Andeans Macro Daily(Beta Mode)

Andean Stocks Mixed, Peru Dives on PEN Slump

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 43.94 | +0.21% |

| MSCI Peru | 82.87 | -4.85% |

| USD/COP | 3,608.15 | +0.37% |

| USD/CLP | 885.38 | -0.10% |

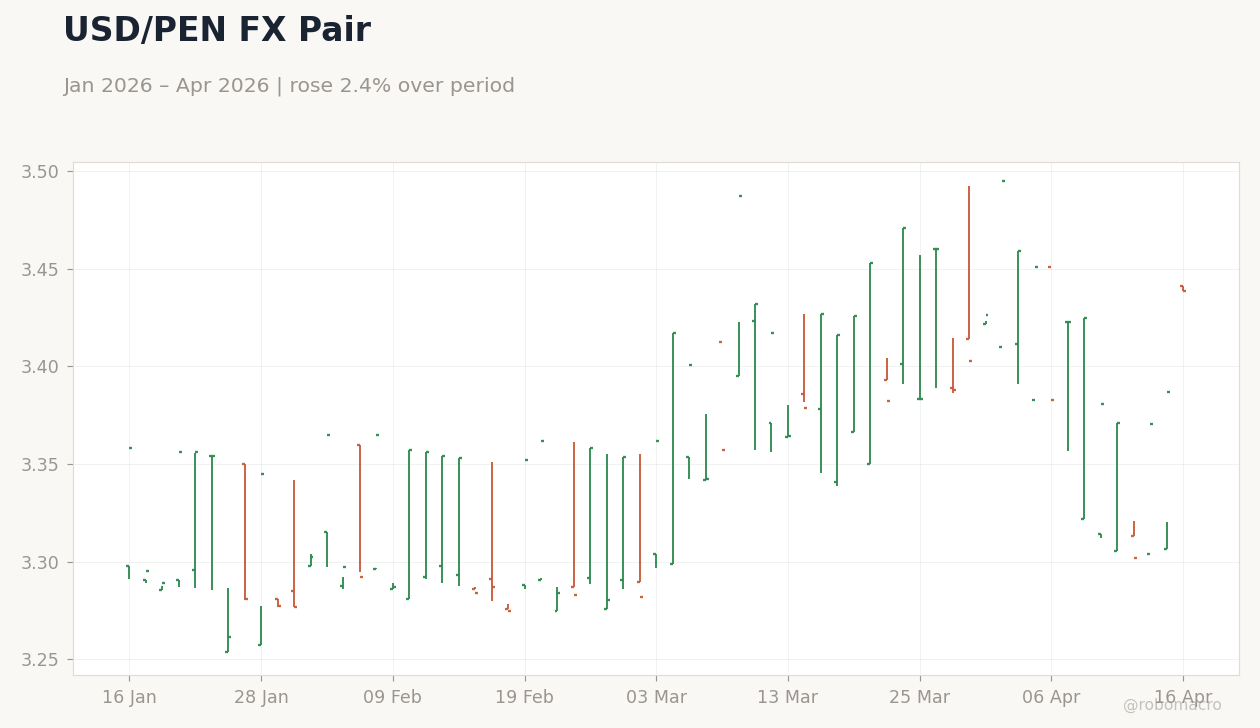

| USD/PEN | 3.44 | +1.53% |

| Copper | 6.08 | +0.12% |

| Gold | 4,840.00 | +0.83% |

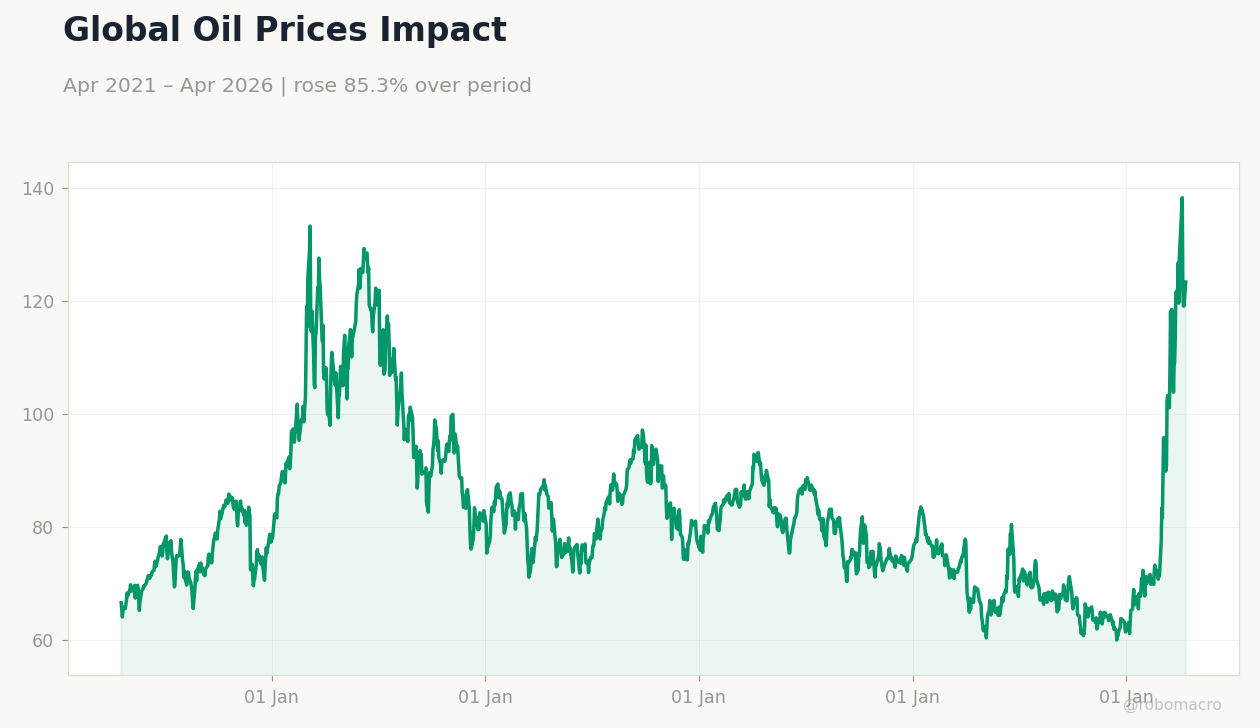

| Brent Crude | 95.64 | +0.75% |

| Bitcoin | 74,335.05 | -0.63% |

| Colombia 10Y Govt Yield | - | - |

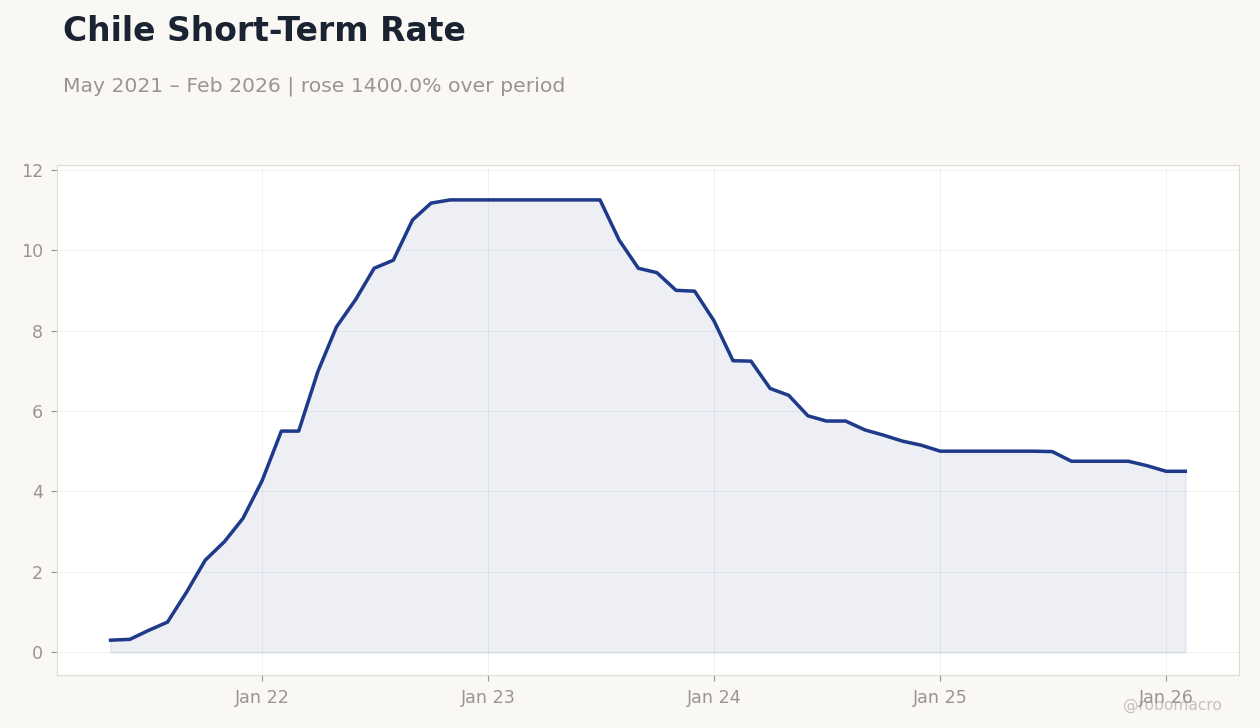

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Short-Term Rate | Type: macro_line | Chile Rate: 4.5 (2026-02-01) | Range: 0.3–11.25 | Trend(5pt): 0.3,9.55,9.55,5.25,4.5

Chile Short-Term Rate | Type: macro_line | Chile Rate: 4.5 (2026-02-01) | Range: 0.3–11.25 | Trend(5pt): 0.3,9.55,9.55,5.25,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Peruvian equities plunged amid PEN depreciation and global uncertainty, while Chilean stocks edged higher on copper gains.

- Colombian peso weakened slightly with flat equities, as oil prices firmed but fiscal concerns persisted.

