ASEAN Macro Daily(Beta Mode)

BI Defends Rupiah Amid Energy Crisis

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 6,956.80 | -2.03% |

| SET | 1,493.69 | +0.13% |

| KLCI | 1,722.02 | +0.09% |

| PSEi | 5,833.64 | -1.26% |

| STI | 4,912.69 | +1.06% |

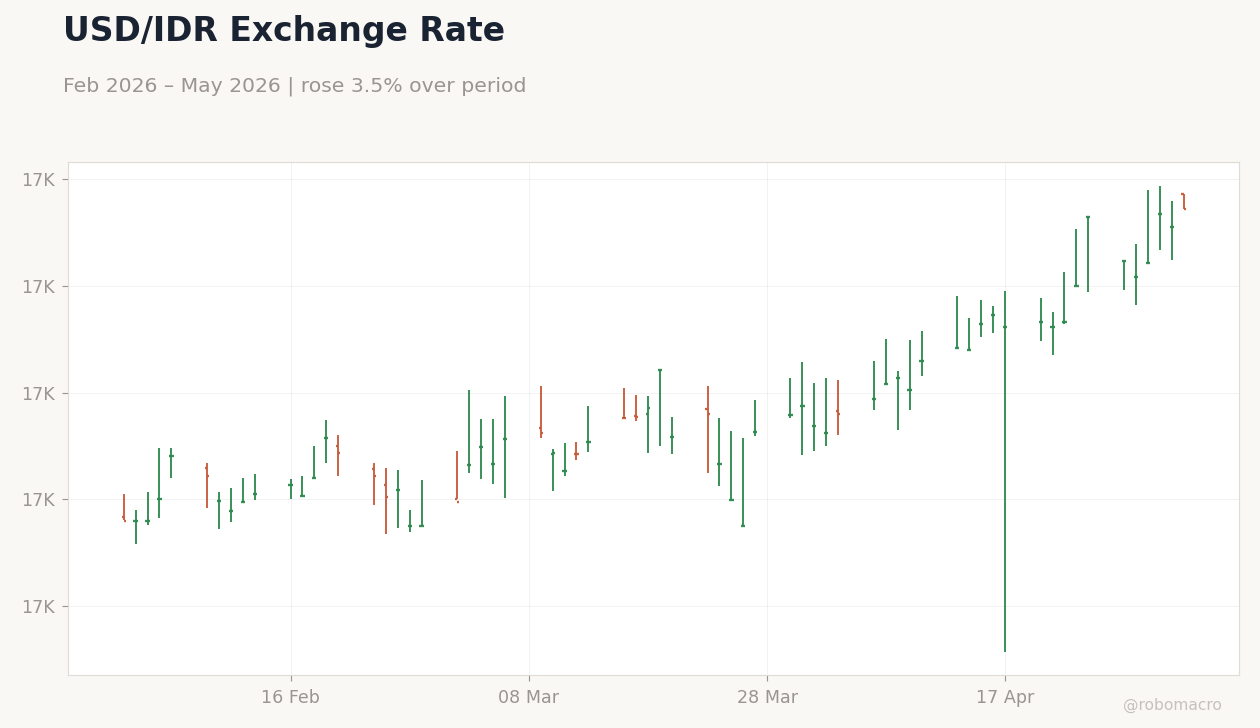

| USD/IDR | 17,345.00 | +0.20% |

| USD/THB | 32.33 | -0.52% |

| USD/MYR | 3.97 | +0.01% |

| USD/PHP | 61.45 | +0.22% |

| USD/SGD | 1.27 | +0.04% |

| Brent Crude | 108.17 | -5.12% |

| Gold | 4,644.50 | +0.65% |

| Bitcoin | 79,083.61 | +0.54% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Oil Price | Type: market_hloc | Brent Price: 108.2 (2026-05-03) | Range: 67.33–118.3 | Trend(6pt): 67.33,70.85,107.4,95.92,114,108.2

Brent Crude Oil Price | Type: market_hloc | Brent Price: 108.2 (2026-05-03) | Range: 67.33–118.3 | Trend(6pt): 67.33,70.85,107.4,95.92,114,108.2

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | 1,280m | - | 00:00 |

| Inflation Rate Year-over-Year | 3.48 | - | 00:00 |

| Inflation Rate Year-over-Year | 4.10 | - | 21:00 |

| GDP Growth Year-over-Year | 5.39 | 5.30 | 00:00 |

| Headline Unemployment Rate | 5.10 | - | 21:10 |

| GDP Growth Quarter-over-Quarter | 0.60 | - | 22:00 |

| GDP Growth Year-over-Year | 3 | - | 22:00 |

- Rupiah weakens on global energy risks; BI unveils stability measures.

- Mixed ASEAN equities: JCI down 2%, STI up 1% on commodity volatility.

- Malaysia's ringgit strength signals IMF-backed economic confidence.

Yesterday's Recap

ASEAN equity markets displayed mixed results on May 2, with Indonesia's JCI declining 2.03% to 6,956.80 due to rupiah pressures from a global energy crisis and Brent crude's 5.12% drop to $108.17. Thailand's SET rose 0.13% to 1,493.69, aided by tourism recovery indicators, while Malaysia's KLCI increased 0.09% to 1,722.02 amid positive IMF upgrades and ringgit gains. The Philippines' PSEi fell 1.26% to 5,833.64, reflecting risk aversion, whereas Singapore's STI advanced 1.06% to 4,912.69, supported by financial sector performance.

FX movements included USD/IDR rising 0.20% to 17,345.00 despite BI interventions, USD/THB declining 0.52% to 32.33 on export strength, USD/MYR edging up 0.01% to 3.97, USD/PHP increasing 0.22% to 61.45, and USD/SGD rising 0.04% to 1.27. Gold climbed 0.65% to $4,644.50 for haven appeal, while Bitcoin rose 0.54% to $79,083.61, boosting tech sentiment in Singapore. Commodity swings and currency defenses shaped the session, with Indonesia central amid its exposure.

The Day Ahead

Key releases include Indonesia's trade balance on May 4, with prior surplus at $1.28 billion potentially aiding rupiah via exports. Indonesia's YoY inflation, previous at 3.48%, follows, informing BI policy. Philippines' YoY inflation, prior at 4.1%, is due later on May 4, affecting BSP views on consumption.

Indonesia's YoY GDP growth, consensus 5.3% vs. previous 5.39%, arrives on May 5, spotlighting commodities and manufacturing. Philippines' unemployment rate, last at 5.1%, and GDP data on May 6 (QoQ previous 0.6%, YoY 3%) will assess labor and recovery.

These could spur FX and equity moves in ASEAN.

Other Economic Notes

ASEAN trends feature supply chain evolution, with Thailand targeting foreign capital via private trust reforms to attract investment. Indonesia's cross-border QRIS launch with China enhances tourism and payments, supporting trade. Malaysia tests ringgit stablecoins with banks, fostering digital finance innovation.

Thailand remains on US trade watch list, prompting stricter IP enforcement against piracy to safeguard FDI. Indonesia plans to cap ride-hailing commissions at 8% for drivers, aiding gig economy fairness. These initiatives highlight regional efforts in diversification and cooperation amid global tensions.