ASEAN Macro Daily(Beta Mode)

ID GDP Beats, PH CPI Surges

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 7,057.11 | +1.22% |

| SET | 1,490.10 | -0.24% |

| KLCI | 1,747.43 | +0.44% |

| PSEi | 5,898.08 | -0.74% |

| STI | 4,920.61 | -0.08% |

| USD/IDR | 17,400.00 | +0.31% |

| USD/THB | 32.15 | -1.77% |

| USD/MYR | 3.92 | -0.77% |

| USD/PHP | 60.80 | -1.38% |

| USD/SGD | 1.27 | -0.68% |

| Brent Crude | 101.96 | -7.20% |

| Gold | 4,703.10 | +3.23% |

| Bitcoin | 81,406.00 | +0.59% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 3.48 | - | 2.42 |

| Trade Balance | 1,280m | - | 3,320m |

| Inflation Rate Year-over-Year | 4.10 | 5.50 | 7.20 |

| GDP Growth Year-over-Year | 5.39 | 5.30 | 5.61 |

| Headline Unemployment Rate | 5.10 | - | - |

| Headline Unemployment Rate | 5.10 | - | 5 |

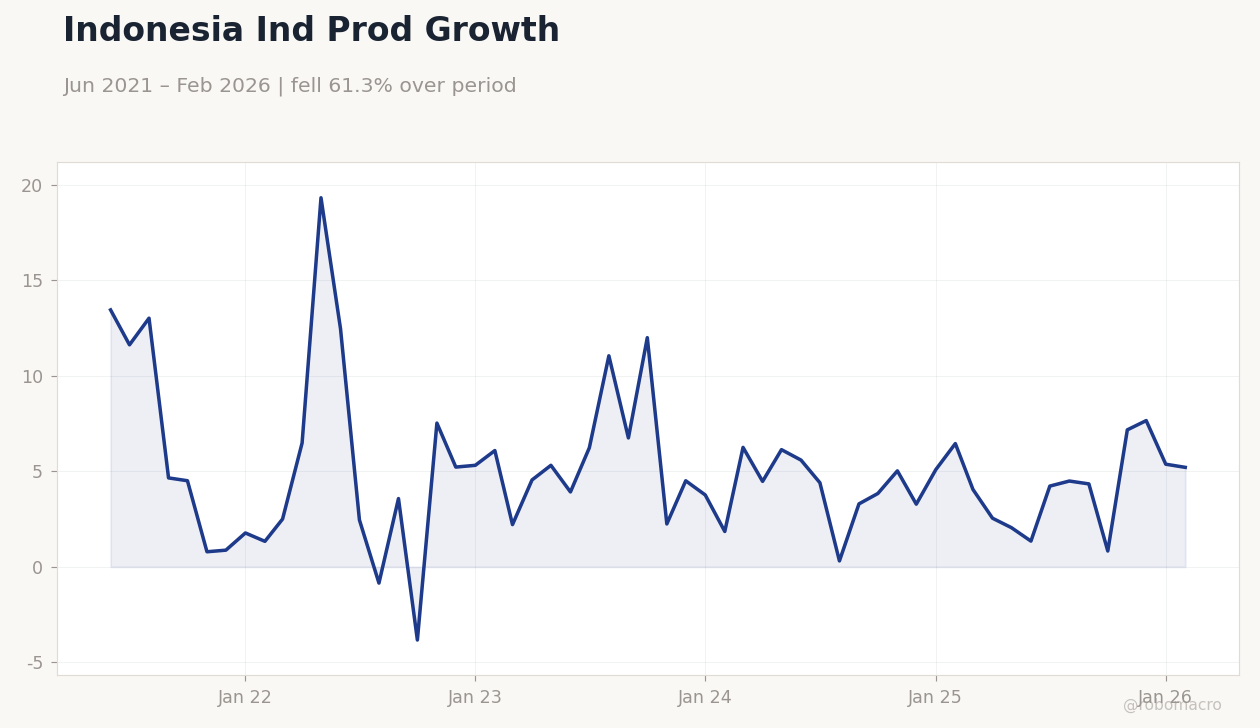

Indonesia Ind Prod Growth | Type: macro_line | Indonesia Ind Prod YoY %: 5.21 (2026-02-01) | Range: -3.835–19.33 | Trend(5pt): 13.46,-0.8528,12,3.282,5.21

