ASEAN Macro Daily(Beta Mode)

ASEAN Stocks Fall, Currencies Weaken

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 6,969.40 | -2.86% |

| SET | 1,500.36 | -0.48% |

| KLCI | 1,748.06 | -0.61% |

| PSEi | 5,960.97 | -1.21% |

| STI | 4,921.90 | -0.41% |

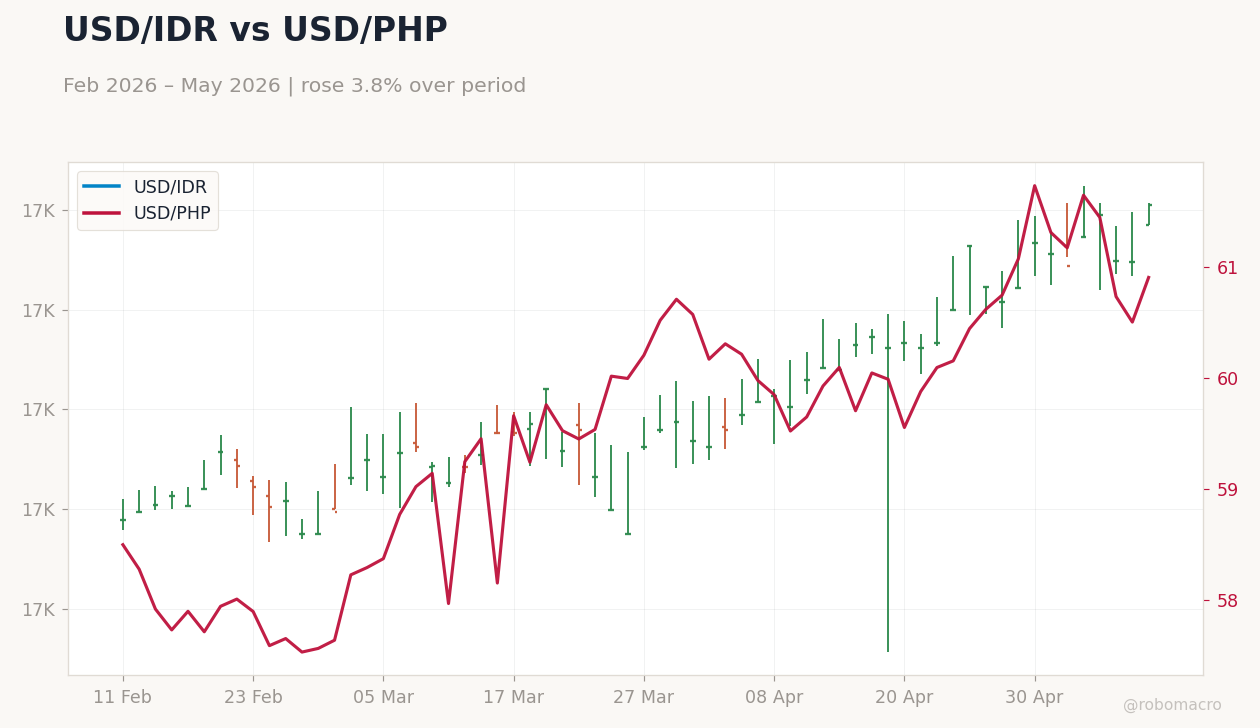

| USD/IDR | 17,410.00 | +0.67% |

| USD/THB | 32.25 | +0.00% |

| USD/MYR | 3.92 | +0.32% |

| USD/PHP | 60.91 | +0.67% |

| USD/SGD | 1.27 | -0.04% |

| Brent Crude | 104.29 | +2.96% |

| Gold | 4,749.60 | +0.62% |

| Bitcoin | 81,831.22 | -0.37% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

