Yesterday's Recap

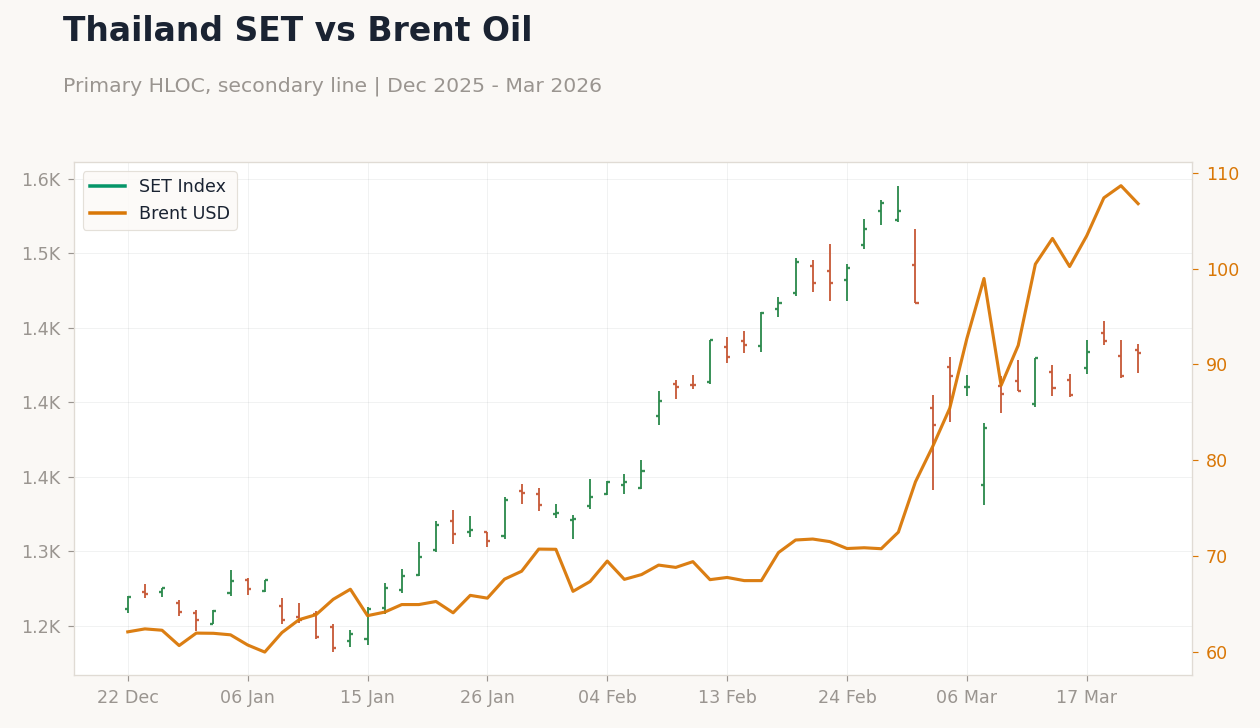

Bank Indonesia (BI) held its benchmark rate steady at 4.75% in a hawkish decision, extending tight policy through 2026 to combat inflation risks from soaring oil prices and support rupiah stability amid Middle East tensions. Malaysia released softer-than-expected inflation data, with February YoY CPI at 1.4% versus consensus 1.6% and prior 1.6%, while MoM rose to 0.2% from 0.1%, potentially giving Bank Negara Malaysia (BNM) room for easing if global risks subside. Indonesian equities outperformed with the JCI rising 1.20% to 7,106.84, buoyed by commodity plays despite Brent crude falling 1.73% to 106.77, while Thailand's SET gained 1.10% to 1,432.99 on tourism optimism.

