ASEAN Macro Daily(Beta Mode)

Indonesia Inflation Hits 3.34%, Trade Swings to Deficit

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 5,695.12 | +0.92% |

| SET | 1,542.34 | -1.04% |

| KLCI | 1,656.83 | -0.43% |

| PSEi | 6,072.24 | +0.02% |

| STI | 5,161.50 | -0.18% |

| USD/IDR | 17,989.00 | +0.30% |

| USD/THB | 33.17 | -0.27% |

| USD/MYR | 4.08 | -0.13% |

| USD/PHP | 61.49 | +0.30% |

| USD/SGD | 1.29 | -0.18% |

| Brent Crude | 71.58 | +0.01% |

| Gold | 4,138.50 | +1.73% |

| Bitcoin | 61,465.51 | +2.44% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 3.08 | 3.20 | 3.34 |

| Trade Balance | 90m | 1,200m | -1,610m |

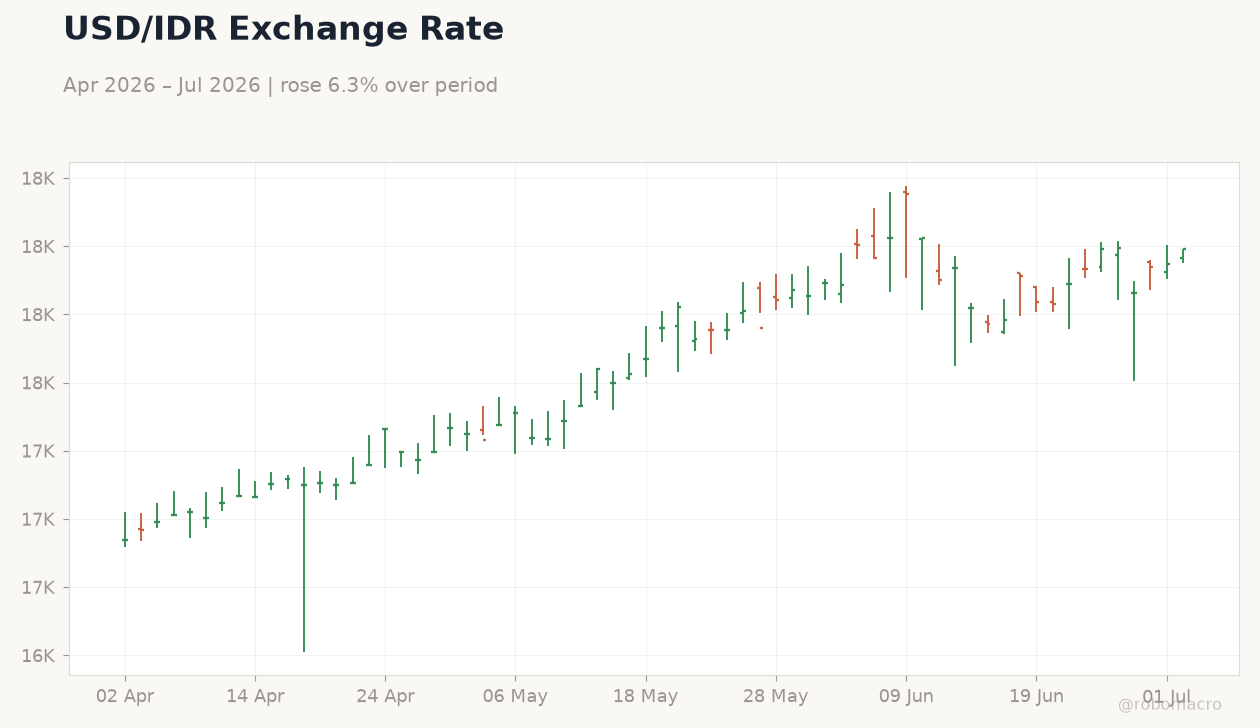

USD/IDR Exchange Rate | Type: market_hloc | IDR per USD: 1.799e+04 (2026-07-02) | Range: 1.692e+04–1.819e+04 | Trend(6pt): 1.692e+04,1.733e+04,1.759e+04,1.819e+04,1.794e+04,1.799e+04

USD/IDR Exchange Rate | Type: market_hloc | IDR per USD: 1.799e+04 (2026-07-02) | Range: 1.692e+04–1.819e+04 | Trend(6pt): 1.692e+04,1.733e+04,1.759e+04,1.819e+04,1.794e+04,1.799e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Indonesia June inflation rose to 3.34% YoY, beating consensus, while trade balance posted a $1.61B deficit.

- JCI gained 0.92% but Rupiah weakened 0.30% to 17,989 amid reserve concerns; SET fell 1.04%.

- Vietnam banks injected over 1.35 trillion VND in H1 credit; Thailand baht supported by stable conditions.

Yesterday's Recap

Indonesia's June inflation accelerated to 3.34% YoY from 3.08%, exceeding the 3.2% consensus and marking a three-month high near Bank Indonesia's upper tolerance band. The trade balance swung sharply to a $1.61 billion deficit versus the $1.2 billion surplus expected, driven by weaker exports. This combination pressured the Rupiah, which depreciated 0.30% to 17,989 per USD and approached the 18,000 psychological level.

Equity markets diverged across the region, with Jakarta's JCI advancing 0.92% to 5,695.12 on selective buying while Bangkok's SET declined 1.04% to 1,542.34. Kuala Lumpur's KLCI eased 0.43% and Singapore's STI slipped 0.18%, while Manila's PSEi held flat. Vietnam recorded continued liquidity support as banks channeled over 1.35 trillion VND into the economy during the first half.

Gold's 1.73% rally offered a partial offset for regional risk sentiment.

The Day Ahead

No major economic releases are scheduled across the six ASEAN economies today, leaving markets to digest Indonesia's latest inflation and trade prints. Focus will remain on Rupiah stability and any Bank Indonesia signals regarding reserve management or capital-flow measures. Thailand's baht is expected to trade range-bound on Commerzbank's assessment of narrowing trade deficits and steady domestic conditions.

Investors will monitor Vietnam's ongoing credit expansion for signs of sustained manufacturing momentum. Regional flows may also react to any fresh US data that shifts rate-cut probabilities and affects carry trades into ASEAN assets.

Other Economic Notes

Indonesia launched a major salt project aimed at lifting domestic production and reducing import reliance in the commodity sector. Malaysia stands to gain from regional currency volatility through shifting trade competitiveness against a weaker Rupiah. Thailand's vehicle output contracted 17.94% YoY in May as exports faced headwinds from Middle East tensions and softer demand.

Upgraded global semiconductor forecasts continue to favor Malaysia and Vietnam's electronics supply chains. Credit expansion in Vietnam remains robust, supporting the country's position as a key FDI destination amid ongoing China-plus diversification.