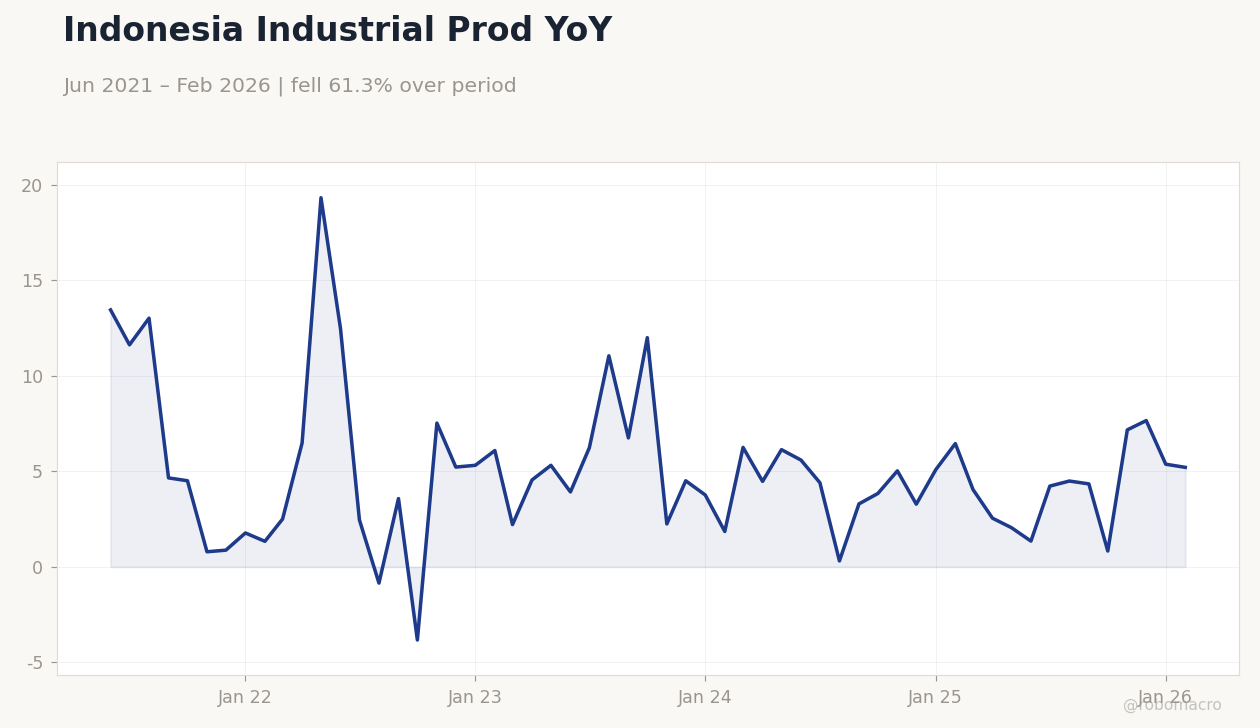

Indonesia Industrial Prod YoY | Type: macro_line | Indonesia IP YoY: 5.21 (2026-02-01) | Range: -3.835–19.33 | Trend(5pt): 13.46,-0.8528,12,3.282,5.21

Indonesia Industrial Prod YoY | Type: macro_line | Indonesia IP YoY: 5.21 (2026-02-01) | Range: -3.835–19.33 | Trend(5pt): 13.46,-0.8528,12,3.282,5.21

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter | 1.90 | - | 22:30 |

| GDP Growth Year-over-Year | 2.50 | - | 22:30 |

- ASEAN equities declined across the board, led by Indonesia's JCI down 2.86% amid rupiah weakness and global caution.

- Currencies mostly softened versus USD, with IDR, MYR, and PHP depreciating, while SGD saw a slight gain.

- Brent crude rose 2.96% to 104.29, offering support to commodity-linked markets, with gold up 0.62% and Bitcoin down 0.37%.

Yesterday's Recap

ASEAN equity markets ended lower on May 10, mirroring global risk aversion driven by mixed economic signals from major economies. Indonesia's JCI fell 2.86% to 6,969.40, hit by rupiah depreciation and outflows from commodity sectors amid softening export demand. Thailand's SET dipped 0.48% to 1,500.36, pressured by ongoing political uncertainties affecting tourism and manufacturing.

Malaysia's KLCI declined 0.61% to 1,748.06, reflecting currency weakness and higher global yields. The Philippines' PSEi dropped 1.21% to 5,960.97, similarly impacted by peso losses and external rate pressures. Singapore's STI eased 0.41% to 4,921.90, with limited inflows despite SGD stability.

On the FX front, USD/IDR climbed 0.67% to 17,410.00, USD/THB held flat at 32.25, USD/MYR rose 0.32% to 3.92, USD/PHP increased 0.67% to 60.91, and USD/SGD dipped 0.04% to 1.27, highlighting uneven capital flow dynamics. Brent crude advanced 2.96% to 104.29, buoyed by supply concerns, while gold gained 0.62% to 4,749.60 and Bitcoin slipped 0.37% to 81,831.22. No regional economic data was released, shifting focus to international developments like US jobs figures.

The Day Ahead

No major economic events are scheduled for May 11 across ASEAN, with markets likely to trade on global sentiment and commodity moves. Upcoming highlights include Thailand's GDP releases on May 17 at 22:30 ET, featuring quarter-over-quarter growth (previous 1.9%) and year-over-year growth (previous 2.5%), which could shape Bank of Thailand policy views. Indonesia may see continued rupiah monitoring by Bank Indonesia amid volatility, potentially prompting interventions.

Singapore's MAS could adjust exchange rate bands if imported inflation pressures build. Malaysia and the Philippines face quiet sessions, though informal updates on industrial output or trade might surface for Vietnam. Traders will eye US Fed signals and oil price trends for directional cues, with any geopolitical escalations from ongoing tensions influencing risk appetite.

Other Economic Notes

ASEAN economies continue navigating supply chain relocations from China, enhancing FDI in Vietnam's electronics and Indonesia's EV sectors despite global slowdown signals. Indonesia and Malaysia's commodity reliance faces volatility from oil and metal prices, with Brent's recent uptick providing temporary relief. <i>↓ p.2</i>