ASEAN Macro Daily(Beta Mode)

BoT Holds, Rupiah Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 7,072.39 | -0.48% |

| SET | 1,480.20 | +0.07% |

| KLCI | 1,729.60 | +0.72% |

| PSEi | 5,866.79 | -0.58% |

| STI | 4,887.69 | -0.10% |

| USD/IDR | 17,319.00 | +0.60% |

| USD/THB | 32.75 | +1.24% |

| USD/MYR | 3.95 | -0.02% |

| USD/PHP | 61.57 | +1.35% |

| USD/SGD | 1.28 | +0.55% |

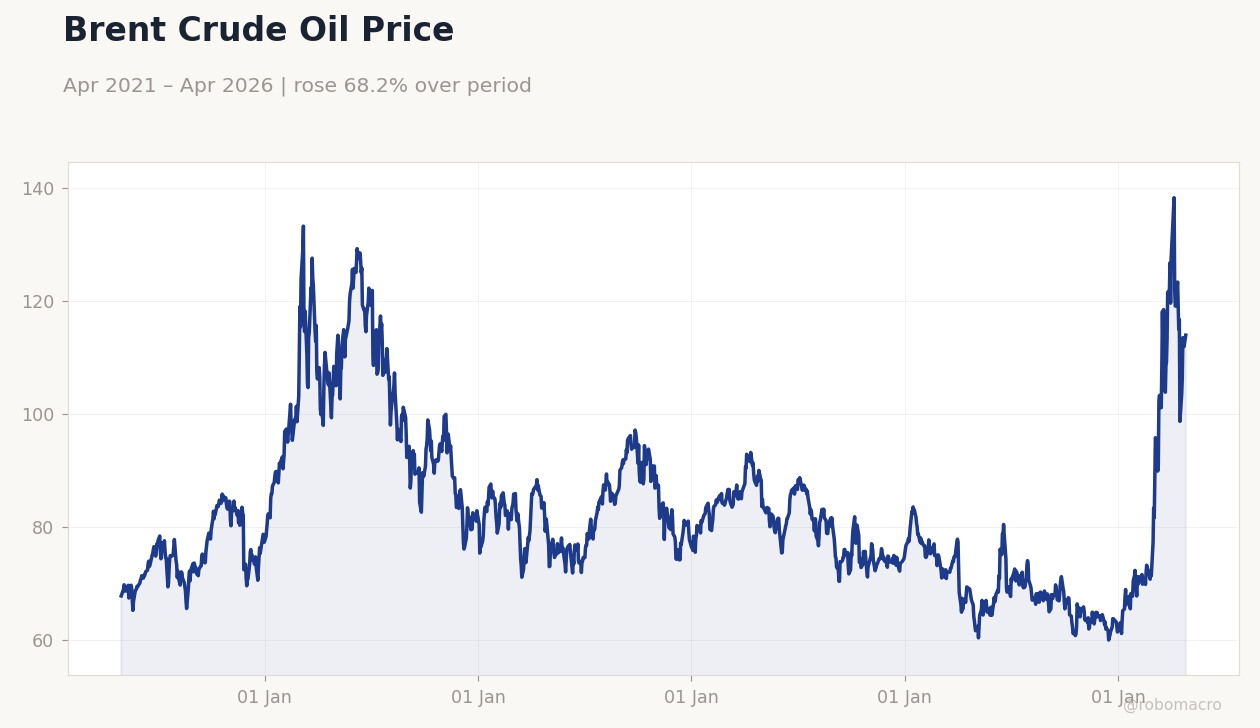

| Brent Crude | 111.91 | +0.58% |

| Gold | 4,557.30 | -0.74% |

| Bitcoin | 75,922.81 | -0.56% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Central Bank Interest Rate Decision | 1 | 1 | 1 |

Brent Crude Oil Price | Type: macro_line | Brent Crude Price (USD): 113.9 (2026-04-27) | Range: 59.93–138.2 | Trend(5pt): 67.73,109.7,90.73,77.3,113.9

Brent Crude Oil Price | Type: macro_line | Brent Crude Price (USD): 113.9 (2026-04-27) | Range: 59.93–138.2 | Trend(5pt): 67.73,109.7,90.73,77.3,113.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Bank of Thailand holds key rate at 1% amid oil shocks and growth cuts, signaling caution on economic recovery.

- Indonesian rupiah slides to 17,319/USD, pressuring BI to delay rate cuts as triple shocks from oil, FX, and costs hit.

- ASEAN equities mixed; Thai stocks edge up post-BoT decision, while Indonesian and Philippine indices dip on FX strains.

Yesterday's Recap

Thailand's Bank of Thailand (BoT) held its key interest rate at 1%, aligning with consensus and previous levels, as it assesses oil price impacts and downgrades 2026 growth to 1.5% and 2027 to 2.0% amid Mideast tensions. Indonesia dominated headlines with the rupiah weakening 0.60% to 17,319/USD, nearing 17,500, driven by oil topping $100, rising costs, and global risk-off sentiment, prompting warnings of delayed BI rate cuts. Equity markets were mixed: Indonesia's JCI fell 0.48% to 7,072.39 on currency pressures, while Thailand's SET rose 0.07% to 1,480.20 buoyed by the rate hold.

Malaysia's KLCI gained 0.72% to 1,729.60, supported by energy stocks amid higher Brent at $111.91 (+0.58%). The Philippines' PSEi dropped 0.58% to 5,866.79, with USD/PHP up 1.35% to 61.57 reflecting broader ASEAN FX strains. Singapore's STI edged down 0.10% to 4,887.69, and other currencies like USD/THB rose 1.24% to 32.75.

Vietnam saw limited data, but regional durian export gluts highlighted agricultural vulnerabilities in Thailand.

The Day Ahead

With no major data releases scheduled for today, markets will focus on digesting yesterday's BoT decision and monitoring FX volatility, particularly in Indonesia where rupiah pressures could intensify. Attention turns to global cues, including any U.S. economic signals that might strengthen the dollar further against ASEAN currencies.

In Thailand, ongoing assessments of tourism recovery and manufacturing slowdowns may influence sentiment without fresh indicators. Broader ASEAN events remain light, allowing traders to eye commodity moves like Brent crude amid Mideast risks. Vietnam and Singapore could see quiet trading, with potential spillover from regional FX dynamics.

Upcoming weeks may bring more clarity on trade data, but today's calendar is empty.

Other Economic Notes

ASEAN economies face mounting pressures from elevated oil prices and USD strength, exacerbating import costs in commodity importers like Thailand and the Philippines while benefiting exporters in Indonesia and Malaysia. Supply chain shifts continue, with Vietnam and Malaysia attracting FDI in semiconductors and electronics amid U.S.-China tensions, though slower inflows signal caution. Tourism-dependent Thailand grapples with durian gluts and weaker Chinese demand, underscoring vulnerabilities in agriculture and services sectors.

(cont...)