ASEAN Macro Daily(Beta Mode)

Indonesia Trade Gap Widens, Rupiah Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JCI | 5,875.78 | +2.28% |

| SET | 1,611.28 | +1.11% |

| KLCI | 1,679.05 | +1.04% |

| PSEi | 6,188.03 | +1.02% |

| STI | 5,244.29 | +0.52% |

| USD/IDR | 17,955.00 | +0.94% |

| USD/THB | 33.12 | -0.21% |

| USD/MYR | 4.07 | -0.26% |

| USD/PHP | 61.44 | +0.72% |

| USD/SGD | 1.29 | -0.14% |

| Brent Crude | 72.13 | +0.46% |

| Gold | 4,187.30 | +1.81% |

| Bitcoin | 63,014.80 | -0.12% |

| Indonesia 10Y Govt Yield | - | - |

| Thailand 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

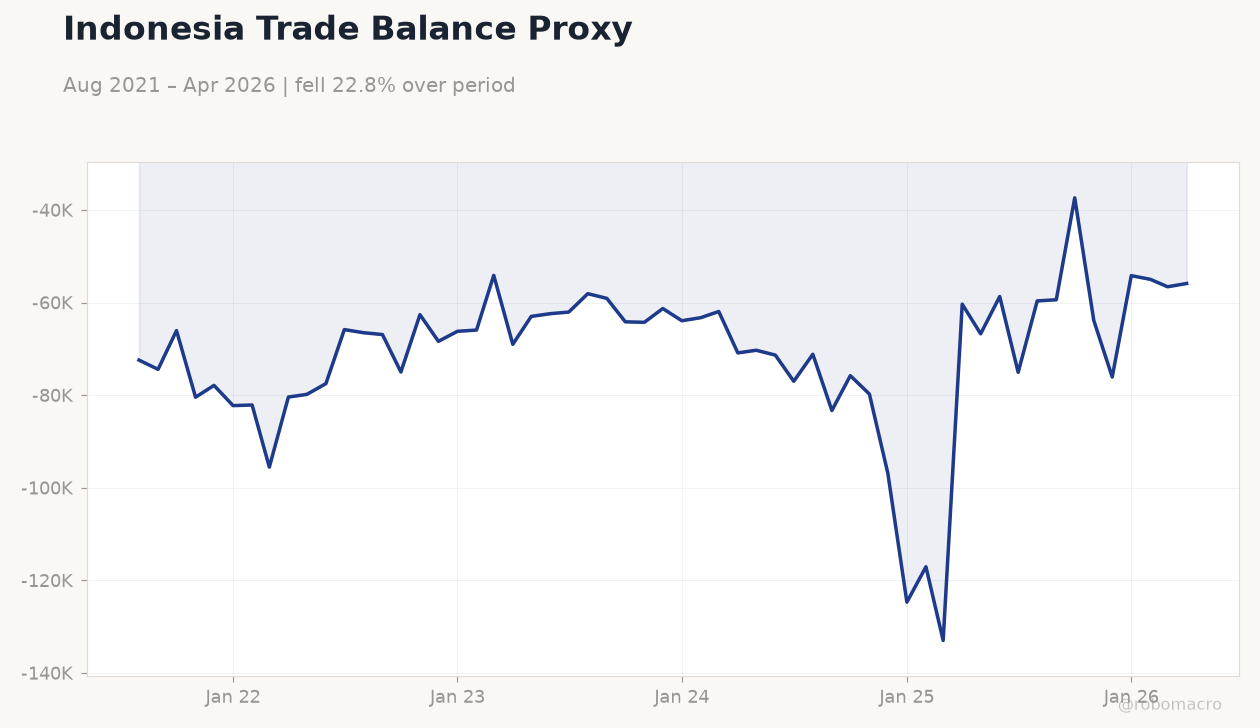

Indonesia Trade Balance Proxy | Type: macro_line | Trade Bal. USD bn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(5pt): -7.242e+04,-7.5e+04,-6.128e+04,-1.171e+05,-5.588e+04

Indonesia Trade Balance Proxy | Type: macro_line | Trade Bal. USD bn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(5pt): -7.242e+04,-7.5e+04,-6.128e+04,-1.171e+05,-5.588e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 6.80 | - | 21:00 |

| Headline Unemployment Rate | 4.70 | - | 21:00 |

- Indonesia records trade deficit, pushing USD/IDR up 0.94% to 17,955 and raising stagflation concerns after manufacturing PMI hits one-year low

- Regional equities advance led by JCI +2.28% and SET +1.11%, while USD/THB and USD/MYR ease modestly

- Philippines inflation and unemployment data due in coming sessions; Vietnam upgraded to upper-middle-income status by World Bank

Yesterday's Recap

Indonesia dominated ASEAN news flow as May trade data showed a widening deficit that triggered fresh selling in the rupiah. The currency closed 0.94% weaker at 17,955 per USD amid concerns over external balances and domestic sentiment. Indonesia’s manufacturing activity printed at a one-year low, stoking stagflation fears and keeping Bank Indonesia on alert for further rupiah pressure.

Equity markets posted broad gains despite thin volumes, with JCI rising 2.28% to 5,875.78, SET adding 1.11% to 1,611.28, KLCI up 1.04%, PSEi +1.02%, and STI +0.52%. USD/THB fell 0.21% and USD/MYR declined 0.26%, while Brent crude edged 0.46% higher to 72.13 and gold jumped 1.81% to 4,187.30. Malaysia’s ringgit faced additional near-term headwinds from election-related noise according to OCBC.

The Day Ahead

Philippines will release June inflation year-over-year and headline unemployment rate, both carrying medium market impact and likely to influence BSP policy expectations. No major data releases are scheduled for Indonesia, Thailand, Malaysia, Singapore or Vietnam. Market participants will monitor any follow-through commentary on Indonesia’s trade balance and potential central-bank verbal intervention.

Regional equity and FX flows may remain sensitive to global commodity moves given the heavy weighting of nickel, palm oil and electronics in ASEAN exports.

Other Economic Notes

Vietnam received a World Bank upgrade to upper-middle-income status, reflecting sustained FDI inflows and strong electronics exports. Thailand continued efforts to expand QR-payment acceptance for tourists while exploring a baht stablecoin pilot. Malaysia’s electrical and electronics shipments remained firm, supporting the view that supply-chain shifts from China continue to benefit ASEAN manufacturers.

Indonesia’s banking sector faces indirect pressure from the trade shortfall, with deposit and lending dynamics likely to stay in focus.

Global Macro News

Rising gold and Brent prices provided a mild tailwind to commodity-linked ASEAN currencies and equities. <i>↓ p.2</i>