Andeans Macro Daily(Beta Mode)

Andean FX Weakens Amid Commodity Dip

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 38.06 | -4.28% |

| MSCI Peru | 74.27 | -3.08% |

| USD/COP | 3,715.91 | +0.68% |

| USD/CLP | 926.13 | +1.20% |

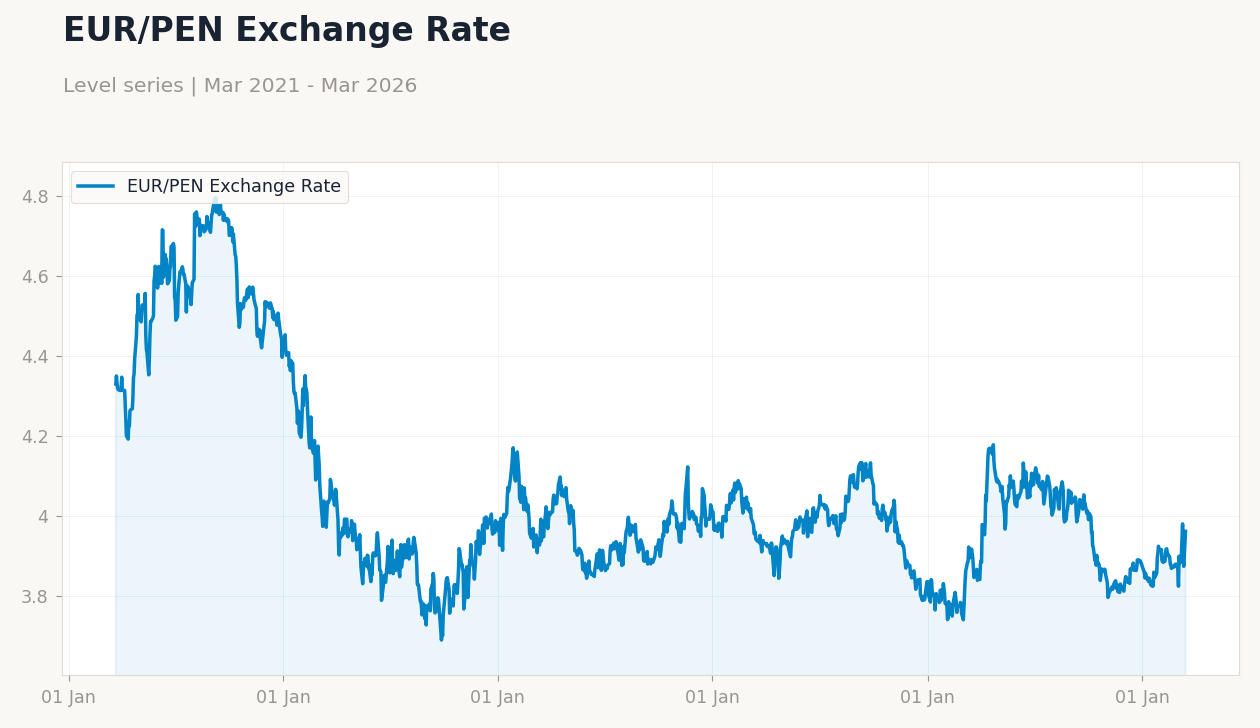

| USD/PEN | 3.48 | +1.46% |

| Copper | 5.37 | -1.08% |

| Gold | 4,574.90 | -0.56% |

| Brent Crude | 106.41 | -2.06% |

| Bitcoin | 70,276.18 | -0.35% |

| Colombia 10Y Govt Yield | - | - |

| Chile Short-term Rate | 4.50% | -3.02% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

