ASEAN Macro Daily(Beta Mode)

BI Holds as Rupiah Faces Pressure

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 7,164.09 | -1.89% |

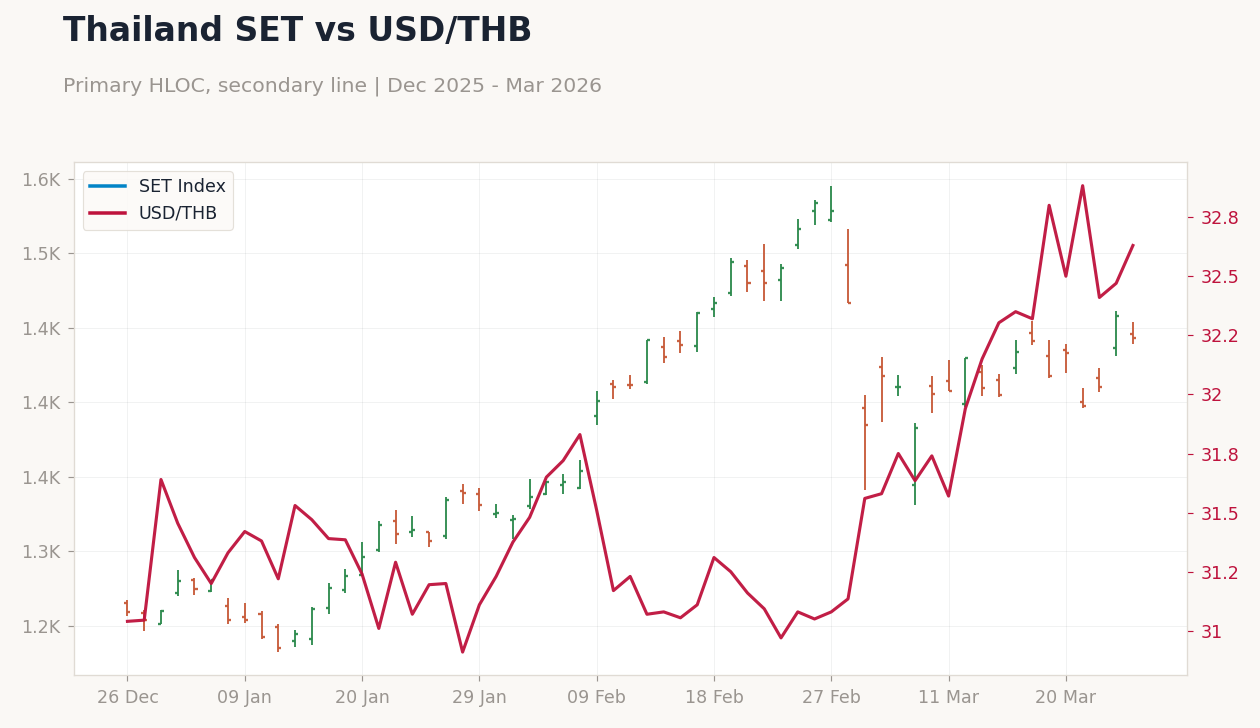

| SET | 1,442.92 | -1.03% |

| KLCI | 1,710.89 | -0.34% |

| PSEi | 5,984.20 | -0.99% |

| STI | 4,887.76 | -0.34% |

| USD/IDR | 16,898.00 | +0.60% |

| USD/THB | 32.63 | +0.49% |

| USD/MYR | 3.99 | +0.96% |

| USD/PHP | 60.14 | +0.20% |

| USD/SGD | 1.29 | +0.62% |

| Brent Crude | 101.26 | -0.94% |

| Gold | 4,376.90 | -3.80% |

| Bitcoin | 68,978.35 | -3.27% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Central Bank Interest Rate Decision | 4.25 | - | 4.25 |

Brent Crude Oil Prices | Type: macro_line | Brent Oil Price (USD): 103.8 (2026-03-23) | Range: 59.93–133.2 | Trend(5pt): 64.06,122.2,97.1,72.12,103.8

Brent Crude Oil Prices | Type: macro_line | Brent Oil Price (USD): 103.8 (2026-03-23) | Range: 59.93–133.2 | Trend(5pt): 64.06,122.2,97.1,72.12,103.8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Bank Indonesia held rates at 4.75% amid global war risks, while Philippines' BSP maintained 4.25% to support growth.

- ASEAN equities fell 0.3-1.9%, with currencies weakening 0.2-1.0% vs USD on profit-taking and oil volatility.

- News highlighted rupiah risks to 20,000/USD, driven by Middle East tensions and inflation fears.

Yesterday's Recap

ASEAN markets retreated yesterday amid profit-taking and global caution, with Indonesia's JCI dropping 1.89% to 7,164.09 as rupiah concerns dominated headlines. The Philippines' BSP held its key rate steady at 4.25%, aligning with consensus to balance inflation and growth amid an energy crisis declaration. Thailand's SET fell 1.03% to 1,442.92, pressured by fiscal strains from oil prices forcing an end to diesel caps.

Malaysia's KLCI edged down 0.34% to 1,710.89, though HSBC projected solid 2026 growth despite Middle East war risks. Singapore's STI dipped 0.34% to 4,887.76, reflecting broader regional caution. The Philippines' PSEi declined 0.99% to 5,984.20 on energy concerns.

Currencies weakened against the USD, led by USD/MYR up 0.96% to 3.99 and USD/IDR rising 0.60% to 16,898.00, reflecting capital outflows and commodity price swings, while Brent crude slipped 0.94% to 101.26. Gold fell 3.80% to 4,376.90, and Bitcoin dropped 3.27% to 68,978.35.

The Day Ahead

With no major data releases scheduled for today, markets will focus on ongoing geopolitical developments, particularly Middle East tensions influencing oil prices and ASEAN energy security. Traders may monitor Indonesia's rupiah movements, as forecasts suggest potential weakening near 16,932/USD amid sentiment triggers. Attention could shift to broader regional themes like Malaysia's economic resilience and Thailand's fiscal adjustments post-price cap removal.

Vietnam's manufacturing strength may draw FDI interest in a quiet session. Singapore, as the financial hub, might see flows tied to global risk appetite. Overall, expect subdued trading unless fresh global headlines emerge.

Other Economic Notes

Broader ASEAN themes underscore resilience amid external shocks, with Indonesia extending tax filing deadlines to April 30 to ease administrative burdens during cautious reopening. Oil-driven inflation risks are stymieing Indonesia's bond market boom, while the Philippines grapples with an energy crisis, prompting Indonesia to assure its own supplies remain secure. Structural shifts persist, as Malaysia benefits from positive growth outlooks and Thailand expands retail infrastructure with Central Pattana's $3.4 billion investment plan.

(cont...)