Yesterday's Recap

Bank Indonesia (BI) held its key interest rate steady at 4.75% as expected, emphasizing rupiah defense amid global turmoil, including the Iran conflict, which could pressure commodity exports. BI clarified new rules on foreign currency transactions, while analysts expect rates to remain at 4.75% for longer, limiting rupiah gains. PT Bank Rakyat Indonesia prepared for a Lebaran 2026 surge with 1.2 million agents, boosting banking sector sentiment.

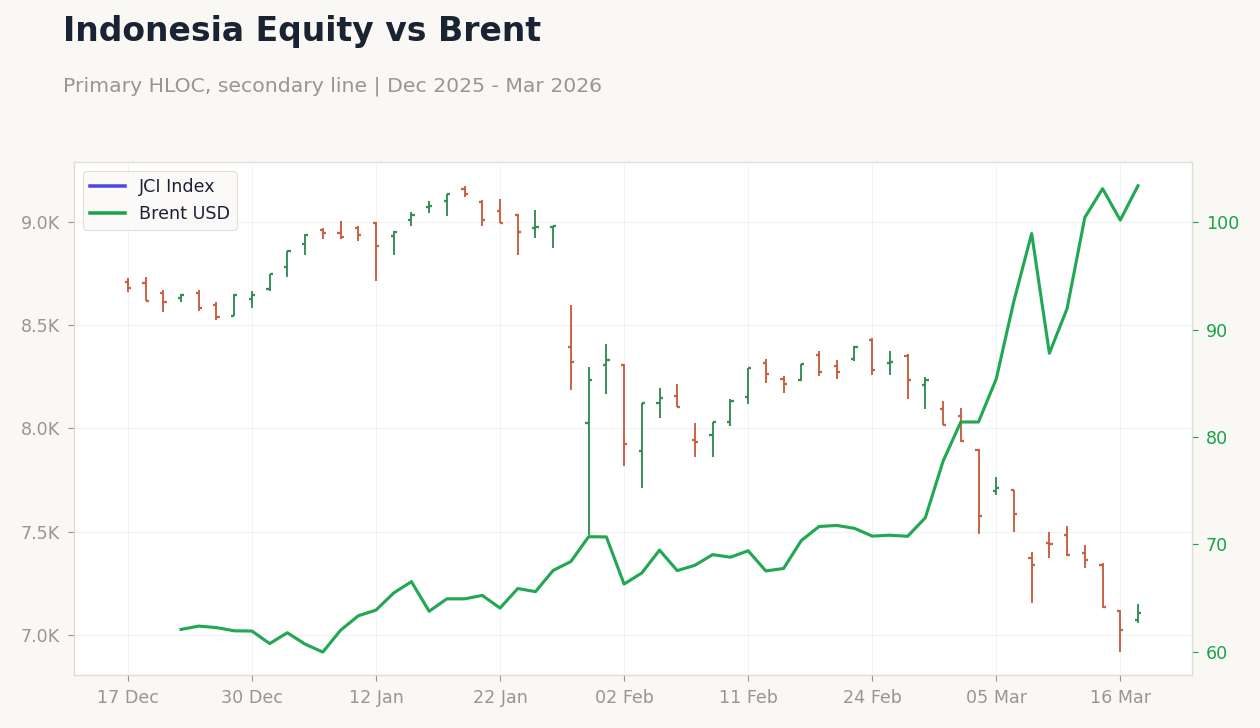

Indonesia eyes $5 billion in budget savings to cushion Iran war impacts. Malaysia reported softer-than-anticipated inflation, with February YoY CPI at 1.4% (down from 1.6% prior, below consensus of 1.6%) and MoM at 0.2% (up from 0.1%), reflecting easing food and energy costs in the manufacturing-heavy economy. Indonesia's JCI index rose 1.20% to 7,106.84, driven by banking sector strength ahead of Lebaran festivities, while Thailand's SET climbed 1.10% to 1,432.99 on tourism recovery hopes.

In contrast, Malaysia's KLCI fell 0.53% to 1,720.71 amid semiconductor headwinds, the Philippines' PSEi dropped 0.61% to 6,018.62 on remittance slowdown concerns, and Singapore's STI eased 0.38% to 4,948.87 as financials corrected. Currencies weakened broadly against the USD, with USD/IDR up 0.37% to 16,978.00 and USD/THB rising 0.83% to 32.77, USD/MYR nearly flat with a -0.01% change to 3.94, USD/PHP up 0.06% to 59.80, and USD/SGD up 0.35% to 1.28. Brent crude fell 2.06% to 106.41, gold dipped 0.56% to 4,574.90, and Bitcoin declined 1.33% to 67,799.59.

Vietnam saw no major data releases but benefited from ongoing FDI inflows in manufacturing, supporting its export growth narrative.

The Day Ahead

The ASEAN calendar remains light today with no major data releases or events scheduled across the six economies, allowing markets to digest yesterday's BI decision and Malaysia inflation figures. Investors will monitor global cues, particularly energy price volatility from the Iran war, which could influence commodity-dependent Indonesia and Malaysia. Tomorrow also features an empty slate, shifting focus to potential FX interventions by central banks like BI amid USD strength.

Attention may turn to Singapore's exchange rate band adjustments by MAS, though no immediate policy meeting is set. Broader sentiment could be swayed by any updates on US-China trade ties, given ASEAN's role in supply chain diversification. Overall, expect subdued trading volumes ahead of the weekend, with ringgit stability projected near 3.95 against the USD next week.

Indonesia Policy Rate | Type: macro_line | Indonesia Short-Term Rate %: 3.96 (2026-02-01) | Range: 2.79–6.3 | Trend(6pt): 2.79,2.79,5.62,6.17,4.13,3.96

Indonesia Policy Rate | Type: macro_line | Indonesia Short-Term Rate %: 3.96 (2026-02-01) | Range: 2.79–6.3 | Trend(6pt): 2.79,2.79,5.62,6.17,4.13,3.96