ASEAN Macro Daily(Beta Mode)

Bank Indonesia Hikes Rates to Defend Rupiah

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 6,177.14 | +0.08% |

| SET | 1,572.50 | -0.79% |

| KLCI | 1,712.03 | +0.04% |

| PSEi | 6,135.35 | -0.30% |

| STI | 5,192.70 | -0.39% |

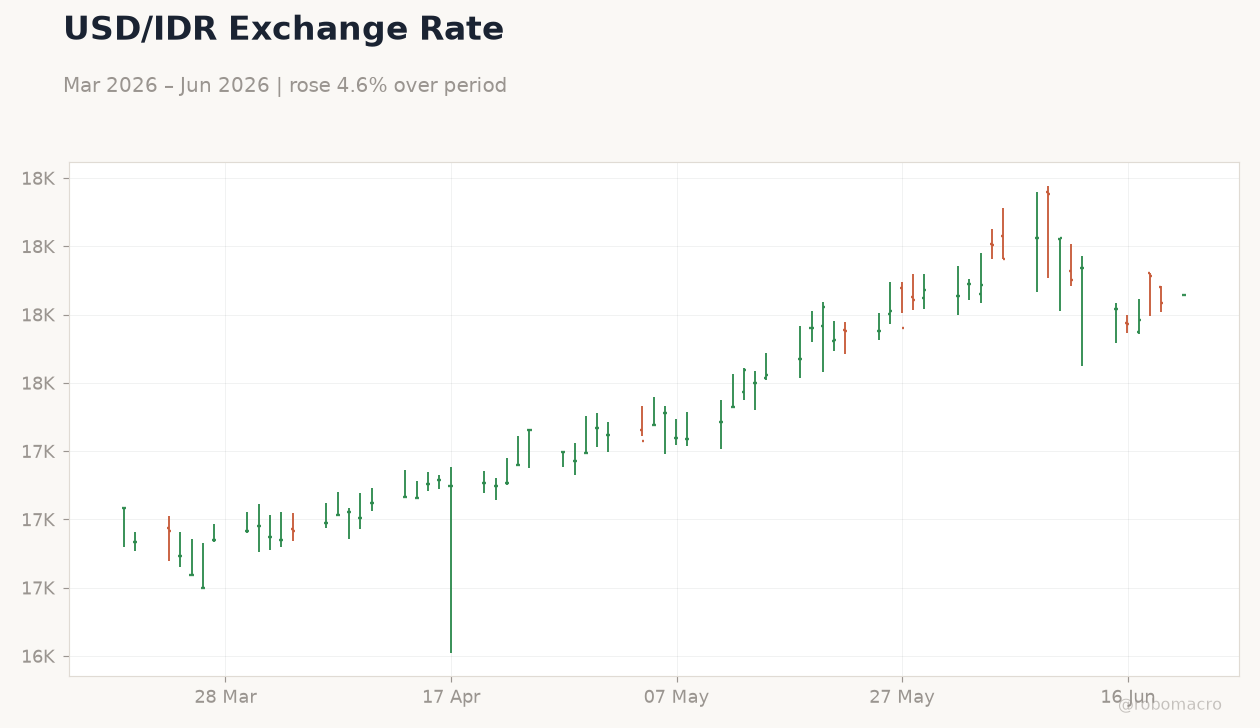

| USD/IDR | 17,821.00 | +0.15% |

| USD/THB | 32.82 | +0.15% |

| USD/MYR | 4.13 | +0.46% |

| USD/PHP | 60.62 | +0.93% |

| USD/SGD | 1.29 | +0.07% |

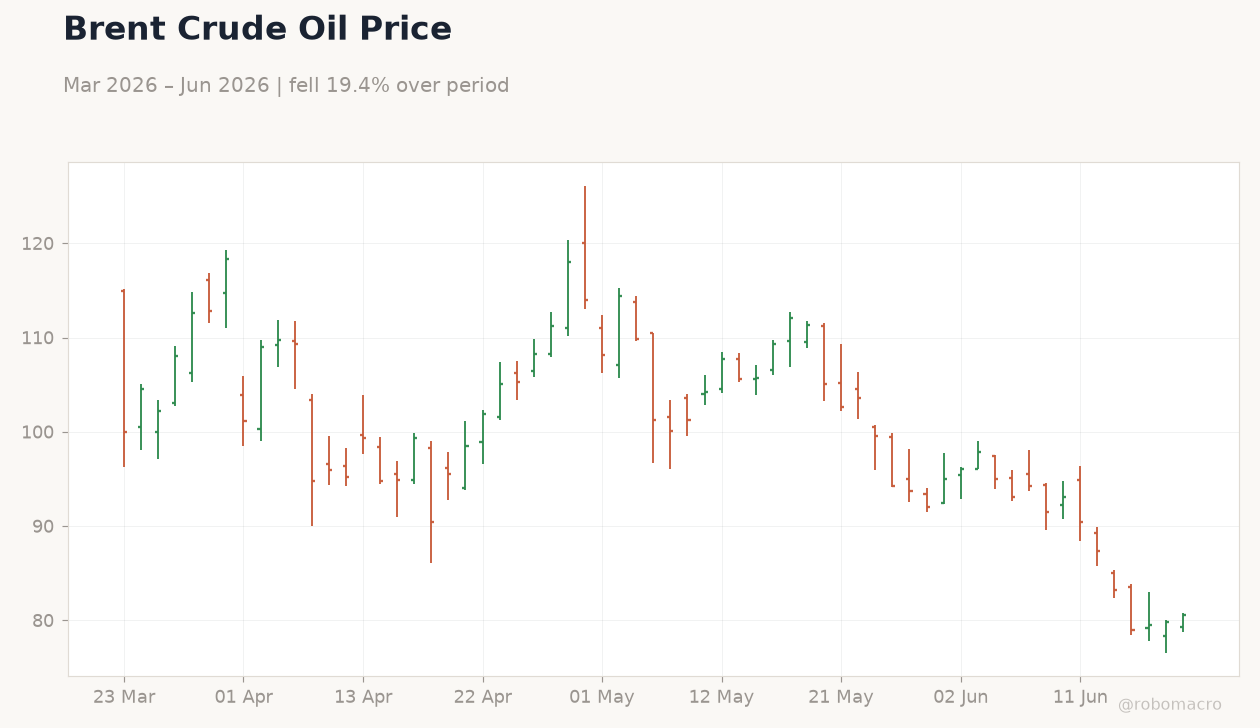

| Brent Crude | 80.59 | +0.93% |

| Gold | 4,172.90 | -1.21% |

| Bitcoin | 63,623.99 | -0.96% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

USD/IDR Exchange Rate | Type: market_hloc | IDR per USD: 1.782e+04 (2026-06-21) | Range: 1.675e+04–1.819e+04 | Trend(5pt): 1.704e+04,1.708e+04,1.739e+04,1.784e+04,1.782e+04

USD/IDR Exchange Rate | Type: market_hloc | IDR per USD: 1.782e+04 (2026-06-21) | Range: 1.675e+04–1.819e+04 | Trend(5pt): 1.704e+04,1.708e+04,1.739e+04,1.784e+04,1.782e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Central Bank Interest Rate Decision | 1 | 1 | 03:00 |

- Bank Indonesia raised policy rates to counter rupiah weakness, with USD/IDR climbing 0.15% to 17,821.

- Thailand’s central bank is scheduled to announce its rate decision on 24 June, with consensus holding the benchmark at 1.0%.

- Regional equities closed mixed as USD strength pressured ASEAN currencies, while Brent crude rose 0.93% to $80.59.

Yesterday's Recap

Indonesia dominated regional news flow as Bank Indonesia delivered another rate increase aimed at stabilising the rupiah after it slipped back below the 18,000 per dollar mark. The central bank also lowered the documentation threshold for dollar purchases and mandated rupiah use for tourism transactions in Bali. Equity markets reflected selective resilience, with Indonesia’s JCI edging 0.08% higher to 6,177.14 while Thailand’s SET fell 0.79% to 1,572.50.

