ASEAN Macro Daily(Beta Mode)

Rupiah Weakens as Indonesia's Growth Doubted

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 6,162.04 | +1.10% |

| SET | 1,538.67 | +0.39% |

| KLCI | 1,712.67 | +0.25% |

| PSEi | 5,961.40 | +0.69% |

| STI | 5,068.15 | +0.44% |

| USD/IDR | 17,712.00 | +0.11% |

| USD/THB | 32.64 | +0.21% |

| USD/MYR | 3.96 | +0.15% |

| USD/PHP | 61.57 | +1.24% |

| USD/SGD | 1.28 | -0.00% |

| Brent Crude | 100.21 | -2.31% |

| Gold | 4,523.20 | -0.37% |

| Bitcoin | 76,576.49 | -0.13% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

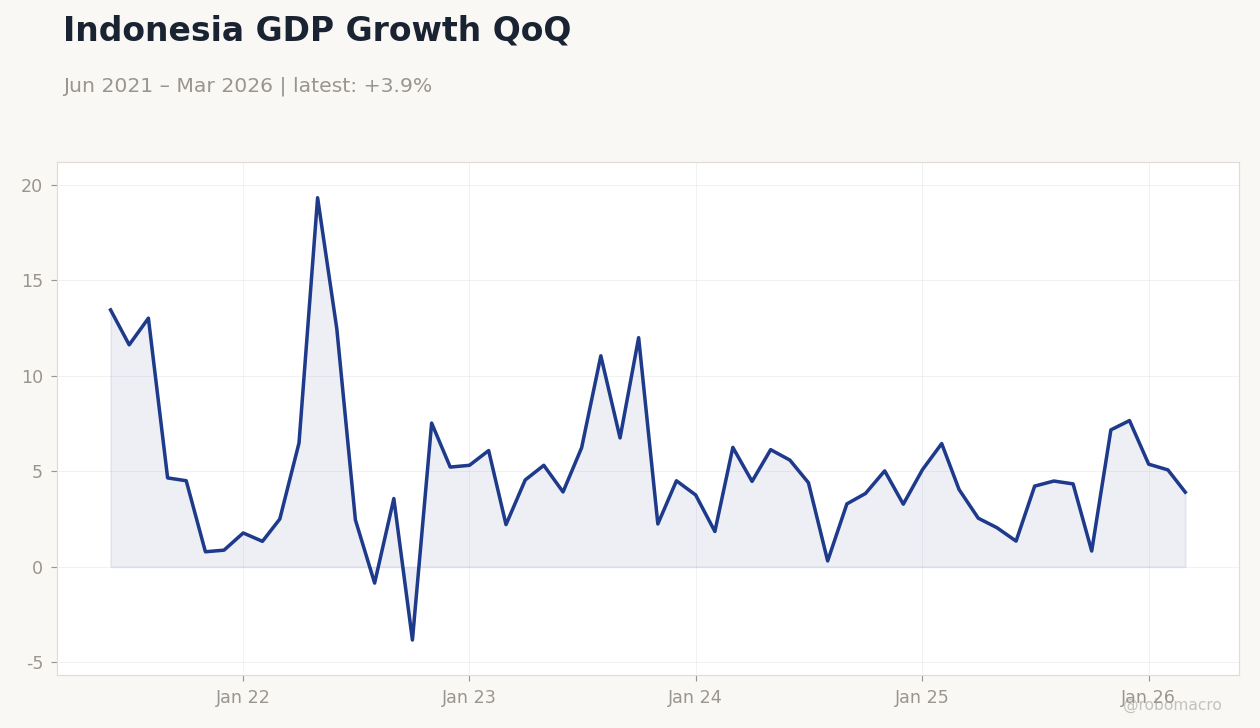

Indonesia GDP Growth QoQ | Type: macro_line | QoQ %: 3.911 (2026-03-01) | Range: -3.835–19.33 | Trend(6pt): 13.46,-0.8528,12,3.282,5.077,3.911

Indonesia GDP Growth QoQ | Type: macro_line | QoQ %: 3.911 (2026-03-01) | Range: -3.835–19.33 | Trend(6pt): 13.46,-0.8528,12,3.282,5.077,3.911

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- JCI rises 1.10% while USD/IDR edges 0.11% higher to 17,712 amid ongoing rupiah pressure.

- Bank Indonesia urges banks to freeze lending rates following its latest hike and reports increased non-dollar trade settlements.

- Regional equities post modest gains but currencies across ASEAN soften against the dollar except SGD.

Yesterday's Recap

Indonesian equities led regional gains as JCI climbed 1.10% to 6,162.04, supported by commodity prices despite fresh questions over the reported 5.61% Q1 GDP figure. Bank Indonesia called on lenders to hold loan rates steady after its recent policy tightening and highlighted a sharp increase in non-dollar bilateral transactions. The rupiah slipped 0.11% to 17,712 per dollar, extending weakness that has already disrupted corporate and education plans.

Thai equities advanced 0.39% to 1,538.67 while the baht weakened 0.21% to 32.64. The ringgit eased 0.15% to 3.96. Philippine and Singapore bourses also finished higher but USD/PHP jumped 1.24% to 61.57.

Brent crude fell 2.31% to 100.21 while gold slipped 0.37%.

The Day Ahead

No major economic releases are scheduled for Indonesia, Thailand, Malaysia, Philippines, Singapore or Vietnam. Markets will monitor ongoing rupiah volatility and any further Bank Indonesia comments on lending rates. Thailand’s bond market remains in focus after recent defaults by listed firms.

Malaysia’s ringgit is expected to trade in a narrow 3.95-3.97 range against the dollar. Regional investors will also track external drivers including US Treasury yields and oil prices. Equity turnover is likely to stay light ahead of the holiday-adjusted week.

Other Economic Notes

Indonesia’s large commodity base has not shielded the rupiah from sustained depreciation pressures that now echo earlier crisis episodes. Growth scepticism centres on whether Q1 data fully capture subdued capital-goods imports. Thailand’s bond defaults add to domestic credit concerns without immediate central-bank intervention.

Broader ASEAN economies continue to navigate supply-chain shifts that favour Vietnam yet leave Indonesia and the Philippines more exposed to capital-flow reversals.

Global Macro News

US Treasury yields above 5% and elevated oil prices have created a perfect storm for emerging-market currencies including the rupiah and peso. Comparisons to 1997-98 pressures have resurfaced in market commentary though Indonesian officials insist fundamentals rule out a repeat. European Central Bank signals on inflation risks tied to geopolitical tensions add another layer of external volatility.

<i>↓ p.2</i>