ASEAN Macro Daily(Beta Mode)

PH Inflation Meets Target, Oil Surges

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 7,585.69 | -1.62% |

| SET | 1,410.37 | -0.49% |

| KLCI | 1,718.06 | +0.28% |

| PSEi | 6,320.41 | -0.94% |

| STI | 4,848.25 | +0.03% |

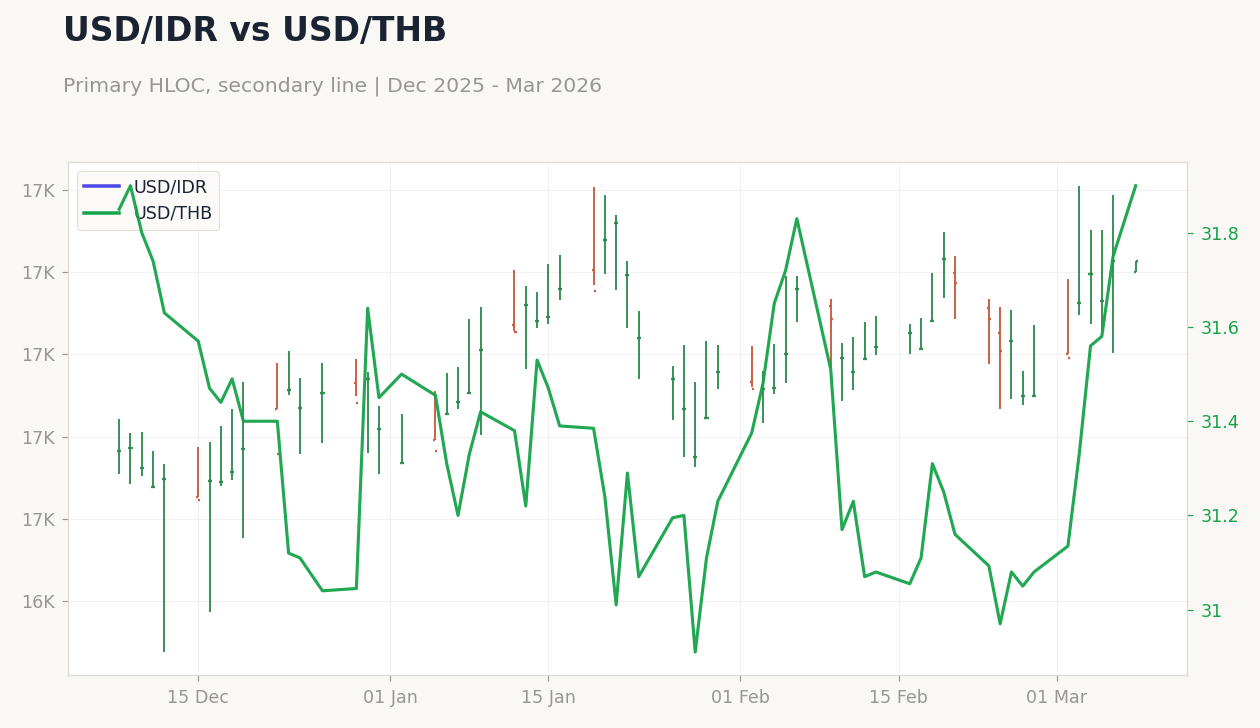

| USD/IDR | 16,914.00 | +0.01% |

| USD/THB | 31.75 | +0.00% |

| USD/MYR | 3.94 | -0.14% |

| USD/PHP | 59.02 | +0.43% |

| USD/SGD | 1.28 | +0.07% |

| Brent Crude | 92.69 | +8.52% |

| Gold | 5,158.70 | +1.84% |

| Bitcoin | 65,772.97 | -2.23% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2 | 2.40 | 2.40 |

JCI Indonesia vs SET Thailand | Type: market_hloc | JCI Level: 7586 (2026-03-06) | Range: 7577–9135 | Trend(6pt): 8711,8647,8992,8291,7711,7586 | SET Level: 1410 (2026-03-06) | Range: 1235–1534 | Trend(6pt): 1261,1260,1312,1412,1385,1410

JCI Indonesia vs SET Thailand | Type: market_hloc | JCI Level: 7586 (2026-03-06) | Range: 7577–9135 | Trend(6pt): 8711,8647,8992,8291,7711,7586 | SET Level: 1410 (2026-03-06) | Range: 1235–1534 | Trend(6pt): 1261,1260,1312,1412,1385,1410

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Philippines inflation hit 2.4% YoY, matching consensus and supporting BSP's steady stance amid remittance strength.

- ASEAN equities mixed; Indonesia's JCI dropped 1.62% on Fitch outlook cut, Malaysia's KLCI up 0.28%.

- Brent crude jumped 8.52% on Middle East tensions, aiding commodity-linked ASEAN economies.

Yesterday's Recap

Philippines inflation climbed to 2.4% YoY, meeting consensus expectations and rising from the previous 2%, underscoring stable demand in its remittance-fueled economy. Indonesia's JCI index fell 1.62% to 7,585.69, pressured by Fitch Ratings' shift of the credit rating outlook to negative due to growing uncertainty. Thailand's SET index declined 0.49% to 1,410.37, weighed down by tourism vulnerabilities after the Bank of Thailand's unexpected rate cut.

Malaysia's KLCI advanced 0.28% to 1,718.06, bolstered by manufacturing strength despite external risks. The Philippines' PSEi decreased 0.94% to 6,320.41, reflecting broader market caution. Singapore's STI inched up 0.03% to 4,848.25, supported by financial sector steadiness.

Currency movements were subdued: USD/IDR rose 0.01% to 16,914.00, USD/THB held flat at 31.75, USD/MYR fell 0.14% to 3.94, USD/PHP increased 0.43% to 59.02, and USD/SGD gained 0.07% to 1.28. Brent crude surged 8.52% to 92.69, offering a lift to resource exporters like Indonesia amid global volatility.

The Day Ahead

No significant ASEAN economic releases are planned for today, giving markets time to absorb the Philippines' inflation data and escalating oil prices. Indonesia may see attention on its upcoming meeting with MSCI to discuss capital market reforms, potentially stabilizing JCI after recent routs. Thailand's focus could shift to economic signals following the Bank of Thailand's rate cut, though no events are scheduled.

Malaysia's anticipated Q4 GDP growth, polled as the fastest in over a year, may influence sentiment. Singapore officials are closely tracking the Iran situation, with possible reassessments of GDP forecasts if energy prices rise further. Vietnam's calendar is empty, but ongoing manufacturing trends remain in view amid global supply chain shifts.

Other Economic Notes

Middle East conflict is heightening oil price risks, threatening inflation in import-reliant ASEAN nations like the Philippines and Thailand, where fuel costs could climb to ₱90 per liter and affect transport and power prices. Maersk's suspension of key shipping services due to the Iran war disrupts global trade, challenging Singapore's logistics role and Vietnam's export manufacturing. Indonesia's weak bond auction, linked to holidays and MSCI downgrade concerns, signals market jitters ahead of central bank decisions.

(cont...)