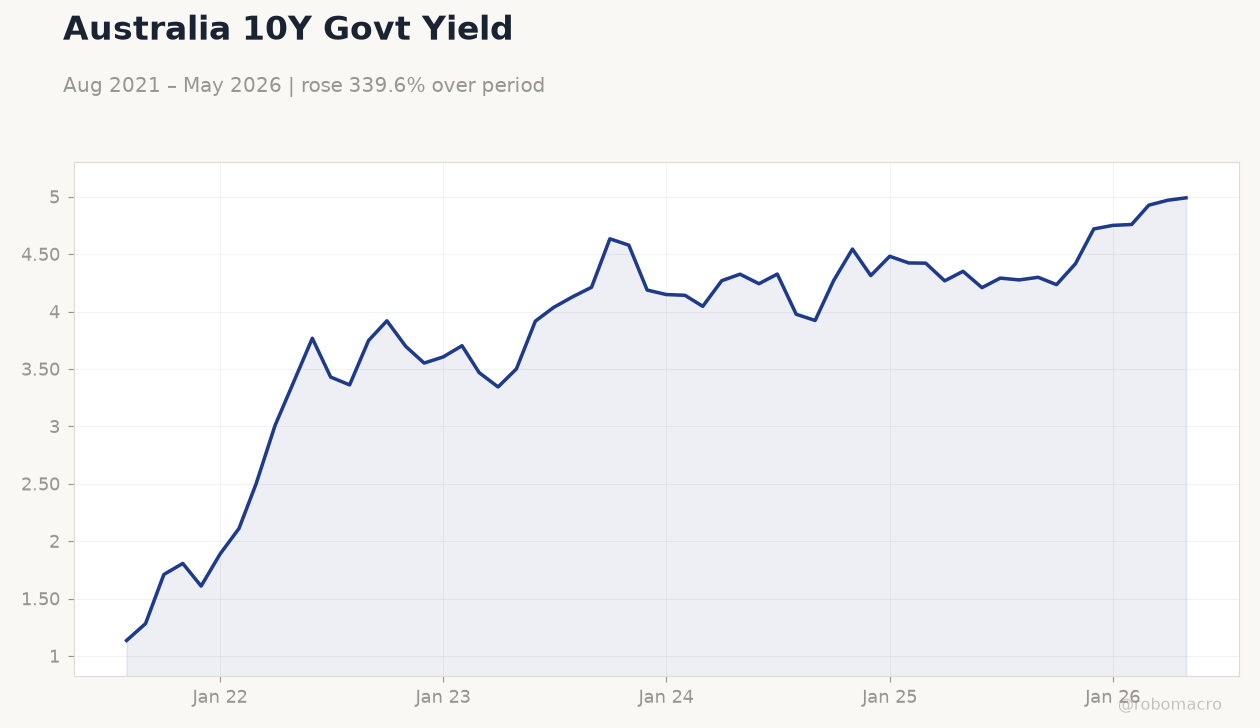

| Australia 10Y Govt Yield | 4.99% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBA Kent Speech | - | - | - |

| Building Permits Month-over-Month Prel | -0.20 | 1 | -1.10 |

| Trade Balance | 1,383m | 2,200m | -3,018m |

Australia 10Y Govt Yield | Type: macro_line | Percent: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.135,3.919,4.187,4.423,4.969,4.99

Australia 10Y Govt Yield | Type: macro_line | Percent: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.135,3.919,4.187,4.423,4.969,4.99

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Australia posted a A$3.018 billion trade deficit in May, missing consensus by a wide margin and highlighting softening commodity export momentum.

- Building permits fell 1.1% month-over-month, exceeding the expected 1% gain and adding to concerns over housing activity.

- ASX 200 declined 0.64% while AUD/USD rose 0.44% to 0.69 amid resilient US dollar pressure and RBA hawkish signals.

Yesterday's Recap

Australia’s May trade balance swung to a A$3.018 billion deficit against a A$2.2 billion consensus, driven by weaker goods exports. Building permits contracted 1.1% month-over-month, reversing the prior 0.2% decline and signalling cooling housing momentum. RBA Assistant Governor Kent delivered remarks that markets interpreted as cautious on near-term easing.

The ASX 200 fell 0.64% to 8,722.90 while the NZX 50 slipped 0.21% to 13,582.19. AUD/USD gained 0.44% to 0.69 and NZD/USD rose 0.39% to 0.57 despite the trade print. Australian 10-year yields climbed 0.42% to 4.99% as investors pared rate-cut bets.

BHP shares declined 0.58% to 59.57, tracking softer iron-ore sentiment.

The Day Ahead

No major ANZ data releases are scheduled for 2-3 July. Markets will monitor RBA June minutes due next week for further policy clues. Attention also turns to the RBNZ 8 July meeting, where Westpac expects a hold at the current cash rate.

China’s Caixin services PMI on 4 July will provide the next read on external demand for Australian commodities. NZ retail sales data the same day may highlight ongoing domestic weakness. Thin trading volumes are likely to keep AUD and NZD sensitive to US dollar moves.

Other Economic Notes

Persistent housing market weakness in Australia risks weighing on consumption and construction activity through 2026. Tight financial conditions continue to support the case for the RBA remaining on hold despite below-target inflation. New Zealand’s dairy export earnings remain the key support for the NZD amid subdued domestic demand.

Both economies remain heavily exposed to China’s growth trajectory, with iron ore and dairy prices acting as leading indicators. Productivity concerns flagged by the RBA add to medium-term growth risks.