ASEAN Macro Daily(Beta Mode)

ID Inflation Jumps, TH Surprises With Cut

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 8,016.83 | -2.66% |

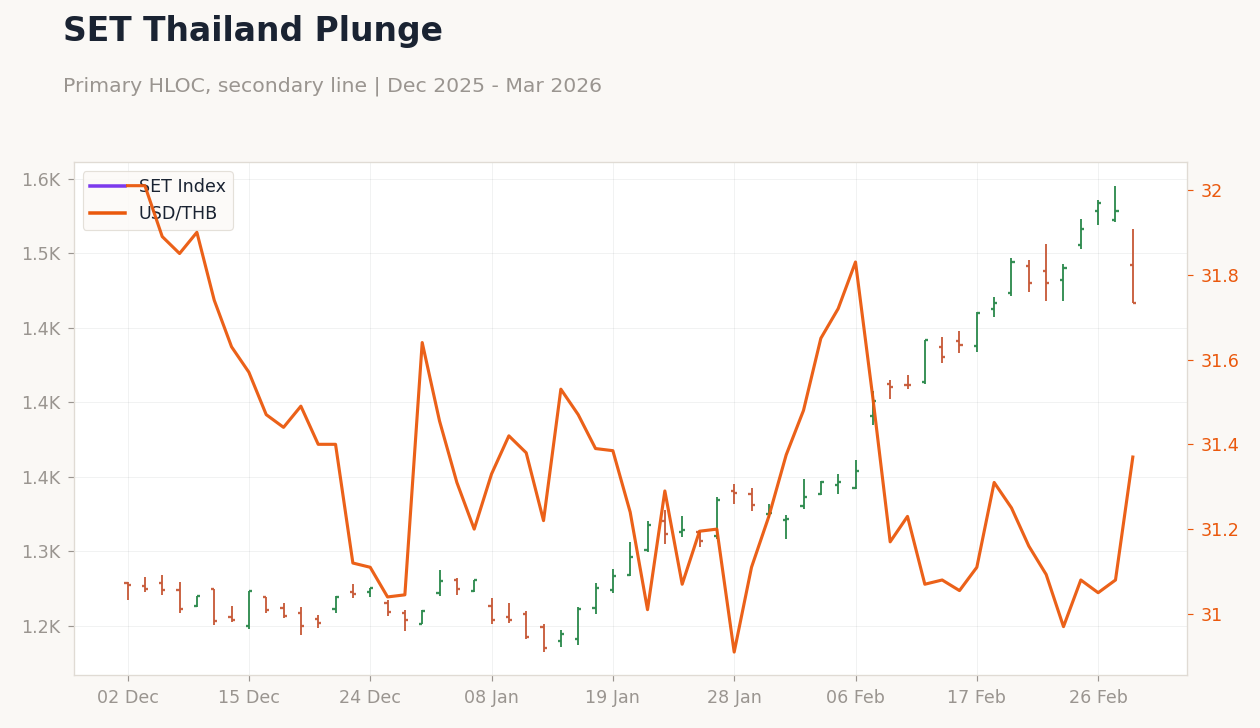

| SET | 1,466.51 | -4.04% |

| KLCI | 1,700.21 | -0.96% |

| PSEi | 6,426.83 | -2.79% |

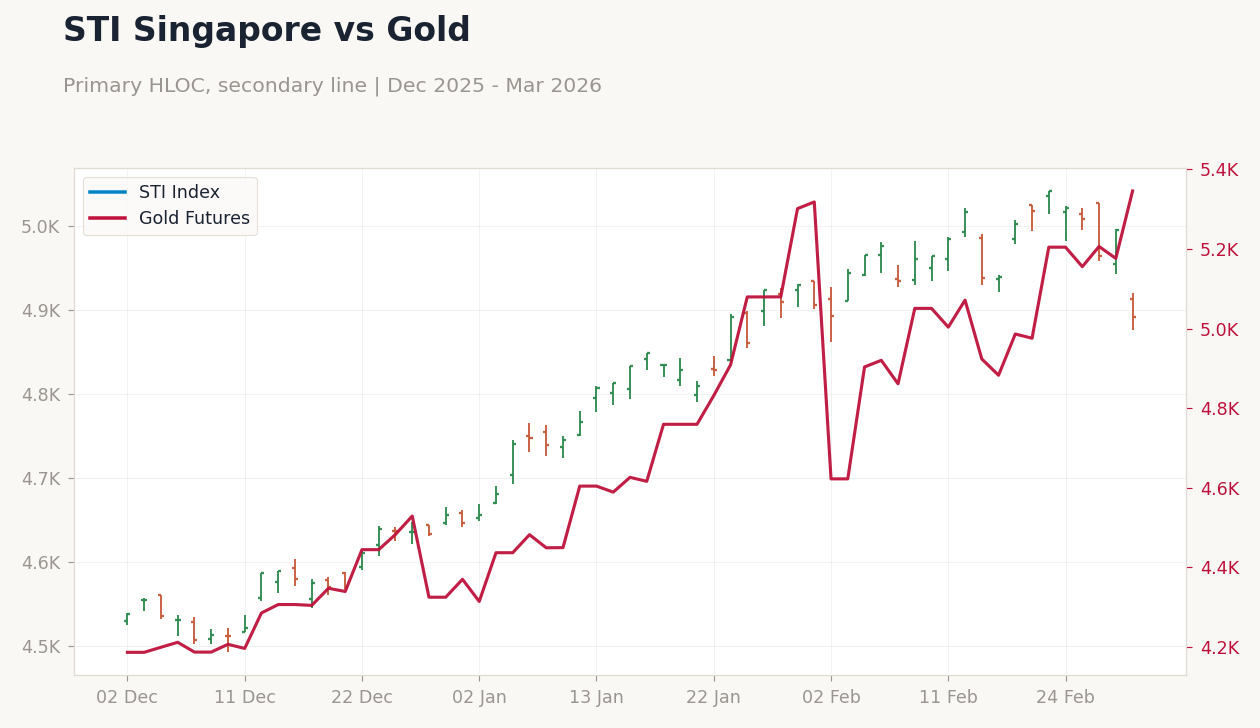

| STI | 4,890.86 | -2.09% |

| USD/IDR | 16,843.00 | +0.56% |

| USD/THB | 31.08 | +0.10% |

| USD/MYR | 3.92 | +1.08% |

| USD/PHP | 58.16 | +1.04% |

| USD/SGD | 1.27 | +0.78% |

| Brent Crude | 77.66 | +7.15% |

| Gold | 5,335.90 | +2.02% |

| Bitcoin | 69,291.18 | +5.40% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | 2,520m | 2,760m | 950m |

| Inflation Rate Year-over-Year | 3.55 | - | 4.76 |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2 | 2.40 | 15:00 |

- Indonesia's inflation surged to 4.76% YoY from 3.55%, while trade balance missed at $950M vs consensus $2.76B, weighing on JCI and rupiah.

- Bank of Thailand unexpectedly cut rates in a 4-2 vote to support recovery amid tariff risks, sparking SET plunge and regional sell-off.

- ASEAN equities fell sharply, currencies weakened vs USD, as Iran attack drove oil spike and global risk aversion.

Yesterday's Recap

Indonesia led key data releases with February inflation accelerating to 4.76% year-over-year from 3.55% prior, fueled by rising food and energy prices, while the trade surplus shrank to $950 million against a consensus of $2.76 billion, due to softer exports amid global slowdowns. This disappointed investors, contributing to a 2.66% drop in the JCI to 8,016.83 and a 0.56% rise in USD/IDR to 16,843.00, underscoring challenges in the commodity-reliant economy. Thailand's central bank surprised with a rate cut in a 4-2 vote to aid fragile growth facing tariff uncertainties, exacerbating market declines with the SET tumbling 4.04% to 1,466.51 and USD/THB edging up 0.10% to 31.08.

