ASEAN Macro Daily(Beta Mode)

ID CPI Eases, Rupiah Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 6,956.80 | -2.03% |

| SET | 1,493.69 | +0.13% |

| KLCI | 1,722.02 | +0.09% |

| PSEi | 5,833.64 | -1.26% |

| STI | 4,912.69 | +1.06% |

| USD/IDR | 17,363.00 | +0.30% |

| USD/THB | 32.72 | +0.68% |

| USD/MYR | 3.95 | -0.44% |

| USD/PHP | 61.56 | +0.41% |

| USD/SGD | 1.28 | +0.29% |

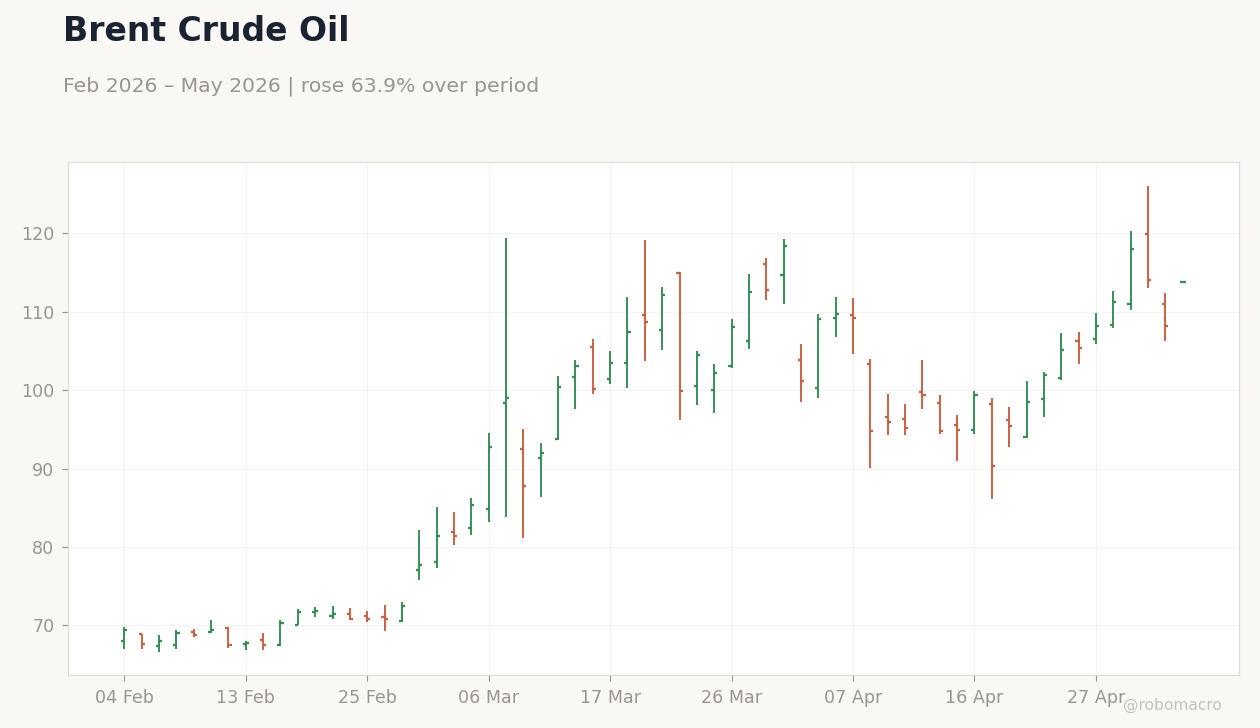

| Brent Crude | 113.76 | +5.17% |

| Gold | 4,532.40 | -2.11% |

| Bitcoin | 80,283.24 | +2.22% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 3.48 | - | 2.42 |

| Trade Balance | 1,280m | - | 3,320m |

Indonesia Industrial Production YoY | Type: macro_line | Indonesia Industrial Prod: 5.21 (2026-02-01) | Range: -3.835–19.33 | Trend(5pt): 13.46,-0.8528,12,3.282,5.21

Indonesia Industrial Production YoY | Type: macro_line | Indonesia Industrial Prod: 5.21 (2026-02-01) | Range: -3.835–19.33 | Trend(5pt): 13.46,-0.8528,12,3.282,5.21

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 4.10 | 5.50 | 21:00 |

| GDP Growth Year-over-Year | 5.39 | 5.30 | 00:00 |

| Headline Unemployment Rate | 5.10 | - | 21:10 |

| GDP Growth Quarter-over-Quarter | 0.60 | - | 22:00 |

| GDP Growth Year-over-Year | 3 | 3.70 | 22:00 |

- Indonesia Apr CPI fell to 2.42% YoY (prev 3.48%), trade surplus swelled to $3.32B (prev $1.28B), but rupiah hit 17,363/USD amid BI interventions.

- ASEAN equities mixed: JCI -2.03%, STI +1.06%; Brent surged 5.17% to $113.76 on energy risks.

- Philippines CPI due tonight; ID Q1 GDP tomorrow signals slower 5.3% YoY growth.

Yesterday's Recap

Indonesia dominated with April CPI dropping to 2.42% YoY from 3.48%, signaling disinflation amid lower food prices, easing pressure on Bank Indonesia. March trade balance surprised at $3.32B surplus versus $1.28B prior, driven by commodity exports despite global energy headwinds. Rupiah weakened 0.30% to 17,363/USD, prompting BI to unveil FX support measures and aggressively defend the currency amid US-Iran tensions and 1998 crisis echoes.

Equities diverged: Indonesia's JCI fell 2.03% to 6,956.80 on rupiah fears; Thailand's SET edged up 0.13% to 1,493.69; Malaysia's KLCI +0.09% to 1,722.02; Philippines' PSEi -1.26% to 5,833.64; Singapore's STI +1.06% to 4,912.69. Regional FX broadly softer: USD/THB +0.68% to 32.72, USD/PHP +0.41% to 61.56, USD/SGD +0.29% to 1.28, but USD/MYR -0.44% to 3.95. Brent crude rallied 5.17% to $113.76, boosting commodity plays but fueling inflation worries.

The Day Ahead

Philippines April CPI (exp 5.5%, prev 4.1%) prints at 21:00 ET tonight, with upside risks from energy costs potentially pressuring BSP. Indonesia Q1 GDP YoY (exp 5.3%, prev 5.39%) releases at 00:00 ET tomorrow, watched for manufacturing strain as rupiah nears 17,400. Philippines unemployment (prev 5.1%) follows at 21:10 ET, gauging labor market resilience amid remittances.

PH Q1 GDP q/q (prev 0.6%) and y/y (exp 3.7%, prev 3%) due May 6 at 22:00 ET, key for growth trajectory. No major Thai, Malaysian, Singaporean, or Vietnamese prints today.

Other Economic Notes

Indonesia-China QRIS cross-border payments launched, easing tourism and trade friction to boost bilateral flows. Thailand stays on US trade watch list over piracy, risking tariffs on exports; BoT eyes capital market reforms via private trusts to attract FDI. Malaysia's ringgit firmed on IMF GDP upgrade, signaling external buffer strength.

Global Macro News

Brent's 5.17% surge to $113.76 reflects war risks and US naval threats against Iran, hammering ASEAN energy importers like Philippines and Thailand. Gold dipped 2.11% to $4,532.40 as USD strength overshadowed haven bids; Bitcoin +2.22% to $80,283 on risk appetite. BoT noted prior rate cuts as buffer amid Fed policy split and escalating conflicts rattling EMs.

(cont...)