ASEAN Macro Daily(Beta Mode)

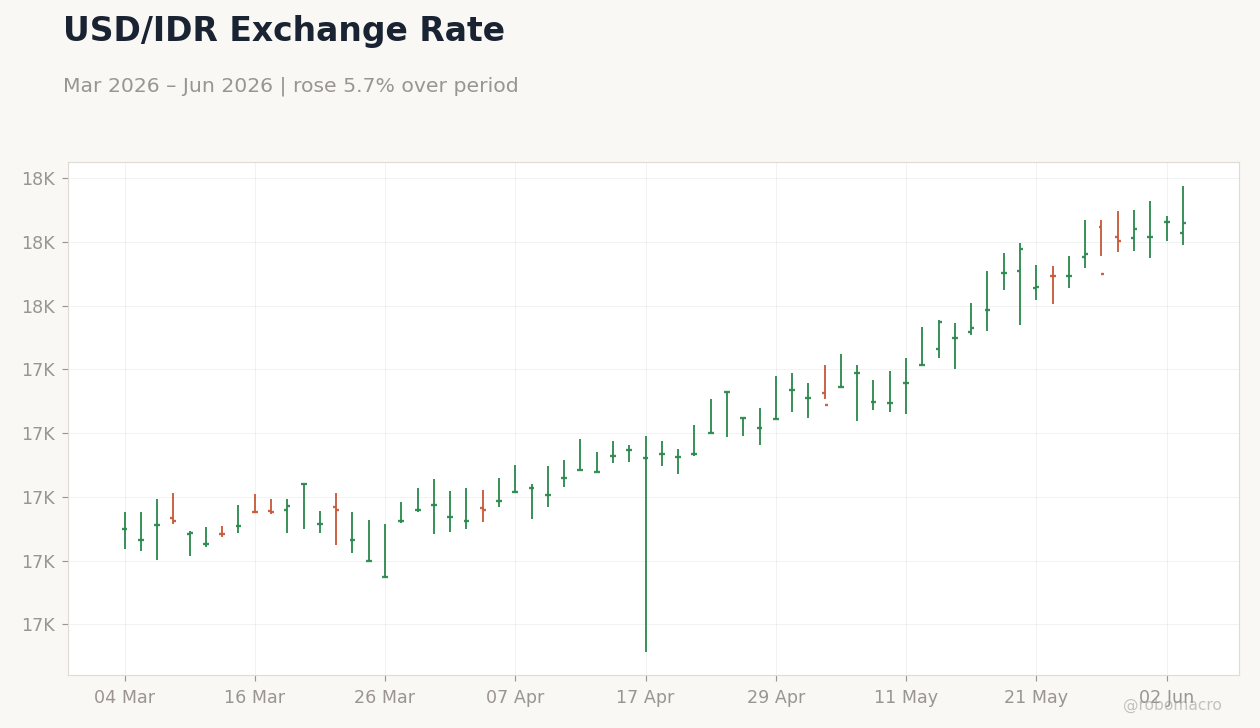

BI Defends Rupiah at Record Low on Inflation Beat

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 6,195.43 | +1.11% |

| SET | 1,588.06 | +1.26% |

| KLCI | 1,683.07 | +0.00% |

| PSEi | 5,912.69 | +1.95% |

| STI | 5,097.42 | +1.18% |

| USD/IDR | 17,858.00 | -0.03% |

| USD/THB | 32.69 | +0.00% |

| USD/MYR | 3.97 | +0.13% |

| USD/PHP | 61.68 | -0.12% |

| USD/SGD | 1.28 | +0.26% |

| Brent Crude | 97.19 | +1.24% |

| Gold | 4,477.50 | -0.26% |

| Bitcoin | 64,215.38 | -3.73% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2.42 | 2.97 | 3.08 |

| Trade Balance | 3,320m | 1,500m | 90m |

Indonesia Trade Balance | Type: macro_line | USD mn: -6.031e+04 (2026-03-01) | Range: -1.359e+05–-3.11e+04 | Trend(5pt): -6.917e+04,-6.778e+04,-6.505e+04,-1.283e+05,-6.031e+04

Indonesia Trade Balance | Type: macro_line | USD mn: -6.031e+04 (2026-03-01) | Range: -1.359e+05–-3.11e+04 | Trend(5pt): -6.917e+04,-6.778e+04,-6.505e+04,-1.283e+05,-6.031e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 7.20 | 7.50 | 17:00 |

| Thursday (2026-06-04) | |||

| Inflation Rate Year-over-Year | 7.20 | 7.50 | 17:00 |

- Indonesia inflation rose to 3.08% y/y while trade surplus collapsed to $90 million, missing forecasts sharply.

- Rupiah hit fresh record lows near 17,900 per USD, prompting stepped-up Bank Indonesia intervention and capital-flow measures.

- Regional equities advanced with PSEi gaining 1.95% and JCI rising 1.11%, while USD/IDR held near session highs.

Yesterday's Recap

Indonesia’s May inflation print surprised to the upside at 3.08% y/y against a 2.97% consensus, while the trade balance plunged to just $90 million versus expectations of $1.5 billion. The rupiah weakened to record lows around 17,858-17,900 per USD, triggering Bank Indonesia statements that it would continue supporting the currency through direct intervention and synergy with fiscal authorities. Equity markets showed resilience despite the currency pressure, with the JCI closing 1.11% higher at 6,195.43 and the PSEi surging 1.95% to 5,912.69.

Thailand’s SET index rose 1.26% while the Bank of Thailand flagged 2% GDP growth and 3% inflation for 2026. Malaysia’s KLCI was flat and the Singapore dollar weakened 0.26% against the USD. Brent crude climbed 1.24% to $97.19, providing modest support to commodity-linked ASEAN assets.

The Day Ahead

Philippines May inflation data due tomorrow will be the key release, with consensus pointing to a 7.5% y/y print. Markets will watch for any acceleration that could prompt the BSP to accelerate tightening. No major data are scheduled for Indonesia, Thailand or Malaysia.

Traders will also monitor Bank Indonesia’s daily FX operations and any further comments on rupiah stability. Regional bond auctions in Singapore and Thailand may provide additional color on local yield curves.

Other Economic Notes

Supply-chain diversification continues to favor Vietnam and Malaysia, with semiconductor and electronics FDI inflows remaining robust. Indonesia’s weaker-than-expected trade balance highlights downside risks to the current-account surplus that has helped buffer rupiah pressure. Regional equity valuations remain supported by commodity prices and selective foreign inflows, though persistent USD strength poses a headwind for external-debt issuers.

Thailand’s planned BOT fee overhaul is expected to trim bank revenues by roughly 5 billion baht annually.

Global Macro News

Gold slipped 0.26% while Bitcoin fell 3.73%, reflecting risk-off sentiment that has amplified pressure on the rupiah. IMF and Bundesbank cautioned against political interference in central-bank independence, a theme relevant for several ASEAN policymakers.