ASEAN Macro Daily(Beta Mode)

PH Inflation Spikes, Rupiah Hits 17k

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 7,279.21 | +4.42% |

| SET | 1,485.03 | +1.41% |

| KLCI | 1,696.31 | +1.16% |

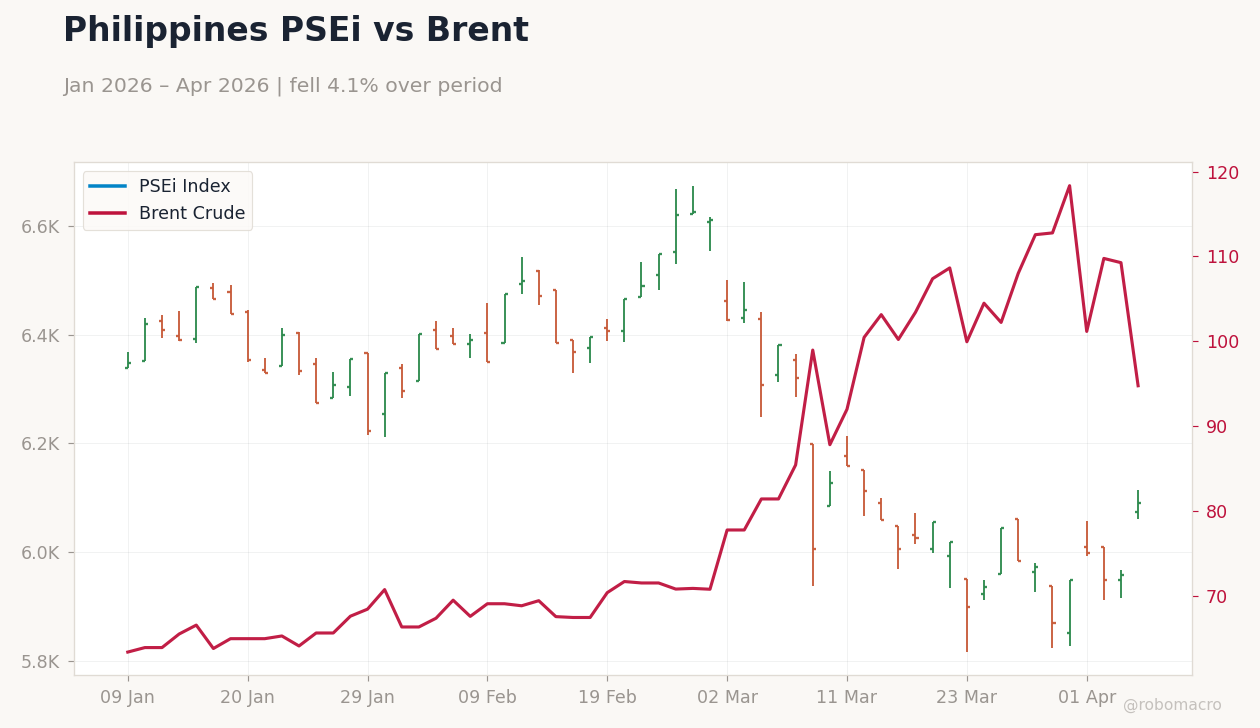

| PSEi | 6,089.91 | +2.22% |

| STI | 4,996.05 | +0.77% |

| USD/IDR | 17,077.00 | +0.29% |

| USD/THB | 31.88 | -0.59% |

| USD/MYR | 3.98 | -1.20% |

| USD/PHP | 59.66 | -0.32% |

| USD/SGD | 1.27 | -0.28% |

| Brent Crude | 96.44 | +1.78% |

| Gold | 4,790.50 | +0.86% |

| Bitcoin | 72,318.18 | +1.68% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2.40 | 3.60 | 4.10 |