Malaysia's KLCI slipped 0.96% to 1,700.21 as USD/MYR climbed 1.08% to 3.92, affected by regional sentiment despite expectations of robust Q4 GDP growth from domestic demand. The Philippines' PSEi declined 2.79% to 6,426.83 with USD/PHP up 1.04% to 58.16, while Singapore's STI fell 2.09% to 4,890.86 and USD/SGD rose 0.78% to 1.27, both pressured by broader currency weakness and risk-off flows. No direct Vietnam data was reported, but regional trends suggest manufacturing sentiment may have softened amid the ASEAN-wide rout.

The Day Ahead

Focus shifts to the Philippines' February inflation data, scheduled for release on March 4 at 15:00 ET, with consensus at 2.4% YoY from 2.0% prior, which could shape BSP's policy if it remains in target. No significant economic indicators are due today from Indonesia, Thailand, Malaysia, Singapore, or Vietnam, giving markets time to absorb recent developments and global news. Indonesia may provide updates from its planned meeting with MSCI this week on capital market reforms, following recent volatility and downgrade risks.

Thailand's economic outlook post-rate-cut could influence regional FX, while external factors like oil price fluctuations from Iran tensions may impact energy-dependent nations such as Singapore and Thailand.

Other Economic Notes

ASEAN countries are adapting to supply chain relocations from China toward Vietnam and Indonesia, attracting manufacturing FDI but heightening exposure to US tariff risks, as evidenced by Thailand's proactive rate adjustment. The remittance-reliant Philippines and tourism-focused Thailand contend with global economic slowdowns, whereas Malaysia's anticipated Q4 GDP speedup highlights strong domestic consumption. (cont...)