ASEAN Macro Daily(Beta Mode)

Indonesian GDP Beats, Thai Baht Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 6,858.90 | -0.68% |

| SET | 1,483.56 | -0.38% |

| KLCI | 1,750.56 | +0.30% |

| PSEi | 5,971.98 | -0.25% |

| STI | 4,946.00 | +0.07% |

| USD/IDR | 17,491.00 | +0.45% |

| USD/THB | 32.30 | +0.09% |

| USD/MYR | 3.93 | +0.20% |

| USD/PHP | 61.33 | +0.44% |

| USD/SGD | 1.27 | +0.22% |

| Brent Crude | 105.51 | -2.10% |

| Gold | 4,701.90 | +0.52% |

| Bitcoin | 79,259.91 | -1.51% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

SET vs USD/THB | Type: market_hloc | SET: 1484 (2026-05-12) | Range: 1383–1534 | Trend(5pt): 1430,1410,1443,1484,1484 | USD/THB: 32.3 (2026-05-13) | Range: 30.97–32.96 | Trend(5pt): 31.08,31.64,32.85,32.18,32.3

SET vs USD/THB | Type: market_hloc | SET: 1484 (2026-05-12) | Range: 1383–1534 | Trend(5pt): 1430,1410,1443,1484,1484 | USD/THB: 32.3 (2026-05-13) | Range: 30.97–32.96 | Trend(5pt): 31.08,31.64,32.85,32.18,32.3

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter | 1.90 | - | 22:30 |

| GDP Growth Year-over-Year | 2.50 | - | 22:30 |

| Inflation Rate Month-over-Month | 0.30 | - | 00:00 |

| Inflation Rate Year-over-Year | 1.70 | - | 00:00 |

| Central Bank Interest Rate Decision | 4.75 | - | 03:30 |

- Indonesia's Q1 GDP surged to 5.6% y/y, exceeding estimates and signaling resilience despite global headwinds from the Iran War.

- Thai baht under pressure from oil shocks linked to Middle East conflict, with government eyeing $12bn borrowing to cushion impacts.

- Foreign central banks increase holdings of Malaysian bonds, highlighting ringgit's appeal amid regional stability.

Yesterday's Recap

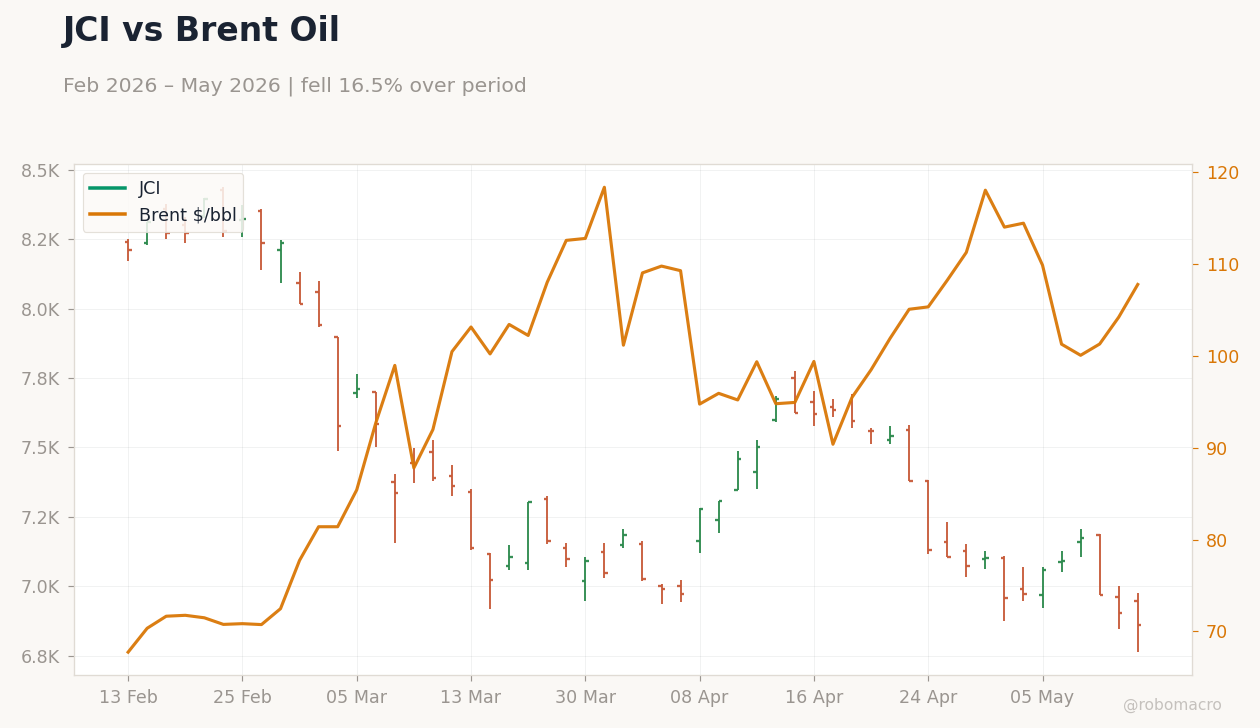

ASEAN equity markets closed mixed amid volatile commodity prices and a firmer USD. Indonesia's JCI fell 0.68% to 6,858.90, pressured by rupiah weakness as USD/IDR rose 0.45% to 17,491.00, despite news highlighting the economy's escape from the '5% growth curse' with Q1 expansion at 5.6%. Thailand's SET dipped 0.38% to 1,483.56, with USD/THB up 0.09% to 32.30, exacerbated by oil price fluctuations and reports of opposition challenges to $12bn debt plans.

Malaysia's KLCI gained 0.30% to 1,750.56, supported by foreign inflows into bonds, while USD/MYR increased 0.20% to 3.93. The Philippines' PSEi declined 0.25% to 5,971.98 as USD/PHP climbed 0.44% to 61.33, and Singapore's STI edged up 0.07% to 4,946.00 with USD/SGD rising 0.22% to 1.27. Brent crude dropped 2.10% to 105.51, weighing on commodity exporters like Indonesia and Malaysia, while gold rose 0.52% to 4,701.90, offering some haven appeal.

Bitcoin fell 1.51% to 79,259.91. No major data releases occurred yesterday, but ongoing news emphasized Indonesia's strong Q1 growth and Thailand's fiscal responses to the Iran War.

The Day Ahead

Key upcoming releases include Thailand's Q1 GDP on May 18, with prior quarter-over-quarter at 1.9% and year-over-year at 2.5%, potentially shaping BoT policy amid baht pressures from oil shocks. Malaysia's April inflation data follows on May 19, after March's 0.3% m/m and 1.7% y/y, testing price stability. Indonesia's BI rate decision is set for May 20, with the benchmark at 4.75% likely to hold steady to support rupiah amid USD/IDR volatility.

These events could spur FX movements across ASEAN, particularly if Thai growth misses or Malaysian inflation rises. Vietnam and Philippines have no immediate data, but spillover from neighbors may influence sentiment. Singapore's MAS will watch NEER bands for imported inflation risks.

Other Economic Notes

Supply chain relocations from China benefit Vietnam and Indonesia, with strong FDI supporting manufacturing and exports like Indonesia's nickel and palm oil. Thailand's tourism sector shows recovery, but Middle East oil disruptions risk higher import costs and fiscal strain, prompting debt ceiling reviews for additional borrowing. The Philippines, reliant on remittances, faces PHP depreciation but draws resilience from domestic consumption.

<i>↓ p.2</i>