Andeans Macro Daily(Beta Mode)

Andean Stocks Dip, Copper Rebounds

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 41.09 | -2.38% |

| MSCI Peru | 77.56 | -1.52% |

| USD/COP | 3,619.63 | +0.26% |

| USD/CLP | 905.65 | +1.63% |

| USD/PEN | 3.52 | +0.21% |

| Copper | 5.99 | +1.85% |

| Gold | 4,656.30 | +2.44% |

| Brent Crude | 102.24 | -13.38% |

| Bitcoin | 76,115.98 | +0.45% |

| Colombia 10Y Govt Yield | - | - |

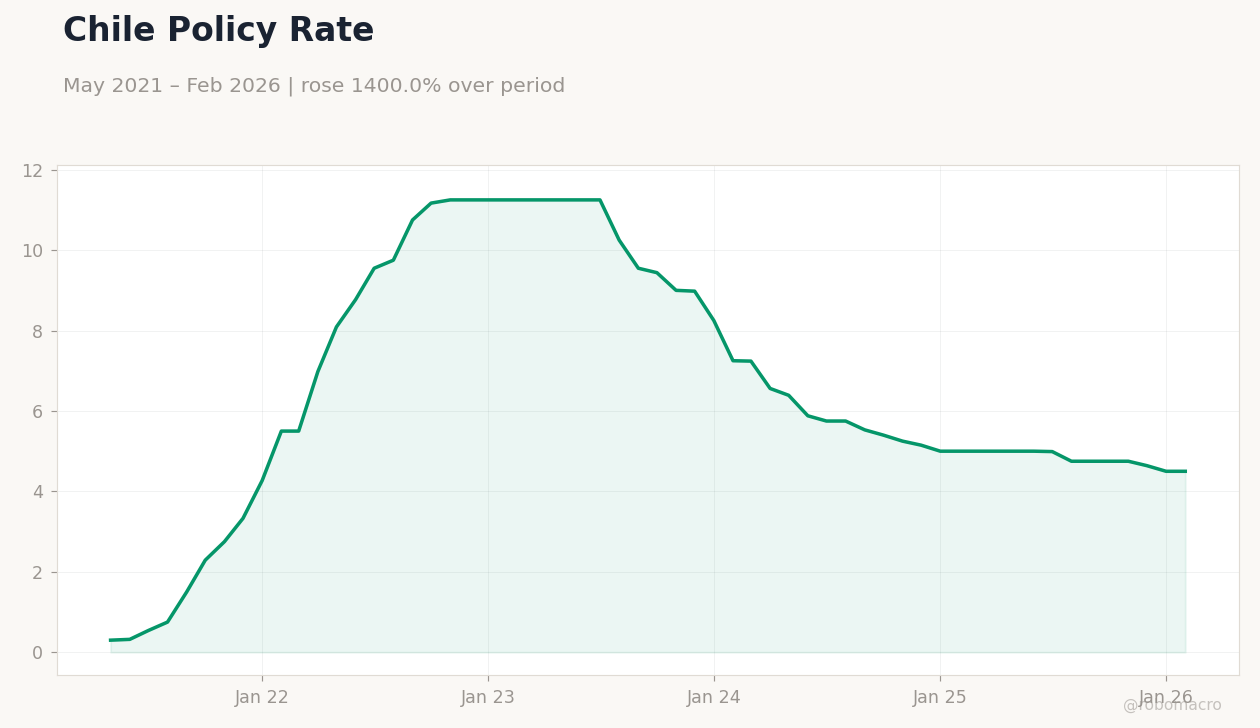

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Prices | Type: macro_line | Brent Price USD/bbl: 113.9 (2026-04-27) | Range: 59.93–138.2 | Trend(5pt): 68.91,111.5,90.73,78.01,113.9

Brent Crude Prices | Type: macro_line | Brent Price USD/bbl: 113.9 (2026-04-27) | Range: 59.93–138.2 | Trend(5pt): 68.91,111.5,90.73,78.01,113.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Andean equities mostly declined amid commodity volatility and USD strength, with Chile and Peru facing steeper losses.

- FX rates weakened against the dollar, driven by global risk-off moves and local economic pressures.

- Commodities mixed: copper and gold rose, while Brent crude fell sharply, impacting regional exporters.

Yesterday's Recap

Andean markets saw mixed performance on April 29, 2026, with MSCI Chile dropping 2.38% to 41.09, pressured by prior copper weakness and domestic inflation concerns following fuel price hikes. MSCI Peru fell 1.52% to 77.56, hit by emerging market selloffs despite gold's supportive gains for mining. MSCI Colombia remained flat at 9.02 with a 0.00% change, cushioned by stable oil trends but vulnerable to fiscal worries.

FX pairs depreciated versus the USD: USD/COP increased 0.26% to 3,619.63, USD/CLP rose 1.63% to 905.65, and USD/PEN climbed 0.21% to 3.52, reflecting dollar strength amid global tensions. Commodities diverged notably—copper gained 1.85% to 5.99, providing relief to Chile and Peru's export sectors after recent declines; gold advanced 2.44% to 4,656.30, bolstering Peru's output and Colombia's reserves; Brent crude plunged 13.38% to 102.24, potentially straining Colombia's energy revenues and fiscal transfers. Bitcoin edged up 0.45% to 76,115.98, showing mild resilience.

Chile's short-term rate held steady at 4.50% with no change, amid ongoing inflation debates.

The Day Ahead

No significant economic data releases are scheduled for April 30, 2026, leaving markets attuned to commodity price movements, especially copper and gold trends affecting Chile and Peru. Focus may shift to Colombia's presidential election dynamics, with surging rebel attacks and debates on peace versus war strategies influencing sentiment. Regional spillovers from Brazil's rate cut could impact Andean FX, while updates on Chile's inflation polls and fuel prices may drive local reactions.

A light calendar implies volatility tied to global factors, such as U.S. economic resilience and energy shocks from Iran tensions.

Other Economic Notes

Andean economies remain heavily tied to commodities, with Chile and Peru exposed to copper fluctuations amid signs of Chinese factory output recovery offsetting global pessimism. Colombia grapples with political uncertainty from the upcoming election, where choices on armed conflict resolution could affect fiscal stability and investor inflows. Initiatives like Brazil's cooperation with the ILO on the care economy may inspire similar policies in the Andeans, potentially enhancing labor participation and addressing gender gaps.

(cont...)