ASEAN Macro Daily(Beta Mode)

BI Urges Rate Freeze as IDR Steadies

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 6,162.04 | +1.10% |

| SET | 1,538.67 | +0.39% |

| KLCI | 1,712.67 | +0.25% |

| PSEi | 5,961.40 | +0.69% |

| STI | 5,068.15 | +0.44% |

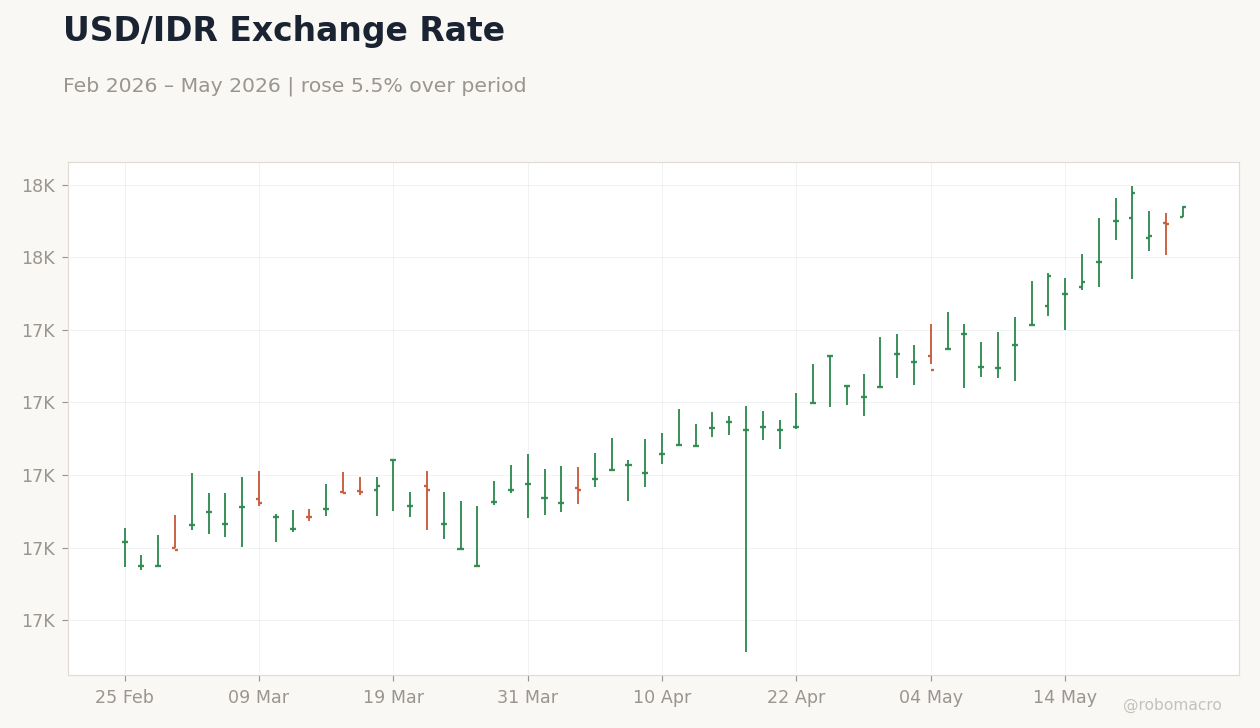

| USD/IDR | 17,738.00 | +0.26% |

| USD/THB | 32.45 | -0.37% |

| USD/MYR | 3.95 | -0.20% |

| USD/PHP | 61.28 | +0.35% |

| USD/SGD | 1.28 | -0.07% |

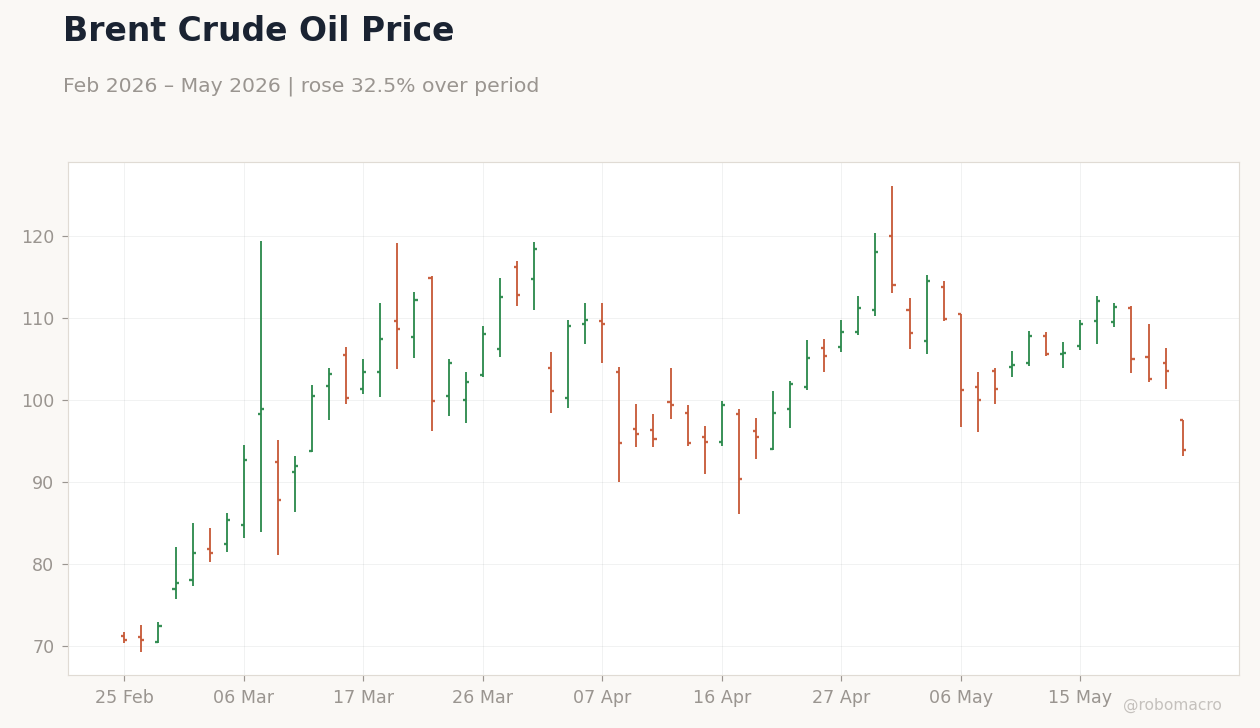

| Brent Crude | 100.21 | -3.22% |

| Gold | 4,574.10 | +1.17% |

| Bitcoin | 77,278.53 | +0.39% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

USD/IDR Exchange Rate | Type: market_hloc | IDR per USD: 1.774e+04 (2026-05-25) | Range: 1.675e+04–1.778e+04 | Trend(5pt): 1.682e+04,1.704e+04,1.706e+04,1.729e+04,1.774e+04

USD/IDR Exchange Rate | Type: market_hloc | IDR per USD: 1.774e+04 (2026-05-25) | Range: 1.675e+04–1.778e+04 | Trend(5pt): 1.682e+04,1.704e+04,1.706e+04,1.729e+04,1.774e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Indonesia’s JCI rose 1.10% to 6,162.04 while USD/IDR edged up 0.26% to 17,738 amid BI guidance to freeze lending rates.

- Regional equities posted modest gains, with SET +0.39%, KLCI +0.25%, PSEi +0.69% and STI +0.44% on thin volume.

- Brent crude fell 3.22% to $100.21 while gold climbed 1.17% to $4,574.10, reflecting softer energy prices and safe-haven demand.

Yesterday's Recap

Indonesia dominated ASEAN market moves as Bank Indonesia urged lenders to hold lending rates steady following its latest policy adjustment. The rupiah traded near 17,738 per dollar, supported by rising non-dollar bilateral settlements and official comments that current weakness differs from 1997-98 crisis dynamics. Jakarta equities advanced 1.10% while Indonesian bonds shrugged off the recent hike, with yields little changed.