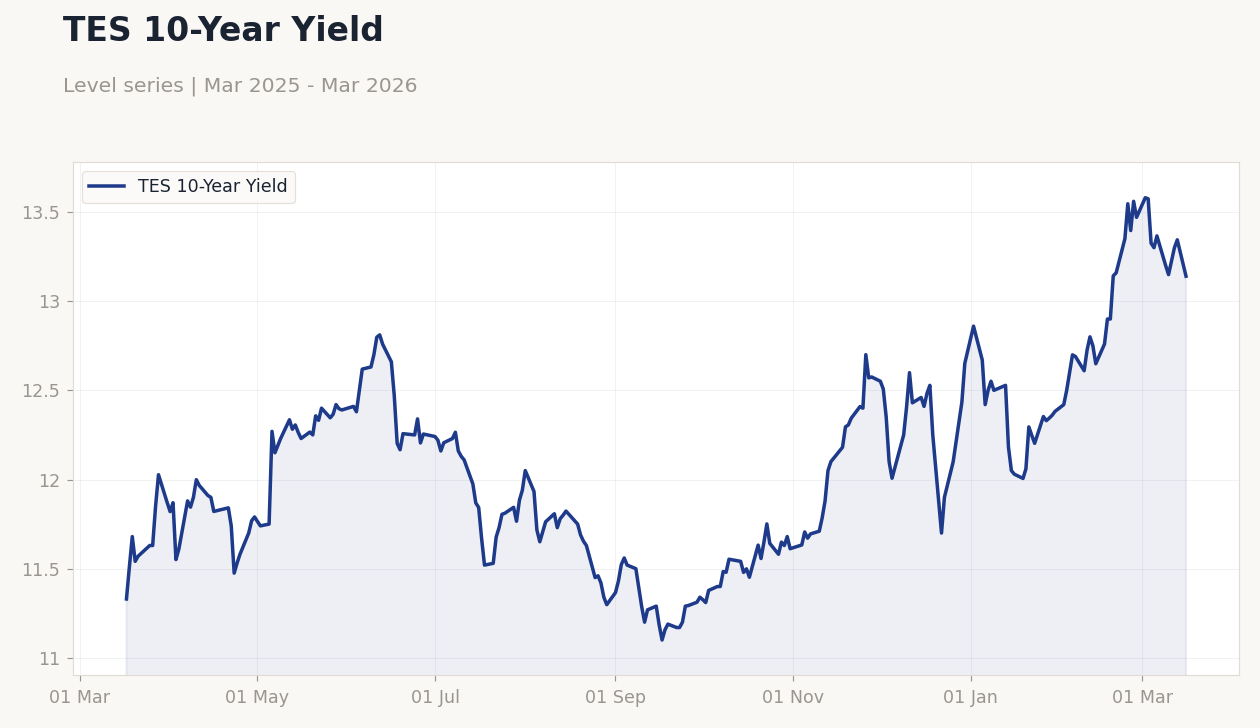

TES 10-Year Yield | Type: macro_line | TES 10-Year Yield: 13.14 (2026-03-16) | Range: 11.1–13.58 | Trend(6pt): 11.33,12.66,11.27,12.6,13.3,13.14

TES 10-Year Yield | Type: macro_line | TES 10-Year Yield: 13.14 (2026-03-16) | Range: 11.1–13.58 | Trend(6pt): 11.33,12.66,11.27,12.6,13.3,13.14

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Andean currencies depreciated against the USD, with CLP and PEN seeing the sharpest declines amid falling commodity prices.

- Equity markets in Chile and Peru dropped over 3%, while Colombia's held flat, reflecting oil's lesser slide.

- Global tensions from Iran conflict pressured energy and metals, impacting Andean export revenues.

Yesterday's Recap

Andean markets faced headwinds on March 20 as commodity prices softened, leading to currency depreciations across the board. In Chile, the MSCI Chile index fell 4.28% to 38.06, driven by a 1.08% drop in copper prices to $5.37 per pound, a key export for the country. Peru's MSCI Peru index declined 3.08% to 74.27, similarly hit by the copper dip and a 0.56% fall in gold to $4,574.90 per ounce, exacerbating the USD/PEN rise of 1.46% to 3.48.

Colombia's MSCI Colombia index remained unchanged at 9.02, cushioned somewhat by Brent crude's 2.06% decline to $106.41 per barrel, though USD/COP still climbed 0.68% to 3,715.91. Chile's short-term rate adjusted to 4.50%, down 3.02%, signaling potential easing amid economic pressures. Overall, the lack of major data releases shifted focus to external factors, with Andean assets underperforming amid broader EM volatility.

No significant fiscal or mining updates emerged, but lithium sector watchers noted ongoing supply chain strains in Chile.

The Day Ahead

With no scheduled economic releases for March 21 across Colombia, Chile, or Peru, markets will likely monitor global commodity trends for directional cues. Attention may turn to any unscheduled statements from Andean central banks, particularly if FX volatility persists. In Chile, traders could eye copper inventory reports that might influence CLP movements.

Peru's gold and mining sectors remain sensitive to overnight metals pricing. Broader Andean focus will include potential spillover from LatAm peers like Brazil's inflation data. Expect quiet trading unless external shocks from the Iran conflict escalate.

Other Economic Notes

Broader Andean themes highlight vulnerability to commodity cycles, with Chile and Peru's reliance on copper and gold amplifying FX risks amid global downturns. Colombia's oil-dependent economy faces balanced pressures from Brent's decline, potentially straining fiscal balances if prolonged. Emerging lithium developments in Chile offer long-term diversification but require stable political reforms to attract investment.