ASEAN Macro Daily(Beta Mode)

Indonesian Inflation Eases, Rupiah Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 7,184.44 | +1.93% |

| SET | 1,470.99 | +1.58% |

| KLCI | 1,708.90 | +1.10% |

| PSEi | 5,998.68 | +0.84% |

| STI | 4,975.83 | +1.85% |

| USD/IDR | 17,010.00 | +0.43% |

| USD/THB | 32.61 | +0.31% |

| USD/MYR | 4.04 | -0.26% |

| USD/PHP | 60.33 | -0.41% |

| USD/SGD | 1.28 | +0.03% |

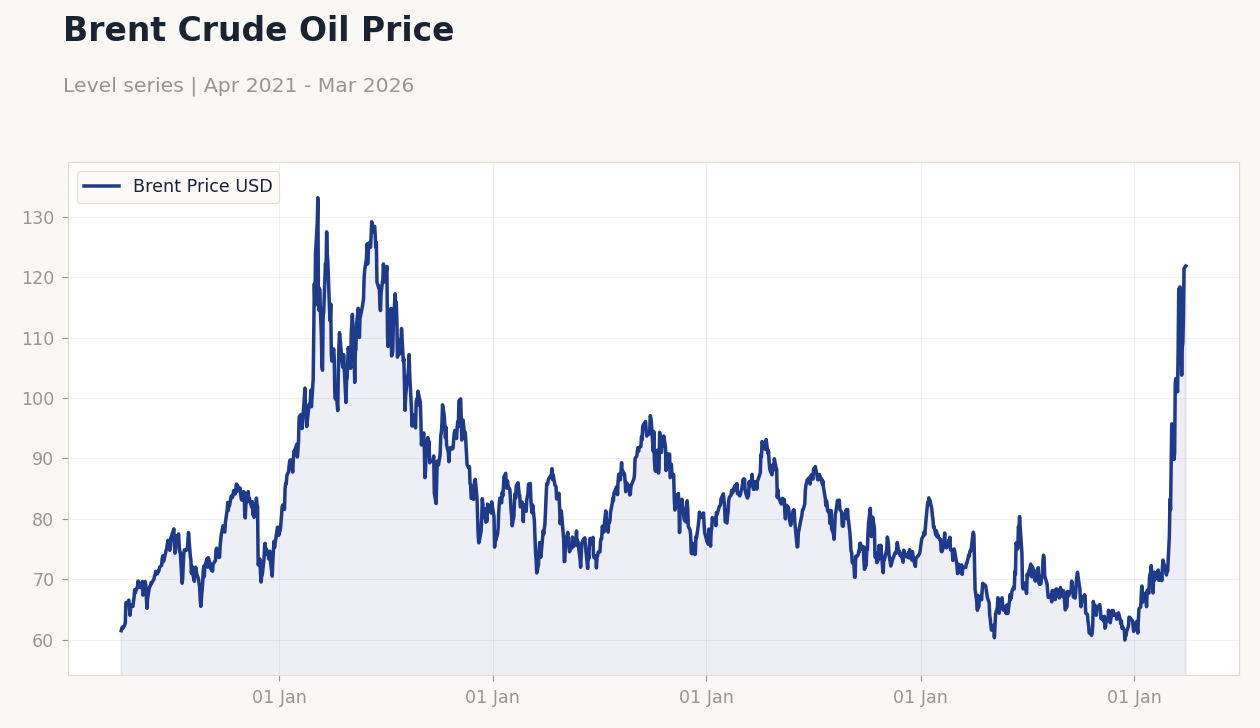

| Brent Crude | 109.05 | +7.80% |

| Gold | 4,702.70 | -1.68% |

| Bitcoin | 66,962.07 | -1.64% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 4.76 | 3.60 | 3.48 |

| Trade Balance | 960m | 1,550m | 1,280m |

Brent Crude Oil Price | Type: macro_line | Brent Price USD: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(5pt): 61.47,121.8,94.46,74.58,121.9

Brent Crude Oil Price | Type: macro_line | Brent Price USD: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(5pt): 61.47,121.8,94.46,74.58,121.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Indonesia's March inflation eased to 3.48% YoY, below consensus of 3.60%, signaling cooling price pressures amid stable food costs.

- Trade balance came in at $1.28 billion surplus, missing expectations of $1.55 billion, as export growth slowed to 1.01% amid wider trade challenges.

- Rupiah weakened beyond 17,000/USD on geopolitical strains and budget deficit fears, while ASEAN equities rallied on commodity gains.

Yesterday's Recap

Indonesia dominated ASEAN macro news with March inflation dropping to 3.48% YoY, undercutting forecasts and prior 4.76%, driven by moderated food and energy prices despite subsidy expansions. The trade surplus came in at $1.28 billion, below consensus, reflecting slower export momentum in commodities like nickel and palm oil amid global demand softness. Rupiah depreciation persisted, with USD/IDR rising 0.43% to 17,010, pressured by Middle East tensions and fiscal concerns, though Bank Indonesia's reforms drew positive index provider feedback.

Equity markets across the region advanced, led by Indonesia's JCI up 1.93% to 7,184.44 on mining gains, Singapore's STI +1.85% to 4,975.83 buoyed by financials, and Thailand's SET +1.58% to 1,470.99 amid tourism optimism. Malaysia's KLCI rose 1.10% to 1,708.90, supported by energy stocks as Brent crude surged 7.80% to $109.05, while Philippines' PSEi gained 0.84% to 5,998.68 on remittance inflows. Vietnam saw steady manufacturing activity, though not detailed in releases, contributing to regional supply chain resilience.

The Day Ahead

No major ASEAN data releases are scheduled for today, allowing markets to digest yesterday's Indonesian figures and global risk cues. Attention turns to potential FX interventions, especially in Indonesia where rupiah weakness tests BI's defenses. Thailand may see follow-up on BoT's cash transaction crackdown, impacting informal sectors.

Broader events include monitoring cross-border payment integrations, like Indonesia's QRIS launch with South Korea, which could boost tourism and trade flows. Singapore's financial hub status may highlight any MAS commentary on NEER bands amid USD strength. Overall, quiet calendar shifts focus to geopolitical developments influencing commodity prices and ASEAN exports.

Other Economic Notes

ASEAN economies continue navigating supply chain shifts from China and US tensions, with Vietnam and Malaysia attracting FDI in semiconductors and electronics. Indonesia's energy subsidy hike by Rp100 trillion underscores fiscal strains from oil volatility, potentially widening deficits in commodity-reliant nations. Thailand's push toward electric vehicles accelerates amid high oil prices, aligning with regional green transitions but challenging traditional auto sectors.