ASEAN Macro Daily(Beta Mode)

BI Tightens FX Oversight as Rupiah Stabilizes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 5,896.13 | -1.72% |

| SET | 1,542.34 | -1.04% |

| KLCI | 1,667.74 | +0.24% |

| PSEi | 6,072.24 | +0.02% |

| STI | 5,191.73 | -0.52% |

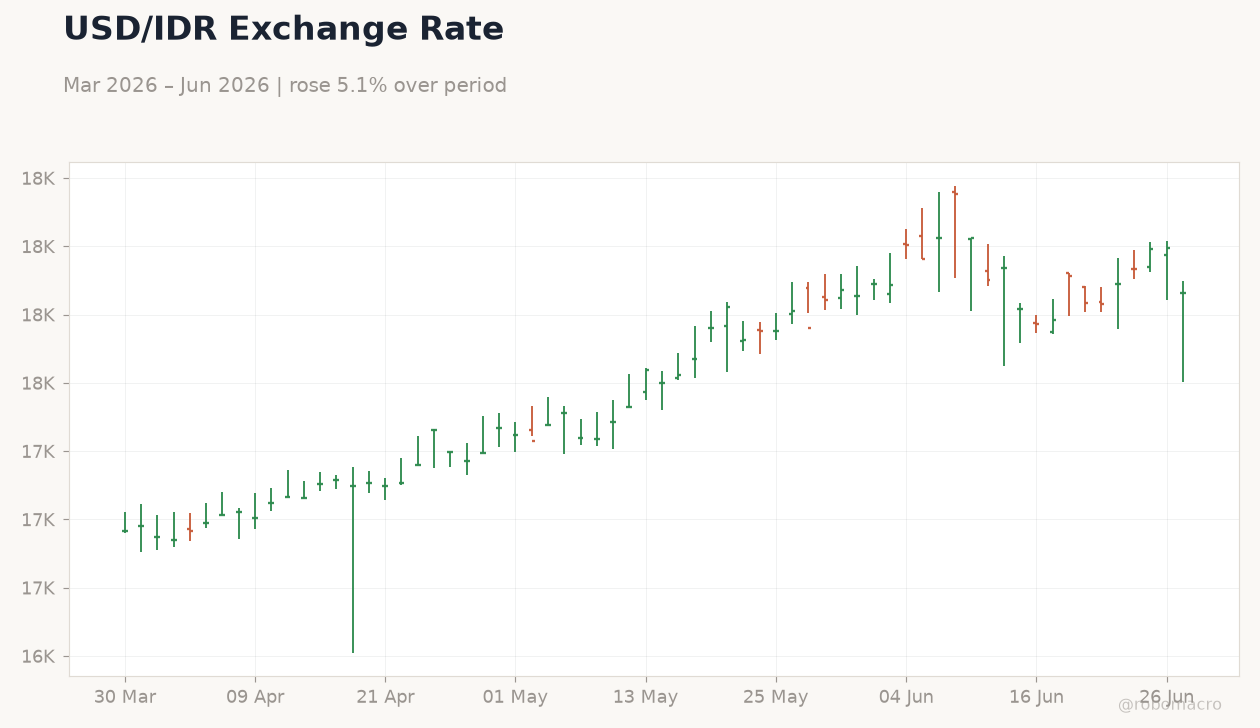

| USD/IDR | 17,830.00 | -0.92% |

| USD/THB | 33.23 | -0.51% |

| USD/MYR | 4.09 | -0.75% |

| USD/PHP | 61.19 | -0.16% |

| USD/SGD | 1.29 | -0.17% |

| Brent Crude | 73.46 | +2.04% |

| Gold | 4,031.00 | -1.17% |

| Bitcoin | 60,258.87 | +1.22% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

USD/IDR Exchange Rate | Type: market_hloc | IDR per USD: 1.783e+04 (2026-06-29) | Range: 1.692e+04–1.819e+04 | Trend(6pt): 1.696e+04,1.712e+04,1.755e+04,1.8e+04,1.8e+04,1.783e+04

USD/IDR Exchange Rate | Type: market_hloc | IDR per USD: 1.783e+04 (2026-06-29) | Range: 1.692e+04–1.819e+04 | Trend(6pt): 1.696e+04,1.712e+04,1.755e+04,1.8e+04,1.8e+04,1.783e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 3.08 | 3.20 | 20:00 |

| Trade Balance | 90m | 1,100m | 20:00 |

- Indonesia draws $9B YTD into central bank bills and bonds while BI ramps up foreign-exchange supervision to anchor the rupiah.

- Bank of Thailand holds policy rate at 1.00% and advances final-stage guidelines for 1:1 baht-backed stablecoins.

- Regional equities close mixed, with JCI falling 1.72% and SET declining 1.04% while KLCI edges 0.24% higher.

Yesterday's Recap

Indonesia equity and currency markets showed divergence as the JCI dropped 1.72% to 5,896.13 amid global risk-off sentiment while the rupiah appreciated 0.92% to 17,830 per dollar on renewed foreign inflows. Bank Indonesia intensified supervision of foreign-exchange carrying to limit speculative pressure and support rupiah stability against Middle East uncertainty. Indonesia attracted $9B year-to-date into central bank bills and sovereign bonds.

In Thailand, the SET fell 1.04% to 1,542.34 after the Bank of Thailand held its benchmark rate at 1.00% and reiterated a cautious outlook tied to Fed policy divergence. Malaysia’s KLCI rose 0.24% to 1,667.74 as MUFG noted policy support limits ringgit downside. Singapore’s STI slipped 0.52% while the Philippine PSEi remained flat.

Brent crude rose 2.04% to $73.46, providing modest support to commodity-linked ASEAN currencies.

The Day Ahead

Indonesia will release inflation and trade balance figures at 20:00 ET, with consensus pointing to a 3.2% year-over-year inflation print and a $1.1B trade surplus. Markets will watch whether hotter-than-expected inflation prompts further BI verbal intervention. Thailand’s central bank is expected to publish final stablecoin regulatory guidelines this week, clarifying 1:1 baht backing requirements for licensed banks.

Malaysia and the Philippines have no major data releases, leaving focus on regional FX flows. Singapore’s MAS will continue monitoring the S$NEER band amid subdued domestic inflation. Vietnam’s SBV is likely to maintain current reserve-adequacy settings given steady FDI inflows.

Other Economic Notes

World Bank projections show Indonesia’s growth easing toward 5% by 2026 as fiscal risks and slower commodity prices weigh on the outlook. Large foreign banks have begun trimming Indonesia exposures, citing policy uncertainty. Supply-chain relocation from China continues to favor Vietnam and Malaysia, though higher US tariffs could compress margins for ASEAN exporters.

Regional bond markets remain supported by lower oil prices anchoring imported inflation across net importers.