Andeans Macro Daily(Beta Mode)

Chilean Reforms Boost Stocks as Copper Dips

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 44.97 | +1.47% |

| MSCI Peru | 85.17 | +0.61% |

| USD/COP | 3,596.34 | -0.46% |

| USD/CLP | 878.60 | -0.85% |

| USD/PEN | 3.43 | +1.79% |

| Copper | 6.02 | -1.42% |

| Gold | 4,812.00 | -0.94% |

| Brent Crude | 95.19 | +5.32% |

| Bitcoin | 75,157.35 | +1.76% |

| Colombia 10Y Govt Yield | - | - |

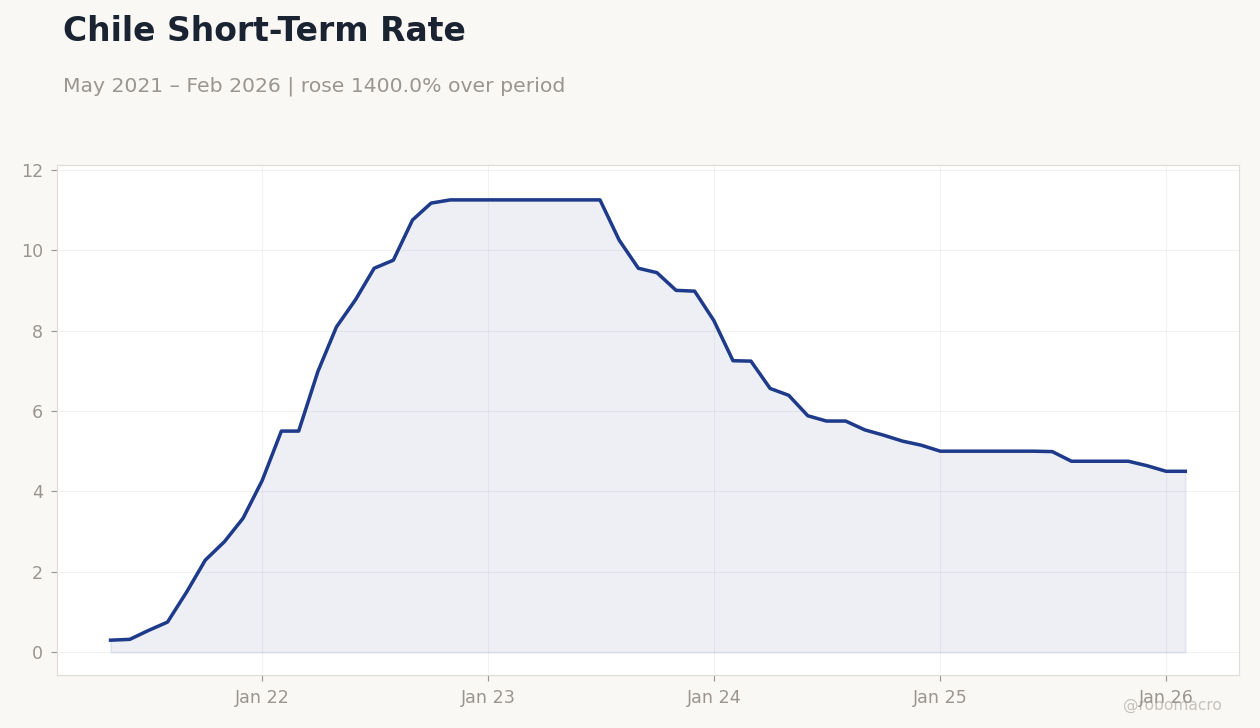

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Short-Term Rate | Type: macro_line | Chile Policy Rate (%): 4.5 (2026-02-01) | Range: 0.3–11.25 | Trend(5pt): 0.3,9.55,9.55,5.25,4.5

Chile Short-Term Rate | Type: macro_line | Chile Policy Rate (%): 4.5 (2026-02-01) | Range: 0.3–11.25 | Trend(5pt): 0.3,9.55,9.55,5.25,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Chilean stocks rose on Kast's tax overhaul, offsetting copper's decline amid US-Iran tensions.

- Peruvian sol depreciated sharply despite slight equity gains; Colombia's peso firmed on oil surge.

- Brent crude jumped 5.32%, aiding Colombian assets, while global risk appetite lifted Bitcoin.

Yesterday's Recap

Andean markets displayed mixed results, with Chile outperforming on domestic policy developments. MSCI Chile advanced 1.47% to 44.97, fueled by President Kast's ambitious tax and spending reforms targeting budget balance, potentially bolstering fiscal health in the copper-reliant nation. MSCI Peru increased 0.61% to 85.17, but the USD/PEN rose 1.79% to 3.43, amid heightened political tensions from the tight presidential runoff between ultraconservative and leftist contenders.

MSCI Colombia remained unchanged at 9.02, buoyed by Brent crude's 5.32% rise to 95.19, benefiting oil major Ecopetrol, while USD/COP declined 0.46% to 3,596.34 as the peso gained ground. USD/CLP fell 0.85% to 878.60, reflecting some currency strength despite commodity pressures. Copper decreased 1.42% to 6.02, impacting mining sectors in Chile and Peru, where Chile's short-term rate held steady at 4.50%.

Gold slipped 0.94% to 4,812.00, slightly denting Peru's export outlook. Commodity splits underscored fiscal risks, particularly for Chile's mining royalties if copper remains subdued.

The Day Ahead

No significant economic events are slated for April 20 in the Andean region, providing space for markets to process recent commodity shifts and geopolitical news. Attention may center on progress in Chile's economic reform package under President Kast, which could affect CLP dynamics and bond yields. In Peru, the unresolved presidential election could sustain volatility in USD/PEN.

Colombia's assets might react to updates from the Santa Marta climate conference, influencing energy policy views. Globally, US-Iran developments could sway oil and metals prices, with potential for low-volume trading absent major catalysts.

Other Economic Notes

Andean economies remain tied to commodities, leaving Chile and Peru exposed to copper fluctuations driven by global factors like Chinese demand. Colombia gains from Brent upticks, yet needs fiscal adjustments to address deficits around 4% of GDP. Chile's emerging battery storage initiatives, such as the new 1,500 MWh project, point to diversification but contend with market oversupply.

Regional trade links, including with Brazil facing economic challenges, add to external vulnerabilities for Peru and others.