ASEAN Macro Daily(Beta Mode)

SG GDP Beats, Rupiah Pressured

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 7,500.19 | +0.56% |

| SET | 1,506.84 | +1.15% |

| KLCI | 1,680.52 | -0.64% |

| PSEi | 6,054.05 | -0.72% |

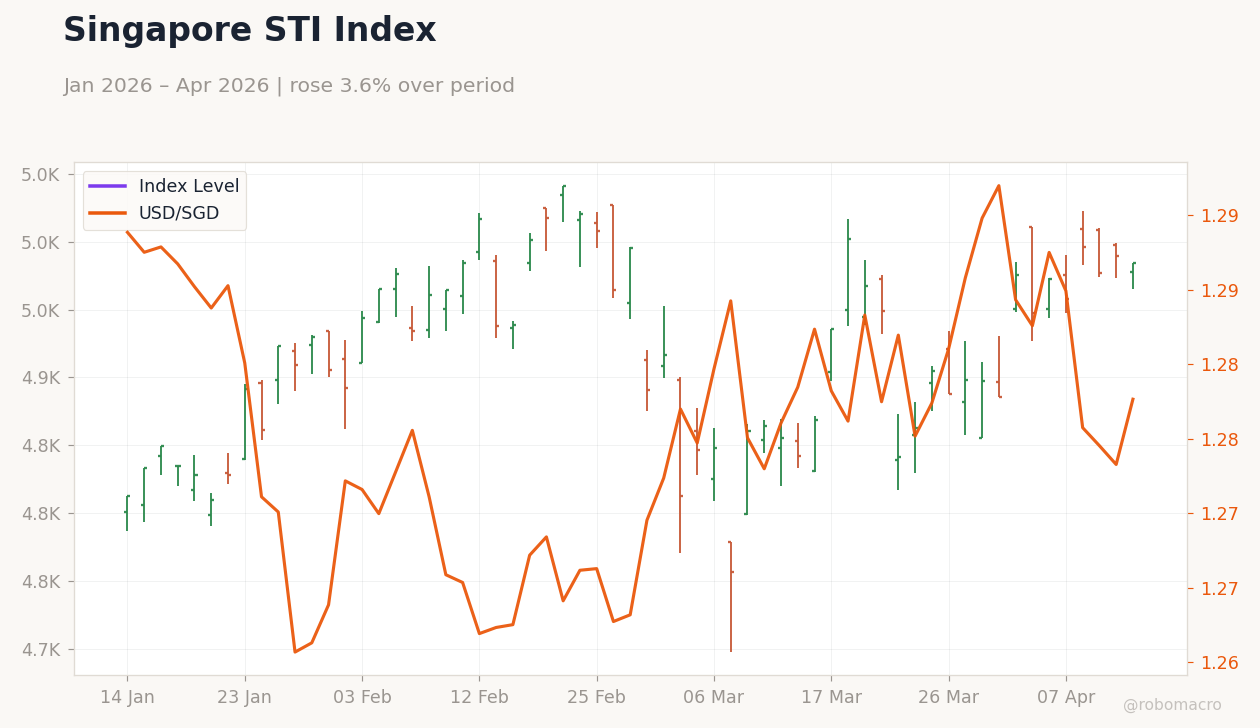

| STI | 4,984.17 | -0.11% |

| USD/IDR | 17,130.00 | +0.28% |

| USD/THB | 31.91 | -1.27% |

| USD/MYR | 3.95 | -0.72% |

| USD/PHP | 59.82 | -0.19% |

| USD/SGD | 1.27 | -0.52% |

| Brent Crude | 95.14 | -4.25% |

| Gold | 4,864.50 | +2.57% |

| Bitcoin | 74,227.00 | -0.35% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter Advance Estimate | 1.30 | -0.50 | -0.30 |

USD/IDR vs Brent | Type: market_hloc | Exchange Rate: 1.713e+04 (2026-04-14) | Range: 1.667e+04–1.713e+04 | Trend(5pt): 1.684e+04,1.68e+04,1.675e+04,1.696e+04,1.713e+04 | Brent Price: 95.52 (2026-04-14) | Range: 63.76–118.3 | Trend(6pt): 66.52,67.55,72.48,112.2,99.36,95.52

USD/IDR vs Brent | Type: market_hloc | Exchange Rate: 1.713e+04 (2026-04-14) | Range: 1.667e+04–1.713e+04 | Trend(5pt): 1.684e+04,1.68e+04,1.675e+04,1.696e+04,1.713e+04 | Brent Price: 95.52 (2026-04-14) | Range: 63.76–118.3 | Trend(6pt): 66.52,67.55,72.48,112.2,99.36,95.52

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Month-over-Month | 0.20 | - | 00:00 |

| Inflation Rate Year-over-Year | 1.40 | 1.70 | 00:00 |

- Singapore's Q1 GDP advance estimate contracted -0.3% QoQ, beating consensus of -0.5%, amid resilient services offsetting manufacturing weakness.

- Indonesian rupiah weakened to 17,130 amid geopolitical tensions and oil volatility, while Thai baht strengthened on tourism inflows.

- ASEAN equities mixed: Thailand's SET +1.15%, Indonesia's JCI +0.56%, but Malaysia's KLCI -0.64% on energy concerns.

Yesterday's Recap

Singapore dominated headlines with its Q1 GDP advance estimate showing a milder-than-expected contraction of -0.3% QoQ against consensus -0.5% and previous 1.3%, reflecting strength in financial services and tourism despite global trade headwinds. Indonesia's equity market, the JCI, rose 0.56% to 7,500.19, supported by banking sector gains as Bank Indonesia emphasized policy stability amid oil prices above $100, though USD/IDR climbed 0.28% to 17,130.00 on Trump-related threats to Hormuz Strait. Thailand's SET advanced 1.15% to 1,506.84, buoyed by tourism recovery and a 1.27% baht appreciation to 31.91 against USD, while Malaysia's KLCI fell 0.64% to 1,680.52 amid concerns over global energy shocks.

Philippines' PSEi dropped 0.72% to 6,054.05, tracking broader EM caution, and Singapore's STI edged down 0.11% to 4,984.17 despite the positive GDP surprise. Vietnam saw no major data releases, but its markets remained stable amid reports of dong stabilization efforts. Overall, Brent crude's 4.25% plunge to 95.14 weighed on commodity-linked currencies, while gold surged 2.57% to 4,864.50 as a safe haven.

The Day Ahead

Attention turns to Malaysia's upcoming inflation data on April 17, with YoY rate consensus at 1.7% versus previous 1.4%, potentially signaling persistent price pressures from energy imports. MoM inflation for Malaysia lacks a consensus but follows 0.2% prior, which could influence BNM's outlook amid resilient domestic growth. No major releases are scheduled for April 15, allowing markets to digest global cues like US-Iran tensions.

Investors will monitor any ASEAN central bank commentary on FX volatility, especially from BI given rupiah weakness. Broader events include potential updates on Indonesia-Saudi creative economy ties, which may boost FDI sentiment. Vietnam's SBV could provide further signals on liquidity measures to support the dong.

Other Economic Notes

Geopolitical risks from the US-Iran war are delivering mixed impacts across ASEAN, with Indonesia facing a double-edged sword from high oil prices boosting exports but raising import costs, as noted by Bank Indonesia. Retail sales in Indonesia surged despite energy woes, highlighting domestic consumption resilience in the region's largest economy. (cont...)