ASEAN Macro Daily(Beta Mode)

Thailand Holds Rate at 1%, Indonesia Adds Liquidity

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 5,896.13 | -1.72% |

| SET | 1,542.34 | -1.04% |

| KLCI | 1,667.74 | +0.24% |

| PSEi | 6,072.24 | +0.02% |

| STI | 5,191.73 | -0.52% |

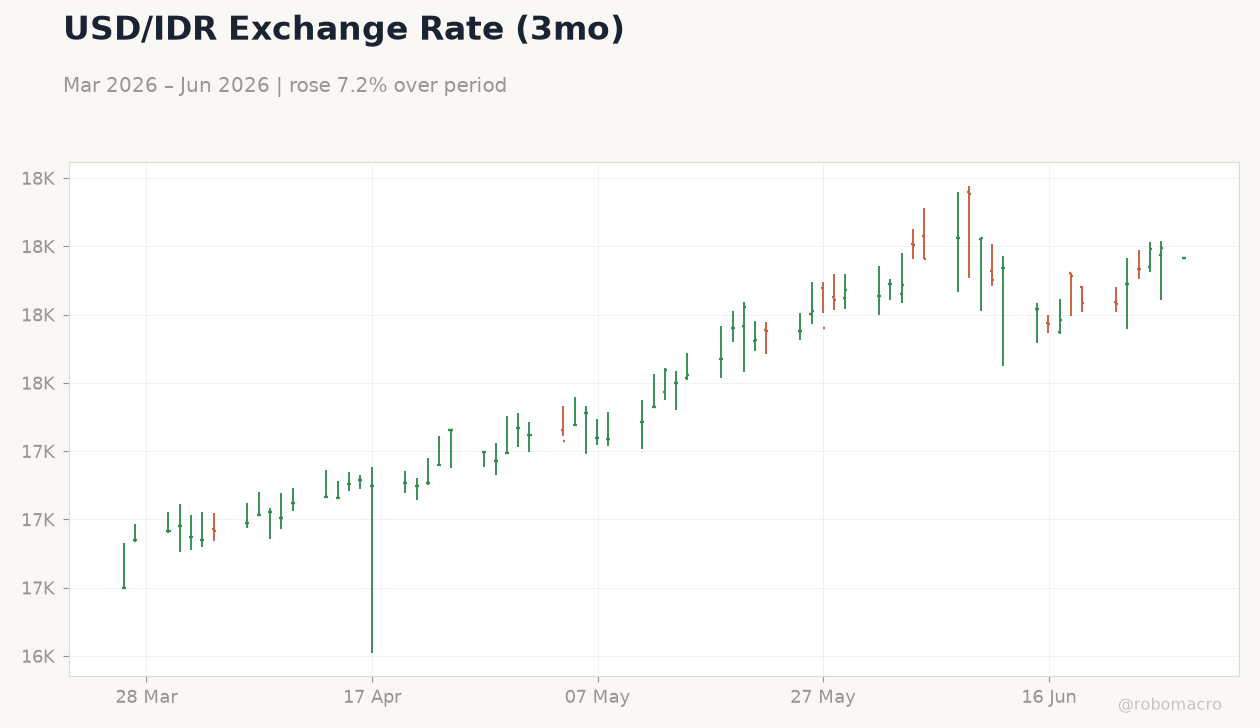

| USD/IDR | 17,957.00 | -0.21% |

| USD/THB | 33.30 | +0.02% |

| USD/MYR | 4.09 | -0.76% |

| USD/PHP | 61.31 | -0.02% |

| USD/SGD | 1.29 | -0.29% |

| Brent Crude | 72.60 | -3.53% |

| Gold | 4,096.30 | +1.63% |

| Bitcoin | 59,703.66 | -0.39% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Central Bank Interest Rate Decision | 1 | 1 | 1 |

Brent Crude Oil (3mo) | Type: market_hloc | USD per Barrel: 72.6 (2026-06-26) | Range: 72.6–118.3 | Trend(6pt): 112.8,98.48,107.8,97.81,75.26,72.6

Brent Crude Oil (3mo) | Type: market_hloc | USD per Barrel: 72.6 (2026-06-26) | Range: 72.6–118.3 | Trend(6pt): 112.8,98.48,107.8,97.81,75.26,72.6

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Bank of Thailand kept its policy rate at 1.00% amid cautious growth outlook and Fed divergence pressures.

- Indonesia announced Rp400 trillion liquidity injection into state banks to support lending and economic activity.

- Regional equities closed mixed with JCI falling 1.72% and SET declining 1.04% while KLCI rose 0.24%.

Yesterday's Recap

Thailand’s central bank held its benchmark rate at 1.00%, matching consensus and the prior level, as the committee cited external uncertainties and a measured domestic recovery. Indonesia’s finance ministry confirmed the Rp400 trillion deposit boost to state banks, aimed at expanding credit channels. Bank Indonesia stepped up foreign-exchange carrying supervision to anchor rupiah stability following recent capital inflows.

The rupiah firmed 0.21% to 17,957 per dollar while the Thai baht edged 0.02% weaker to 33.30. Equity markets reflected profit-taking: Indonesia’s JCI dropped 1.72% to 5,896.13 and Thailand’s SET fell 1.04% to 1,542.34, whereas Malaysia’s KLCI gained 0.24% to 1,667.74. Brent crude slid 3.53% to $72.60 per barrel, easing imported inflation risks across the region.

Singapore’s STI declined 0.52% while the Philippines’ PSEi remained essentially flat.

The Day Ahead

No major data releases or policy meetings are scheduled across the six ASEAN economies today or tomorrow. Markets will monitor follow-through on Indonesia’s liquidity measures and any further Bank Indonesia foreign-exchange guidance. Thailand’s stablecoin regulatory framework is expected to enter its final consultation phase this week.

Regional investors will also track external drivers including US data prints and oil-price movements that influence ASEAN currencies and yields. Attention remains on capital-flow trends given the recent return of foreign inflows to Indonesian assets.

Other Economic Notes

The World Bank lowered its medium-term growth projection for Indonesia to 5.0% by 2026, citing slower investment momentum after the commodity boom. HSBC highlighted rising rupiah-driven risks should growth cool while inflation edges higher next year. Malaysia’s ringgit received policy support from Bank Negara’s renewed repatriation measures, limiting downside despite a firmer dollar.

Thailand’s tourism recovery and electronics exports continue to underpin external balances, though political noise has resurfaced. Broader ASEAN FDI flows remain tilted toward Vietnam’s electronics supply-chain relocation and Indonesia’s battery-related projects.