ASEAN Macro Daily(Beta Mode)

BoT Holds at 1%, Rupiah Rebounds on Inflows

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 5,883.88 | -3.56% |

| SET | 1,572.50 | -0.79% |

| KLCI | 1,682.13 | +0.13% |

| PSEi | 6,135.35 | -0.30% |

| STI | 5,215.99 | +0.20% |

| USD/IDR | 17,990.00 | +0.41% |

| USD/THB | 33.34 | -0.10% |

| USD/MYR | 4.14 | -0.06% |

| USD/PHP | 61.24 | -0.23% |

| USD/SGD | 1.30 | -0.08% |

| Brent Crude | 74.98 | +1.68% |

| Gold | 4,040.30 | +1.25% |

| Bitcoin | 59,743.44 | -2.05% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Central Bank Interest Rate Decision | 1 | 1 | 1 |

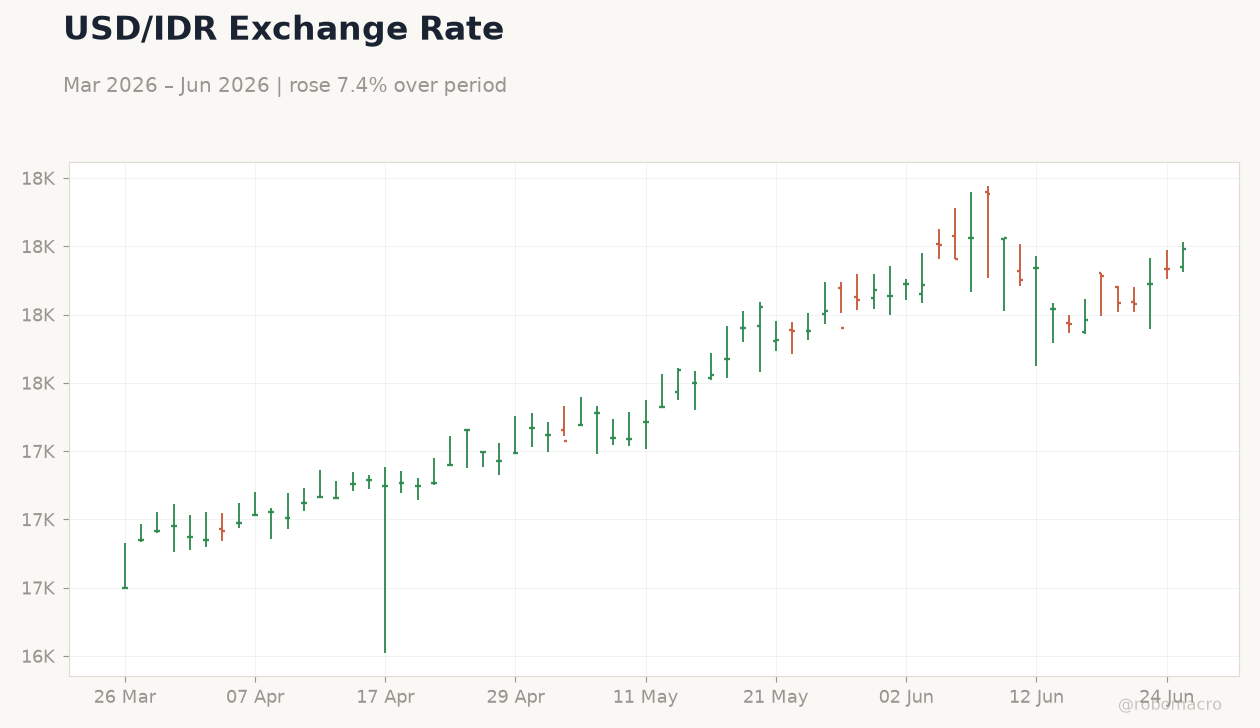

USD/IDR Exchange Rate | Type: market_hloc | Rate: 1.799e+04 (2026-06-25) | Range: 1.675e+04–1.819e+04 | Trend(6pt): 1.675e+04,1.712e+04,1.736e+04,1.786e+04,1.792e+04,1.799e+04

USD/IDR Exchange Rate | Type: market_hloc | Rate: 1.799e+04 (2026-06-25) | Range: 1.675e+04–1.819e+04 | Trend(6pt): 1.675e+04,1.712e+04,1.736e+04,1.786e+04,1.792e+04,1.799e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Bank of Thailand kept its benchmark rate at 1.00% and lifted its 2026 GDP forecast to 2.3%.

- Rupiah recovered after nearing 18,000 per USD as foreign inflows resumed into Indonesian assets.

- Regional equities closed mixed while USD/IDR rose 0.41% to 17,990 amid hawkish Fed signals.

Yesterday's Recap

Thailand’s central bank left its policy rate unchanged at 1.00% as expected, citing the need to monitor fragile domestic demand and inflation. The decision coincided with an upward revision to the 2026 growth outlook to 2.3%. In Indonesia, the rupiah rebounded from session lows near 18,000 after foreign portfolio inflows resumed, supported by optimism around MSCI rebalancing.

Bank Indonesia is viewed by MUFG and Barclays as likely to maintain its 5.50% rate to buffer the currency against further USD strength. Malaysia’s ringgit extended gains on stronger-than-expected economic data, prompting Bank Negara Malaysia to step up measures encouraging foreign-income conversion. Equity markets reflected the divergence: Indonesia’s JCI fell 3.56% while Singapore’s STI rose 0.20% and Malaysia’s KLCI edged up 0.13%.

Thailand’s SET declined 0.79% as investors digested the policy hold and persistent trade deficit concerns.

The Day Ahead

The ASEAN calendar is empty today and tomorrow, leaving markets to focus on external drivers and domestic FX flows. Indonesia’s rupiah trajectory will remain in focus given ongoing de-dollarisation talks with China and potential BI intervention. Malaysia’s ringgit may see continued support if BNM maintains its foreign-income conversion push.

Thailand’s trade data and tourism indicators will be watched for signs the recovery is broadening. Singapore’s MAS will continue to manage the SGD NEER band amid regional volatility, while Philippine peso weakness remains a market theme.

Other Economic Notes

Indonesia is accelerating efforts to secure yuan financing and reduce USD dependence, aligning with broader supply-chain diversification away from single-currency exposure. Regional manufacturing hubs continue to benefit from US-China trade shifts, though Thailand’s persistent trade deficit highlights uneven export momentum. Commodity prices remain supportive for Indonesia and Malaysia, with Brent crude up 1.68% and gold rising 1.25%, providing a buffer to external balances.

Global Macro News

A hawkish Fed tone lifted the dollar and weighed on EM currencies, pushing USD/IDR to 17,990. Brent crude gained 1.68% to $74.98 on supply concerns, while gold advanced 1.25% to $4,040.30 as a hedge. <i>↓ p.2</i>