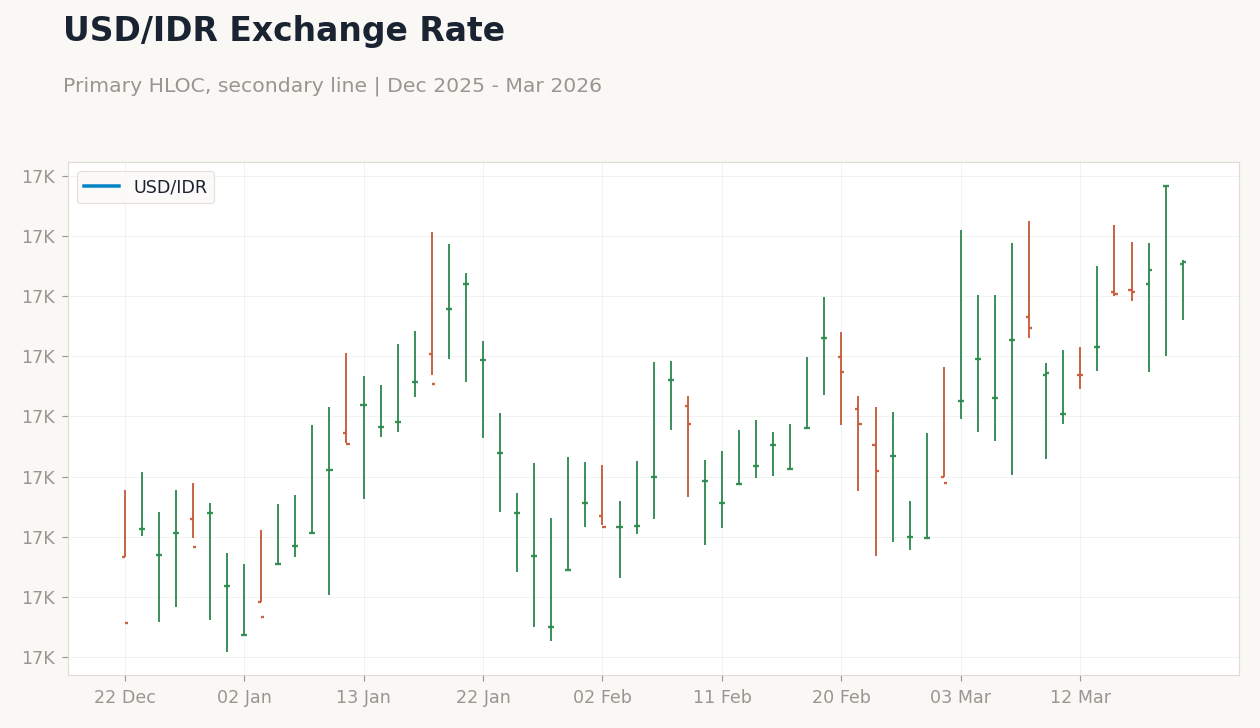

In contrast, Malaysia's KLCI dipped 0.53% to 1,720.71 amid export concerns, and the Philippines' PSEi fell 0.61% to 6,018.62 on peso weakness hitting P60 per dollar. Singapore's STI edged down 0.38% to 4,948.87, reflecting financial sector caution. Currencies showed resilience: USD/IDR declined 0.37% to 16,978.00 as BI monitored offshore rupiah moves, while USD/THB eased 0.09% to 32.77 despite Bank of Thailand (BoT) warnings on baht volatility from Iran conflict.

USD/MYR rose 0.08% to 3.94, USD/PHP increased 0.06% to 59.80, and USD/SGD fell 0.13% to 1.28. Gold dropped 2.36% to 4,492.00, pressuring resource-linked assets, while Bitcoin rose 1.19% to 70,746.03.

The Day Ahead

With no major ASEAN data releases scheduled for today or tomorrow, markets will likely focus on global cues, including any escalation in Middle East tensions that could drive oil prices higher and impact energy importers like Indonesia and Thailand. Traders in Singapore, the financial hub, may watch for updates on U.S. Treasury yields and Fed rhetoric, given the Monetary Authority of Singapore's (MAS) exchange rate policy sensitivity to dollar strength.

In the Philippines, BSP's monitoring of the Mideast conflict could influence peso trades, especially after hitting P60 per dollar. Vietnam's ongoing FDI inflows in manufacturing might support sentiment amid supply chain shifts from China. Expect thin trading in Malaysia due to the upcoming Hari Raya Aidilfitri holiday on March 21.

Overall, regional focus shifts to broader themes like commodity volatility and currency interventions.

Brent Crude Oil Prices | Type: market_hloc | Brent USD: 106.8 (2026-03-20) | Range: 59.96–108.7 | Trend(5pt): 62.07,66.52,67.55,72.48,106.8

Brent Crude Oil Prices | Type: market_hloc | Brent USD: 106.8 (2026-03-20) | Range: 59.96–108.7 | Trend(5pt): 62.07,66.52,67.55,72.48,106.8