Yesterday's Recap

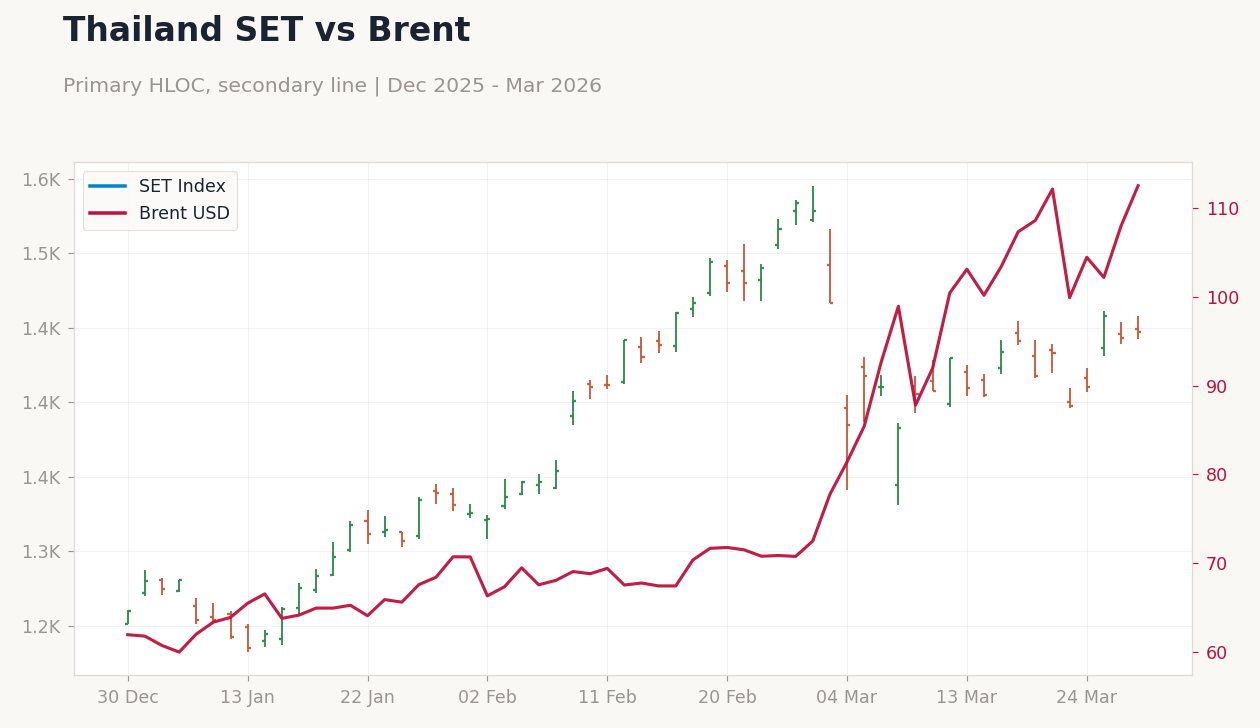

ASEAN equities closed mixed amid volatile global sentiment driven by Middle East tensions and oil price fluctuations. Indonesia's JCI fell 0.94% to 7,097.06, pressured by rupiah depreciation and geopolitical unease following the deaths of Indonesian UN peacekeepers in Lebanon, which heightened regional concerns. Thailand's SET rose 0.29% to 1,447.05, buoyed by tourism sector resilience despite fuel price hikes after subsidy reductions led to a 22% jump in domestic fuel costs.

Malaysia's KLCI edged up 0.10% to 1,712.65, supported by manufacturing stability even as the central bank warned of intensified risks from the conflict and held rates steady. The Philippines' PSEi dipped 0.19% to 5,972.83, reflecting inflation jitters and a downgraded growth forecast to 4.5% by ING due to higher oil prices eroding consumer demand. Singapore's STI gained 0.21% to 4,898.18, benefiting from its financial hub status amid safe-haven flows.

In FX markets, the USD/IDR climbed 0.16% to 16,952.00, underscoring ongoing rupiah weakness as Bank Indonesia bolstered defenses against external shocks. The USD/THB fell 0.55% to 32.78, showing baht strength possibly from export gains, while USD/MYR rose 0.86% to 4.03 amid rate hike expectations building over the next 12 months. USD/PHP increased 0.81% to 60.69, with the peso hit hard by the energy crisis and lack of subsidies, and USD/SGD advanced 0.43% to 1.29.

Commodities saw Brent crude drop 3.36% to 108.79 despite warnings of existential threats to Asian economies from Strait of Hormuz disruptions, which could exacerbate supply chain issues. Gold rose 1.08% to 4,540.40 as a safe haven, and Bitcoin climbed 1.43% to 66,895.34 on broader risk appetite. No major economic data releases occurred yesterday, but news highlighted Australia's reluctance to disclose Chinese boat arrivals, potentially linked to Indonesia's reports of organizing attempts, adding to migration and bilateral tensions.

Overall, the session reflected a cautious tone with focus on Indonesia and Philippines as particularly vulnerable to oil-driven pressures.

The Day Ahead

Attention turns to Indonesia's key releases at 20:00 ET, including the inflation rate year-over-year (previous: 4.76%) and trade balance (previous: 960,000,000.00), both critical for assessing Bank Indonesia's stance amid mounting rupiah pressures and oil price volatility. (cont...)

Brent Oil Price | Type: macro_line | Brent Crude Oil USD: 103.8 (2026-03-23) | Range: 59.93–133.2 | Trend(6pt): 63.52,120.8,97.1,73.19,118.4,103.8

Brent Oil Price | Type: macro_line | Brent Crude Oil USD: 103.8 (2026-03-23) | Range: 59.93–133.2 | Trend(6pt): 63.52,120.8,97.1,73.19,118.4,103.8