Indonesia Ind Prod Growth | Type: macro_line | Indonesia Ind Prod YoY %: 5.21 (2026-02-01) | Range: -3.835–19.33 | Trend(5pt): 13.46,-0.8528,12,3.282,5.21

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter | 0.60 | 1.50 | 18:00 |

| GDP Growth Year-over-Year | 3 | 3.50 | 18:00 |

- Indonesia's Q1 GDP grew 5.61% YoY, topping consensus of 5.3% and prior 5.39%, with inflation easing to 2.42% YoY from 3.48% and trade surplus widening to $3.32B from $1.28B.

- Philippines inflation rose to 7.2% YoY, beating expectations of 5.5% and previous 4.1%, while unemployment fell to 5% from 5.1%, indicating labor market strength.

- Rupiah hit 17,400/USD amid BI stabilization efforts, with ASEAN equities mixed: JCI +1.22%, SET -0.24%, KLCI +0.44%, PSEi -0.74%, STI -0.08%.

Yesterday's Recap

Indonesia led regional news with Q1 GDP expanding 5.61% YoY, exceeding consensus of 5.3% and previous 5.39%, supported by strong commodity exports and domestic demand despite external pressures. Inflation dropped to 2.42% YoY from 3.48%, easing monetary concerns for Bank Indonesia amid rupiah volatility, while the trade balance improved to $3.32B from $1.28B, driven by elevated nickel and palm oil outflows. In the Philippines, inflation accelerated to 7.2% YoY, surpassing the 5.5% forecast and prior 4.1%, due to higher food and energy prices, but unemployment declined to 5% from 5.1%, reflecting resilient services and remittance inflows.

Markets reacted variably: Indonesia's JCI advanced 1.22% to 7,057.11 on commodity boosts, Malaysia's KLCI rose 0.44% to 1,747.43 amid positive palm oil data, but the Philippines' PSEi dropped 0.74% to 5,898.08 on inflation worries. Thailand's SET fell 0.24% to 1,490.10 amid borrowing concerns, and Singapore's STI dipped 0.08% to 4,920.61 with minimal catalysts. Currencies showed divergence against the USD: IDR weakened 0.31% to 17,400, while THB strengthened with USD/THB down 1.77% to 32.15, MYR up via USD/MYR -0.77% to 3.92, PHP stronger at USD/PHP -1.38% to 60.80, and SGD firmer at USD/SGD -0.68% to 1.27.

Brent crude tumbled 7.20% to 101.96, gold climbed 3.23% to 4,703.10, and Bitcoin edged up 0.59% to 81,406.00.

The Day Ahead

Philippines Q1 GDP data is due, with YoY growth forecasted at 3.5% from prior 3% and QoQ at 1.5% from 0.6%, which could shape Bangko Sentral ng Pilipinas policy amid elevated inflation. Attention will be on components like consumer spending and remittances for insights into oil shock resilience. No key releases are scheduled for Indonesia, Thailand, Malaysia, Singapore, or Vietnam, shifting focus to FX trends and potential informal updates on Vietnam FDI.

Malaysia's ringgit may draw interest ahead of Bank Negara Malaysia's meeting, with recent firmness suggesting stable rates to aid manufacturing.

Other Economic Notes

ASEAN growth benefits from supply chain shifts away from US-China tensions, with Vietnam seeing robust FDI in electronics, though Indonesia's commodity dependence leaves it sensitive to Brent crude drops like yesterday's 7.20% decline to 101.96, potentially curbing export earnings. (cont...)