ASEAN Macro Daily(Beta Mode)

Rupiah Firms Pre-BI Decision

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 7,594.11 | -0.52% |

| SET | 1,481.85 | -0.04% |

| KLCI | 1,702.30 | +0.42% |

| PSEi | 6,016.03 | +0.28% |

| STI | 5,004.07 | +0.12% |

| USD/IDR | 17,137.00 | +0.02% |

| USD/THB | 32.15 | +0.06% |

| USD/MYR | 3.95 | -0.05% |

| USD/PHP | 59.94 | +0.65% |

| USD/SGD | 1.27 | +0.00% |

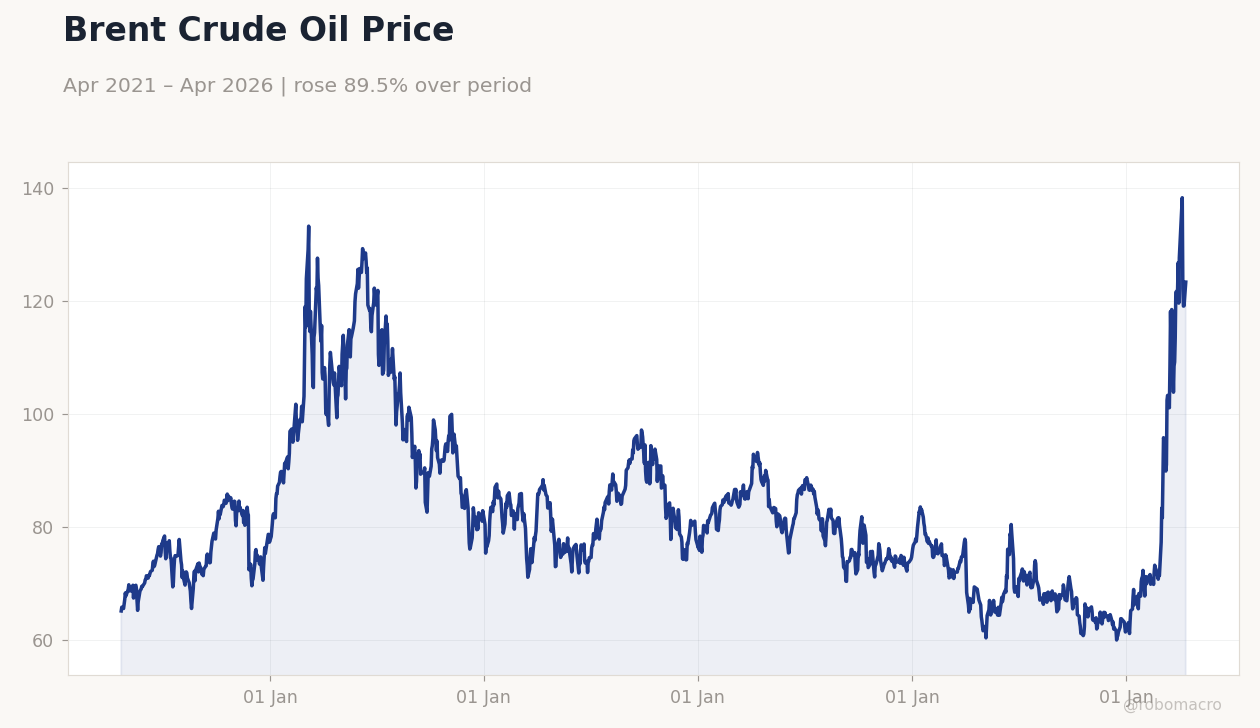

| Brent Crude | 93.52 | -2.05% |

| Gold | 4,744.90 | -1.28% |

| Bitcoin | 75,584.70 | -0.38% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Oil Price | Type: macro_line | USD per Barrel: 123.3 (2026-04-13) | Range: 59.93–138.2 | Trend(5pt): 65.07,115,92.52,82.39,123.3

Brent Crude Oil Price | Type: macro_line | USD per Barrel: 123.3 (2026-04-13) | Range: 59.93–138.2 | Trend(5pt): 65.07,115,92.52,82.39,123.3

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Central Bank Interest Rate Decision | 4.75 | 4.75 | 23:30 |

| Central Bank Interest Rate Decision | 4.25 | - | 22:30 |

| Wednesday (2026-04-22) | |||

| Central Bank Interest Rate Decision | 4.75 | 4.75 | 23:30 |

- Rupiah strengthens ahead of Bank Indonesia's expected rate hold at 4.75%, amid inflation risks from Iran tensions and fuel price hikes.

- ASEAN equities mixed; JCI down 0.52% on commodity weakness, KLCI up 0.42% on ringgit resilience.

- Thailand's outlook upgraded to stable by Moody's, while Malaysia eyes 4.8% export growth.

Yesterday's Recap

ASEAN markets closed mixed on April 20, with no major data releases, as investors awaited central bank decisions in Indonesia and the Philippines. Indonesia's JCI fell 0.52% to 7,594.11, pressured by commodity sectors amid Brent crude's 2.05% drop to 93.52, though rupiah firmed with USD/IDR up just 0.02% to 17,137.00 ahead of BI's meeting. Thailand's SET dipped 0.04% to 1,481.85, reflecting caution despite Moody's upgrade to stable outlook, while USD/THB rose 0.06% to 32.15.

Malaysia's KLCI gained 0.42% to 1,702.30, supported by ringgit strength with USD/MYR down 0.05% to 3.95 and positive export growth forecasts at 4.8%. Philippines' PSEi rose 0.28% to 6,016.03, but USD/PHP climbed 0.65% to 59.94 amid broader FX pressures. Singapore's STI edged up 0.12% to 5,004.07, with USD/SGD flat at 1.27.

Vietnam saw no major equity moves reported but benefited from regional supply chain shifts.

The Day Ahead

Focus shifts to Bank Indonesia's rate decision at 23:30 ET on April 21, with consensus expecting a hold at 4.75% due to inflation from global tensions. The Philippines' BSP decision follows on April 22 at 22:30 ET, with previous rate at 4.25% and no consensus available, potentially shaped by currency weakness. No other major ASEAN data is scheduled, leaving markets to react to global factors like Brent volatility.

Investors will watch BI statements on rupiah stability and possible FX interventions. Updates on Thailand's debt ceiling plans, including potential 500 billion baht borrowing, may influence THB sentiment.

Other Economic Notes

ASEAN economies display divergence, with Indonesia's commodity resilience evident in rupiah gains from fuel price hikes, contrasting broader FX pressures. Thailand's fiscal moves, such as plans to borrow 500 billion baht and lift debt ceilings for $30 billion, aim to address economic challenges amid Moody's stable outlook. Malaysia's ringgit is poised to test 2026 highs on strong fundamentals and 4.8% export growth projections.

Supply chain developments include Thailand's accelerated landbridge project to bypass Malacca Strait risks, enhancing trade resilience. Bangladesh's agent banking shows two-thirds of outlets not engaged in lending, highlighting regional credit gaps. (cont...)