ANZ Macro Daily(Beta Mode)

RBA Hawkish Hold Lifts AUD Ahead of RBNZ

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,844.40 | +1.37% |

| NZX 50 | 13,618.42 | +0.27% |

| AUD/USD | 0.69 | +0.43% |

| NZD/USD | 0.57 | +0.35% |

| AUD/NZD | 1.22 | +0.03% |

| BHP | 60.50 | +1.56% |

| Gold | 4,187.30 | +1.81% |

| Brent Crude | 72.13 | +0.46% |

| Bitcoin | 62,733.43 | -0.56% |

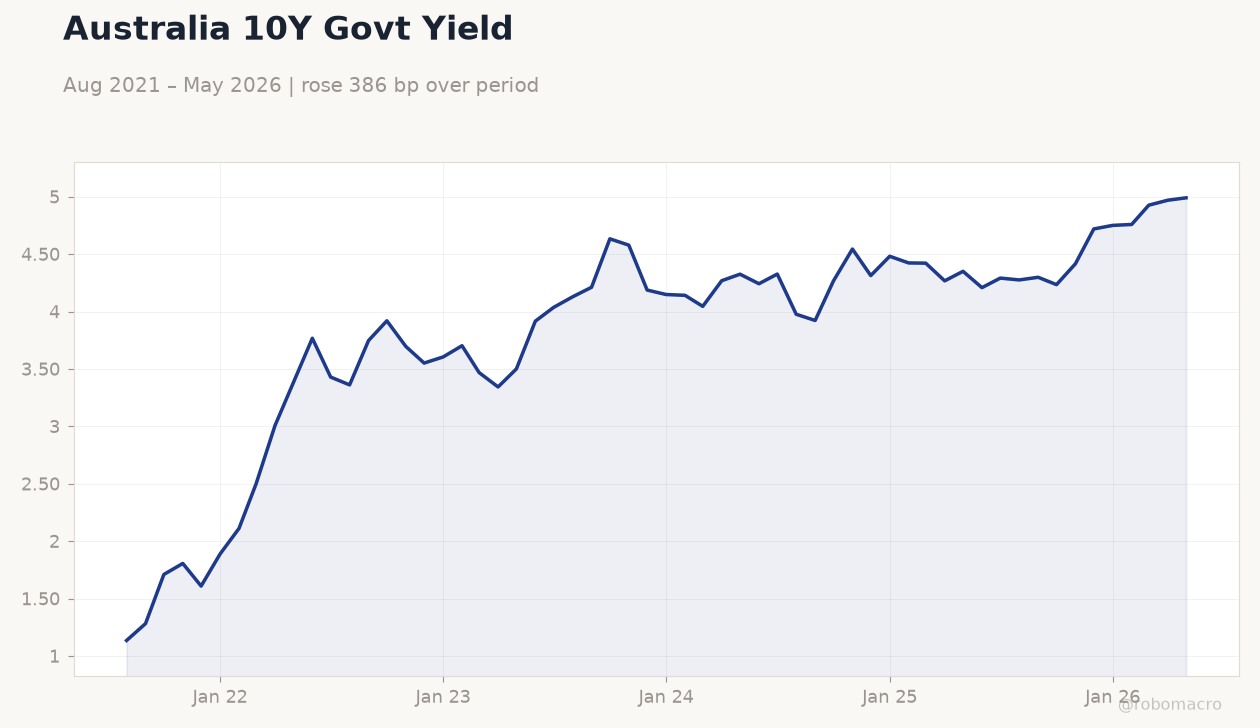

| Australia 10Y Govt Yield | 4.99% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Australia 10Y Govt Yield | Type: macro_line | Yield %: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.135,3.919,4.187,4.423,4.969,4.99

Australia 10Y Govt Yield | Type: macro_line | Yield %: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.135,3.919,4.187,4.423,4.969,4.99

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RBA Hunter Speech | - | - | 21:00 |

| RBNZ Interest Rate Decision | 2.25 | 2.50 | 22:00 |

| Business NZ PMI | 49.90 | - | 18:30 |

- RBA held cash rate at verified 4.31% with hawkish tone, lifting AUD/USD 0.43% to 0.69 on resilient data and trade surplus.

- ASX 200 rose 1.37% to 8,844.40 and NZX 50 gained 0.27% to 13,618.42, led by BHP at 60.50 amid firmer commodities.

- RBNZ decision due 7 July with consensus for 25bp hike to 2.50% from 2.25%; NZ short-term rate fell 9.60% to 4.33%.

Yesterday's Recap

Australian markets advanced on 4 July as the ASX 200 closed at 8,844.40, up 1.37%, led by BHP at 60.50 after iron-ore gains. The NZX 50 edged 0.27% higher to 13,618.42 on defensive buying. AUD/USD climbed 0.43% to 0.69 and NZD/USD rose 0.35% to 0.57, reflecting risk appetite and hawkish RBA signals.

Australian 10-year yields reached 4.99% while gold surged 1.81% to 4,187.30 on safe-haven flows. Brent crude added 0.46% to 72.13. No major ANZ data releases occurred on the holiday-shortened session, leaving focus on prior employment resilience and trade surplus support for the Australian dollar.

The Day Ahead

RBA Assistant Governor Hunter speaks on 7 July at 21:00, likely reinforcing the hawkish hold stance. The RBNZ announces its interest rate decision the same evening at 22:00, with consensus pointing to a 25bp lift to 2.50% from 2.25%. Business NZ PMI follows on 8 July at 18:30, testing manufacturing momentum after the prior 49.9 print.

Australian housing and retail data later in the week will shape RBA policy views. Markets will monitor any divergence between RBA and RBNZ signals given independent inflation targets.

Other Economic Notes

Australia continues to post the highest inflation among major developed economies, sustaining RBA caution despite global easing. Home-building approvals have moderated while staff wage negotiations at the RBA highlight domestic cost pressures. New Zealand’s dairy prices and tourism inflows provide partial offset to construction weakness.

China’s steel output and restocking remain the dominant external driver for Australian commodity revenues and both currencies.

Global Macro News

Fed policy expectations and upcoming minutes keep global yields in focus, supporting AUD and NZD carry trades. Yen weakness below 160 has prompted intervention speculation that could indirectly pressure commodity currencies. Chinese inflation and stimulus signals directly influence iron-ore and LNG demand critical to Australia.

<i>↓ p.2</i>