ASEAN Macro Daily(Beta Mode)

Thai Rate Cut Triggers ASEAN Selloff

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 7,577.06 | -4.57% |

| SET | 1,384.61 | -5.58% |

| KLCI | 1,698.22 | -0.80% |

| PSEi | 6,307.84 | -2.13% |

| STI | 4,812.75 | -2.11% |

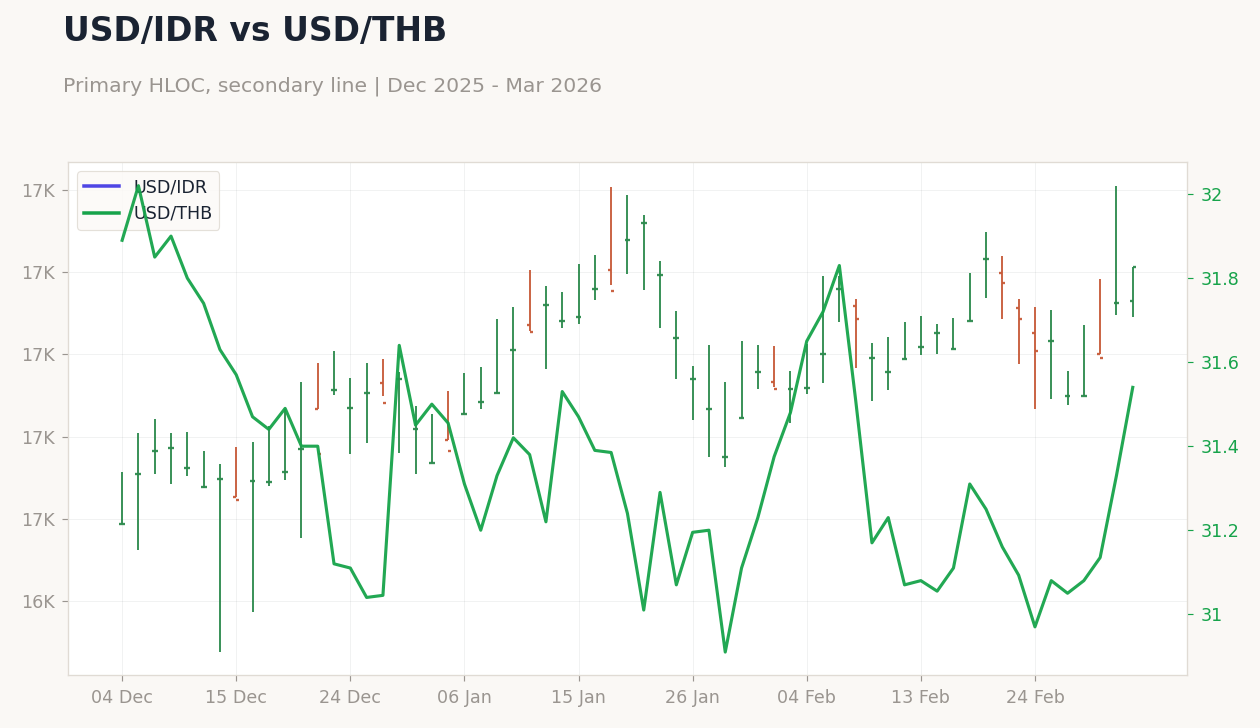

| USD/IDR | 16,906.00 | +0.25% |

| USD/THB | 31.54 | +0.67% |

| USD/MYR | 3.94 | +0.36% |

| USD/PHP | 58.42 | +0.34% |

| USD/SGD | 1.27 | +0.14% |

| Brent Crude | 82.54 | +1.40% |

| Gold | 5,151.60 | +0.87% |

| Bitcoin | 72,811.94 | +6.62% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2 | 2.40 | 15:00 |

- ASEAN stocks plunged, led by Thailand's SET (-5.58%) and Indonesia's JCI (-4.57%), amid Thai policy surprise and global risk aversion.

- Currencies weakened against USD, with THB down 0.67%, as Brent crude gained 1.40% benefiting commodity exporters.

- Bank of Thailand's unexpected rate cut underscores easing to aid recovery, while regional peers focus on inflation stability.

Yesterday's Recap

ASEAN equities suffered steep losses on March 3, 2026, with no key data releases but influenced by global volatility and local developments. Indonesia's JCI fell 4.57% to 7,577.06, weighed down by weak bond auction demand linked to Lunar New Year holidays and MSCI downgrade warnings, though ongoing talks with MSCI on capital market reforms offered some hope. Thailand's SET dropped 5.58% to 1,384.61 following the Bank of Thailand's surprise rate cut to support a fragile recovery amid tariff uncertainties.

Malaysia's KLCI declined 0.80% to 1,698.22, despite polls indicating Q4 growth likely hit its fastest pace in over a year on strong domestic demand. The Philippines' PSEi slid 2.13% to 6,307.84, pressured by profit-taking as authorities reaffirmed easing may soon end with inflation on target. Singapore's STI fell 2.11% to 4,812.75, even after recently crossing the 5,000 mark for the first time, driven by stock market revival measures and a strong Singdollar.

Currencies depreciated versus the USD, with USD/THB up 0.67% to 31.54, USD/IDR rising 0.25% to 16,906.00, USD/MYR increasing 0.36% to 3.94, USD/PHP gaining 0.34% to 58.42, and USD/SGD edging 0.14% higher to 1.27, reflecting outflows amid a strengthening dollar.

The Day Ahead

Focus shifts to the Philippines' inflation rate year-over-year data at 15:00 ET on March 4, 2026, with consensus at 2.4% after a previous 2%, which could shape Bangko Sentral ng Pilipinas' easing outlook. No other significant ASEAN events are slated for today, giving markets time to process the Thai rate cut and global signals. March 5 brings no major releases, with attention on Indonesia's follow-up meeting with MSCI this week regarding market reforms.

Singapore continues monitoring the Iran situation closely, potentially reassessing GDP forecasts if energy prices rise further. Investors will watch FX dynamics, particularly for Indonesia's commodity reliance and broader ASEAN sentiment.

Other Economic Notes

ASEAN economies are gaining from US-China supply chain diversification, with Malaysia and Vietnam drawing manufacturing FDI, while Indonesia benefits from nickel exports tied to EV battery demand. Malaysia's economy likely expanded at its quickest rate in over a year in Q4, fueled by robust domestic and export activity, in contrast to Thailand's challenges from tourism recovery and tariff risks. (cont...)