- Commodities supported Andean exporters, with copper and gold up modestly despite broader FX pressures.

Yesterday's Recap

Andean markets showed mixed performance on April 15, with MSCI Peru dropping sharply by 4.85% to 82.87, driven by a 1.53% weakening of the PEN to 3.44 against the USD amid political noise and commodity volatility. In Chile, MSCI Chile rose 0.21% to 43.94, buoyed by a 0.12% increase in copper prices to 6.08, which offset a minor 0.10% appreciation of the CLP to 885.38 versus the USD. Colombian equities via MSCI Colombia held flat at 9.02 with a 0.00% change, as the COP depreciated 0.37% to 3,608.15 against the USD, tempered by a 0.75% rise in Brent crude to 95.64.

Gold prices climbed 0.83% to 4,840.00, providing some reserve support for Peru and Colombia, though Bitcoin fell 0.63% to 74,335.05, minimally impacting crypto-related hedges in Chile. No major data releases occurred across the bloc, but commodity moves highlighted Chile and Peru's export reliance, while Colombia faced ongoing pressure from fiscal deficit worries. Sovereign yields were stable, with Chile's short-term rate unchanged at 4.50%, reflecting cautious investor sentiment.

The Day Ahead

The Andean calendar remains quiet on April 16, with no scheduled data releases or events for Colombia, Chile, or Peru, allowing markets to digest recent FX and commodity shifts. Investors will monitor global cues, particularly any updates on Middle East tensions that could influence oil and copper prices critical to the region. In Chile, attention may turn to potential lithium sector developments, given emerging battery supply chain talks.

Peru could see continued PEN volatility if political risks escalate, while Colombia's focus stays on fiscal reform progress. Overall, a light day positions Andean assets to track broader LatAm and commodity trends.

Other Economic Notes

Broader Andean themes center on commodity dependence, with copper's stability aiding Chile and Peru's fiscal balances amid global demand uncertainties. Inflation pressures remain elevated in Colombia due to persistent supply shocks, contrasting with Chile's cooling trajectory post-aggressive rate cuts. Political risks, including reform agendas in Peru and fiscal debates in Colombia, continue to weigh on investor confidence and sovereign spreads.