| Headline Unemployment Rate | 5.80 | - | 5.10 |

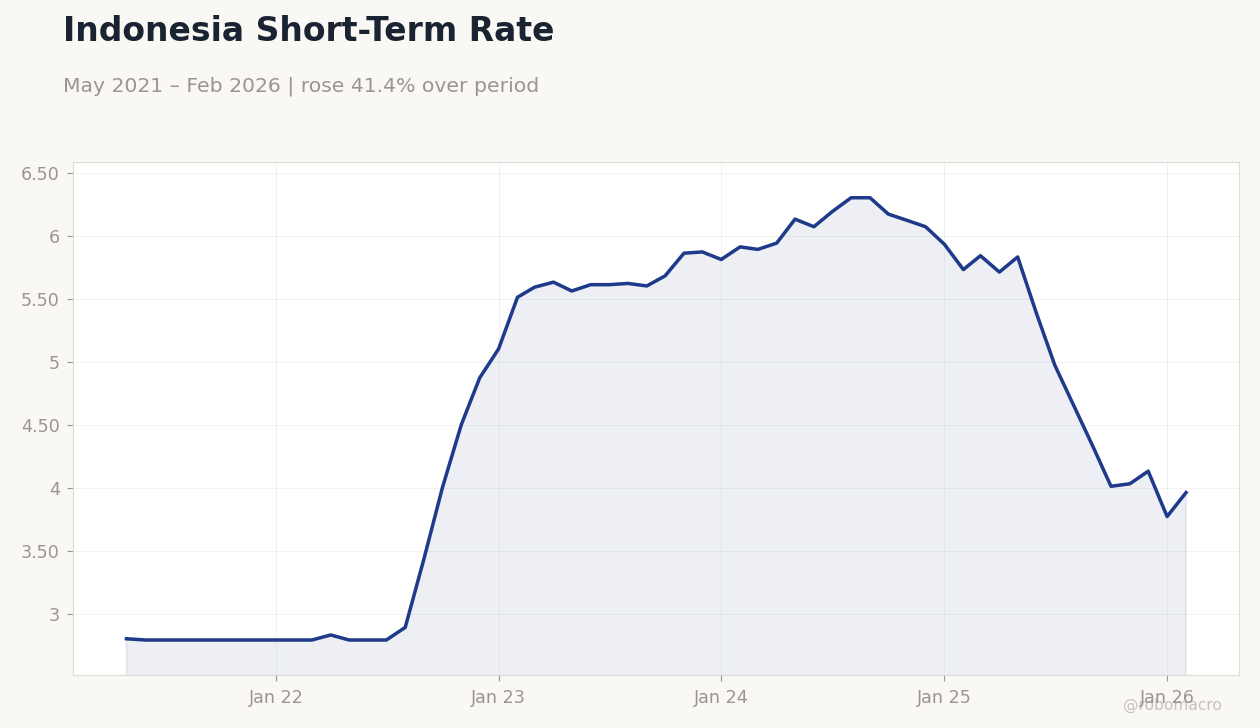

Indonesia Short-Term Rate | Type: macro_line | Indonesia Short-Term Rate: 3.96 (2026-02-01) | Range: 2.79–6.3 | Trend(6pt): 2.8,2.79,5.6,6.12,3.77,3.96

Indonesia Short-Term Rate | Type: macro_line | Indonesia Short-Term Rate: 3.96 (2026-02-01) | Range: 2.79–6.3 | Trend(6pt): 2.8,2.79,5.6,6.12,3.77,3.96

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Philippines inflation accelerated to 4.1% YoY, exceeding consensus, while unemployment fell to 5.1%, signaling mixed labor market dynamics.

- Indonesian rupiah weakened past 17,000 amid BI's stability focus, with equities rallying across ASEAN on commodity gains.

- Thai central bank pledged extended rate pause to bolster economy, as regional currencies faced USD pressure.

Yesterday's Recap

Philippines dominated data releases with inflation surging to 4.1% year-over-year, beating consensus of 3.6% and prior 2.4%, driven by food and energy costs amid global tensions. The country's headline unemployment rate improved to 5.1% from 5.8%, reflecting stronger job creation in services and manufacturing sectors. Indonesian equities led gains as the JCI climbed 4.42% to 7,279.21, supported by commodity exporters, while the rupiah depreciated 0.29% to 17,077 against the USD following BI's intervention signals.

Thai stocks rose 1.41% on the SET to 1,485.03, buoyed by tourism recovery hopes, though the baht strengthened 0.59% with USD/THB at 31.88 amid BoT's supportive stance. Malaysian and Philippine benchmarks advanced, with KLCI up 1.16% to 1,696.31 and PSEi up 2.22% to 6,089.91, while Singapore's STI gained 0.77% to 4,996.05. Vietnam saw no major equity moves reported, but broader ASEAN markets benefited from Brent crude rising 1.78% to 96.44, offsetting FX volatility.

Overall, resource-driven economies like Indonesia outperformed, with total ASEAN equity gains tempered by currency pressures.

The Day Ahead

With no major ASEAN data releases scheduled for today, attention turns to potential FX interventions, particularly in Indonesia where the rupiah's breach of 17,000 may prompt BI action. Thailand's markets could react to ongoing BoT commentary on rate pauses and debt relief measures for households. Malaysia's ringgit recovery from recent lows might stabilize further, influenced by BNM's reserve management amid FX pressures.

In the Philippines, post-inflation sentiment could shape BSP expectations ahead of any policy signals. Singapore and Vietnam face a quiet calendar, allowing focus on global cues like US economic data. Broader events include monitoring commodity prices, with Brent's rally potentially supporting export-heavy sectors across the region.

Other Economic Notes

ASEAN economies exhibit resilience amid global uncertainty, with Indonesia's government optimistic about strong growth driven by commodity exports despite rupiah weakness. Supply chain shifts continue favoring Vietnam as a manufacturing hub, though World Bank projections highlight vulnerability for Vietnam and Thailand to external shocks in 2026. (cont...)