Malaysia’s KLCI gained 0.04% to 1,712.03 and the Philippines PSEi declined 0.30% to 6,135.35. Currencies broadly weakened against the dollar, with USD/PHP rising 0.93% to 60.62 and USD/MYR up 0.46% to 4.13. Gold fell 1.21% to 4,172.90 amid stronger USD flows.

The Day Ahead

Thailand’s Monetary Policy Committee meets on 24 June with markets expecting the policy rate to remain at 1.0%. Indonesia will auction 10-year and 20-year government bonds, testing investor appetite after the latest BI tightening. No major data releases are scheduled for Malaysia, the Philippines or Singapore.

Vietnam’s SBV continues to monitor FDI inflows tied to electronics supply chains. MAS will watch USD/SGD movements within its NEER band for any signs of imported inflation pressure.

Other Economic Notes

Indonesia’s external position benefits from sustained nickel and palm-oil exports, reducing immediate balance-of-payments strain despite global volatility. Vietnam maintains manufacturing momentum through Apple and Samsung supplier shifts, supporting steady FDI. Thailand and Malaysia face softer semiconductor and tourism readings that limit upside to growth forecasts.

Remittance inflows remain a key support for the Philippines peso amid elevated USD/PHP levels.

Global Macro News

US dollar strength continued to transmit pressure across emerging-market currencies, amplifying capital-flow sensitivity in ASEAN. Brent crude advanced on Middle-East supply concerns, providing modest terms-of-trade relief for Indonesia and Malaysia. Gold’s decline reflected reduced safe-haven demand as risk sentiment stabilised.

<i>↓ p.2</i>