ASEAN Macro Daily(Beta Mode)

BI Tightens FX Oversight as Rupiah Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 5,820.79 | -1.28% |

| SET | 1,542.34 | -1.04% |

| KLCI | 1,665.91 | -0.11% |

| PSEi | 6,072.24 | +0.02% |

| STI | 5,208.75 | +0.33% |

| USD/IDR | 17,925.00 | +0.53% |

| USD/THB | 33.27 | +0.06% |

| USD/MYR | 4.08 | +0.21% |

| USD/PHP | 61.28 | +0.40% |

| USD/SGD | 1.29 | +0.19% |

| Brent Crude | 73.47 | +0.44% |

| Gold | 4,020.30 | -0.05% |

| Bitcoin | 58,239.73 | -3.16% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

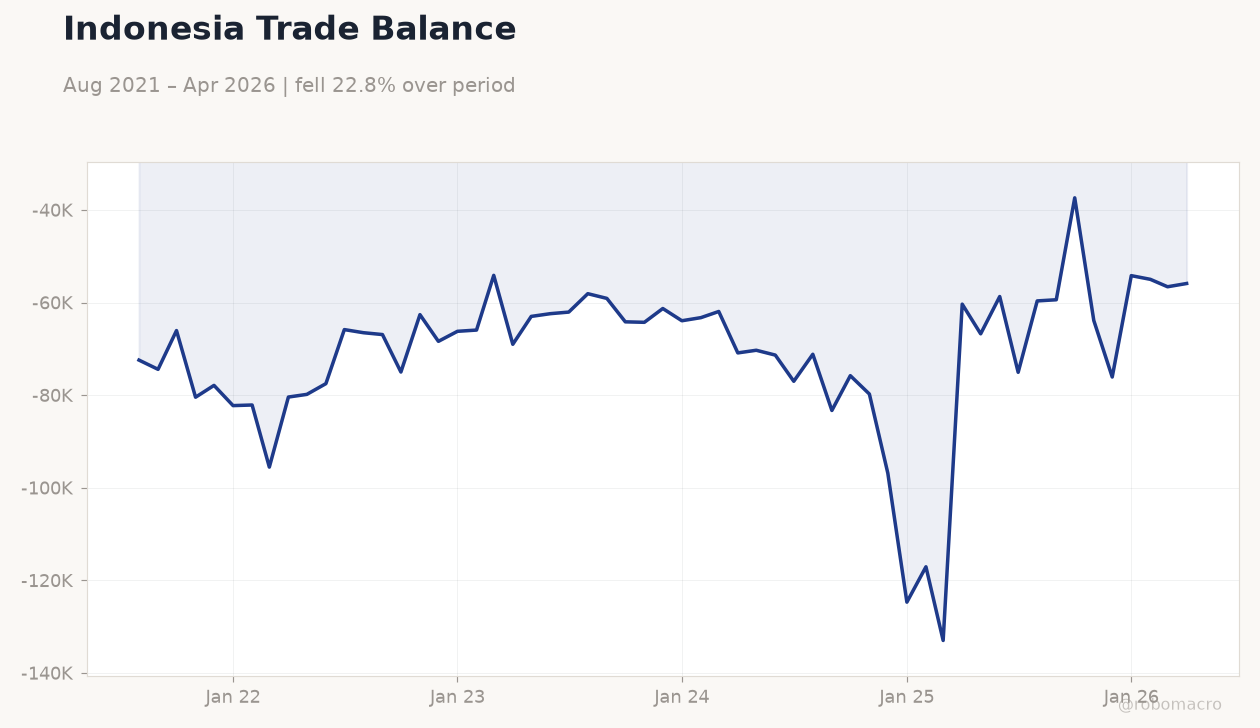

Indonesia Trade Balance | Type: macro_line | Trade Balance USD mn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(5pt): -7.242e+04,-7.5e+04,-6.128e+04,-1.171e+05,-5.588e+04

Indonesia Trade Balance | Type: macro_line | Trade Balance USD mn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(5pt): -7.242e+04,-7.5e+04,-6.128e+04,-1.171e+05,-5.588e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 3.08 | 3.20 | 20:00 |

| Trade Balance | 90m | 1,100m | 20:00 |

| Wednesday (2026-07-01) | |||

| Inflation Rate Year-over-Year | 3.08 | 3.20 | 20:00 |

| Trade Balance | 90m | 1,100m | 20:00 |

- Indonesia’s rupiah fell 0.53% to 17,925 amid Middle East uncertainty and capital-flow concerns, prompting Bank Indonesia to intensify foreign-exchange supervision.

- Regional equities closed lower, with JCI down 1.28% and SET off 1.04%, while Malaysia’s KLCI held near flat and Singapore’s STI rose 0.33%.

- Indonesia’s June inflation and trade-balance prints due tonight carry medium impact, with consensus pointing to a modest CPI uptick and wider surplus.

Yesterday's Recap

Indonesia dominated ASEAN moves as the rupiah weakened on Middle East tensions and news of legal immunity for Danantara bond buyers. Bank Indonesia responded by stepping up short-term measures to shield the economy from global volatility and increasing supervision of foreign-exchange carrying. Foreign banks reportedly scaled back Indonesia exposure, contributing to capital-flight concerns that capped the most-profitable bank’s wealth-management push.

Malaysia’s KLCI edged down just 0.11% while official reserve assets stood at US$130.63 billion at end-May. Thailand’s SET fell 1.04% as baht recovery remained shallow. Singapore’s STI gained 0.33% and the Philippines PSEi was little changed.

Brent crude rose 0.44% to $73.47, offering limited support to commodity-linked currencies.

The Day Ahead

Indonesia releases June inflation and trade-balance data at 20:00 ET, with CPI expected at 3.2% y/y versus 3.08% prior and the trade surplus seen widening to $1.1 billion. No other major ASEAN data prints are scheduled. Bank of Thailand continues its public consultation on 1:1 baht-backed stablecoin rules ahead of a 2026–2027 implementation timeline.

Markets will monitor any further Bank Indonesia comments on rupiah-stability tools. Equity volumes are expected to remain light ahead of the quarter-end.

Other Economic Notes

Thailand and Malaysia are advancing stablecoin frameworks, with Bank of Thailand targeting 2026–2027 rollout and Bank Negara Malaysia already testing ringgit versions with major banks. Malaysia’s May inflation rose to 2.0% on higher electricity costs, while reserve adequacy remains comfortable. Indonesia’s FDI approvals stayed resilient in Q1, yet recent capital outflows highlight vulnerability to global risk sentiment.

Supply-chain shifts from China continue to support Vietnam and Malaysia electronics exports, though ASEAN-wide loan growth faces tighter regulatory scrutiny.