Thailand’s SET index gained 0.39% despite April car production falling 0.44% year-on-year to a five-year low. Malaysia’s KLCI edged 0.25% higher as reserves reached $129.5 billion. Singapore’s STI rose 0.44% with USD/SGD easing 0.07% to 1.28.

Philippine shares climbed 0.69% while the peso weakened 0.35% to 61.28.

The Day Ahead

No major data releases are scheduled across the six ASEAN economies. Markets will monitor follow-through on Bank Indonesia’s call for stable lending rates and any further comments on non-dollar trade settlement growth. Traders will also watch ringgit trading ranges cited between 3.95-3.97 and Thai bond-market developments after recent corporate defaults.

Regional sentiment may stay influenced by external oil-price moves and US Treasury yield levels. Equity volumes are expected to remain light ahead of the US Memorial Day holiday.

Other Economic Notes

Indonesia’s commodity exports continue to underpin trade surpluses even as the rupiah faces structural pressure from higher US yields. Malaysia’s reserve build to $129.5 billion provides a buffer against capital-flow volatility. Thailand’s manufacturing and tourism sectors show mixed signals, with car output at multi-year lows offset by recovering Chinese visitor arrivals.

Broader ASEAN growth remains supported by supply-chain shifts from China, though remittance-dependent Philippines and manufacturing-focused Vietnam face differing external risks.

Global Macro News

US Treasury yields above 5% and elevated oil prices have renewed pressure on emerging-market currencies, echoing 1997-style concerns though officials stress structural differences. <i>↓ p.2</i>