ASEAN Macro Daily(Beta Mode)

BI, BSP Face Rate-Hike Pressure as Rupiah Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 6,254.97 | +4.12% |

| SET | 1,592.41 | +1.28% |

| KLCI | 1,709.99 | +1.10% |

| PSEi | 5,910.06 | -0.53% |

| STI | 5,116.86 | +0.78% |

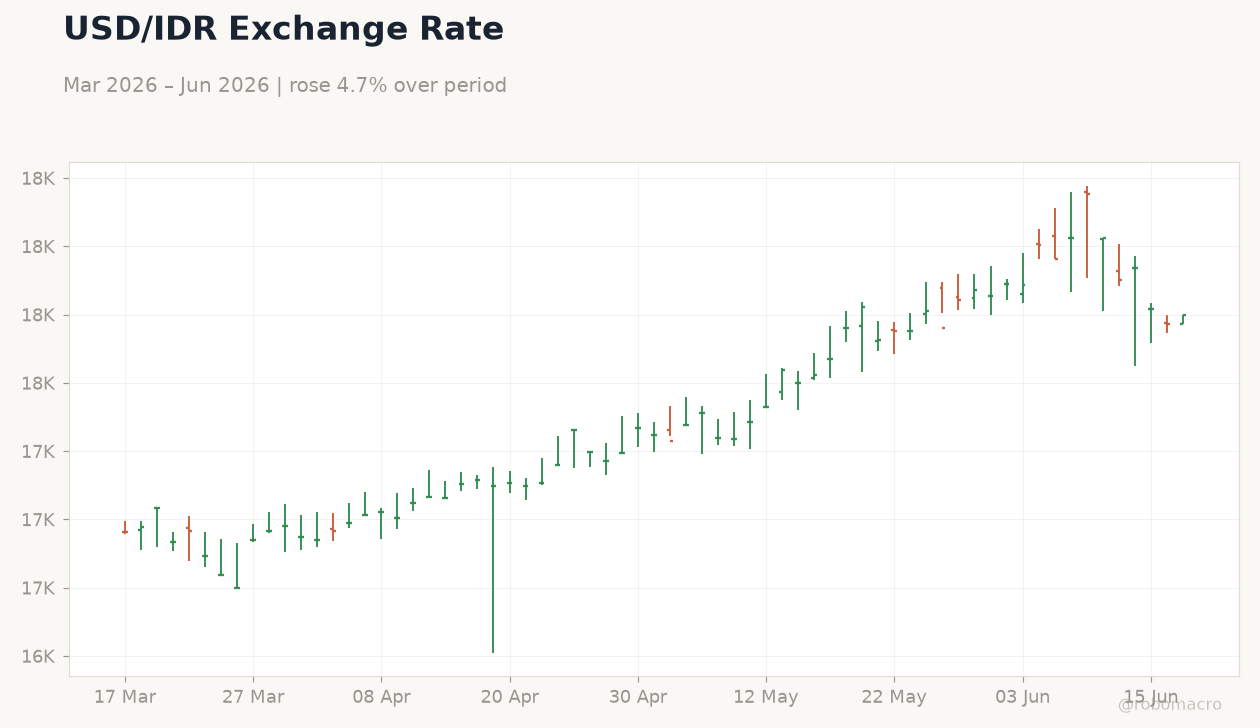

| USD/IDR | 17,748.00 | +0.18% |

| USD/THB | 32.74 | +0.65% |

| USD/MYR | 4.07 | +0.43% |

| USD/PHP | 60.41 | +0.24% |

| USD/SGD | 1.29 | +0.46% |

| Brent Crude | 79.32 | +0.46% |

| Gold | 4,285.80 | -1.04% |

| Bitcoin | 64,281.06 | -2.01% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

JCI Indonesia Equity Index | Type: market_hloc | Index Level: 6255 (2026-06-15) | Range: 5342–7676 | Trend(5pt): 7107,7500,6957,6162,6255

JCI Indonesia Equity Index | Type: market_hloc | Index Level: 6255 (2026-06-15) | Range: 5342–7676 | Trend(5pt): 7107,7500,6957,6162,6255

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Central Bank Interest Rate Decision | 4.50 | 4.75 | 22:30 |

| Central Bank Interest Rate Decision | 5.50 | 5.75 | 23:30 |

| Inflation Rate Month-over-Month | 0.40 | - | 20:00 |

| Inflation Rate Year-over-Year | 1.90 | 2.10 | 20:00 |

- BI and BSP face pressure to raise rates at tonight’s decisions as USD/IDR hits 17,748 and inflation risks rise.

- Regional equities advance with JCI surging 4.12% while PSEi slips 0.53% ahead of policy outcomes.

- Malaysia inflation data tomorrow and BoJ’s 1.0% rate lift shape external capital flow dynamics for ASEAN.

Yesterday's Recap

ASEAN markets showed resilience on 16 June despite thin data releases. Indonesia’s JCI climbed 4.12% to 6,254.97 on commodity support while Thailand’s SET gained 1.28% to 1,592.41 and Malaysia’s KLCI rose 1.10% to 1,709.99. The Philippines PSEi fell 0.53% to 5,910.06 as investors positioned ahead of BSP action.

Currencies weakened modestly against the dollar with USD/IDR at 17,748 (+0.18%), USD/THB at 32.74 (+0.65%) and USD/MYR at 4.07 (+0.43%). Singapore’s STI edged up 0.78% to 5,116.86. Brent crude settled at 79.32 (+0.46%) while gold fell 1.04% to 4,285.80.

News flow centered on rupiah stability concerns ahead of BI’s meeting.

The Day Ahead

Philippines and Indonesia central banks announce policy at 22:30 and 23:30 ET respectively with markets pricing 25 bp hikes. Malaysia releases May inflation MoM and YoY prints at 20:00 ET tomorrow. Traders will monitor any signals on further tightening from BI given persistent USD/IDR pressure.

Thailand’s fuel price cut of 1-1.20 baht per litre offers minor relief to consumers but does not alter BoT’s hold bias. Singapore and Vietnam calendars remain quiet with focus on external Fed signals.

Other Economic Notes

Indonesia’s rupiah recovery hinges on credible BI tightening according to OCBC analysts amid ongoing capital outflow risks. Thailand advances OECD tax information sharing and semiconductor strategy to attract FDI in high-value manufacturing. Malaysia’s economy shifts toward stability-driven growth rather than mega-projects while semiconductor labor demand draws large queues.

Broader ASEAN supply-chain realignment continues as firms diversify from China.

Global Macro News

Bank of Japan raised its policy rate to a 31-year high of 1.0% citing inflation risks and supporting JPY strength that eases pressure on ASEAN currencies. UAE central bank held rates at 3.65% following the Fed’s latest move. Bank of America reiterated its firm stance on persistent inflation.

World Bank-backed FDI initiatives in Egypt highlight competition for capital flows affecting ASEAN. Thailand fuel prices fell 1-1.20 baht per litre at major stations.