Andeans Macro Daily(Beta Mode)

Copper Rally Bolsters Andean Fiscal Outlooks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 39.38 | -1.13% |

| MSCI Peru | 79.31 | -1.13% |

| USD/COP | 3,772.75 | -0.65% |

| USD/CLP | 906.50 | +0.67% |

| USD/PEN | 3.42 | +0.03% |

| Copper | 6.24 | +1.16% |

| Gold | 4,497.30 | -0.20% |

| Brent Crude | 108.49 | -2.51% |

| Bitcoin | 77,416.67 | +0.87% |

| Colombia 10Y Govt Yield | - | - |

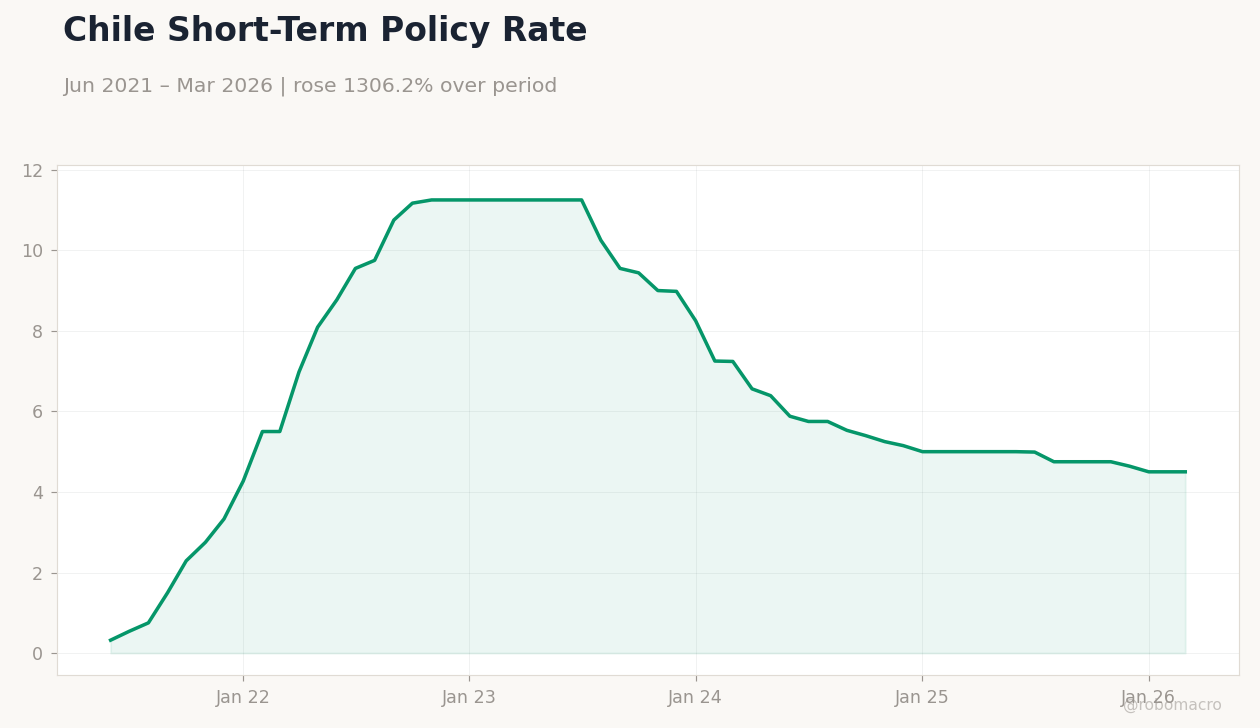

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

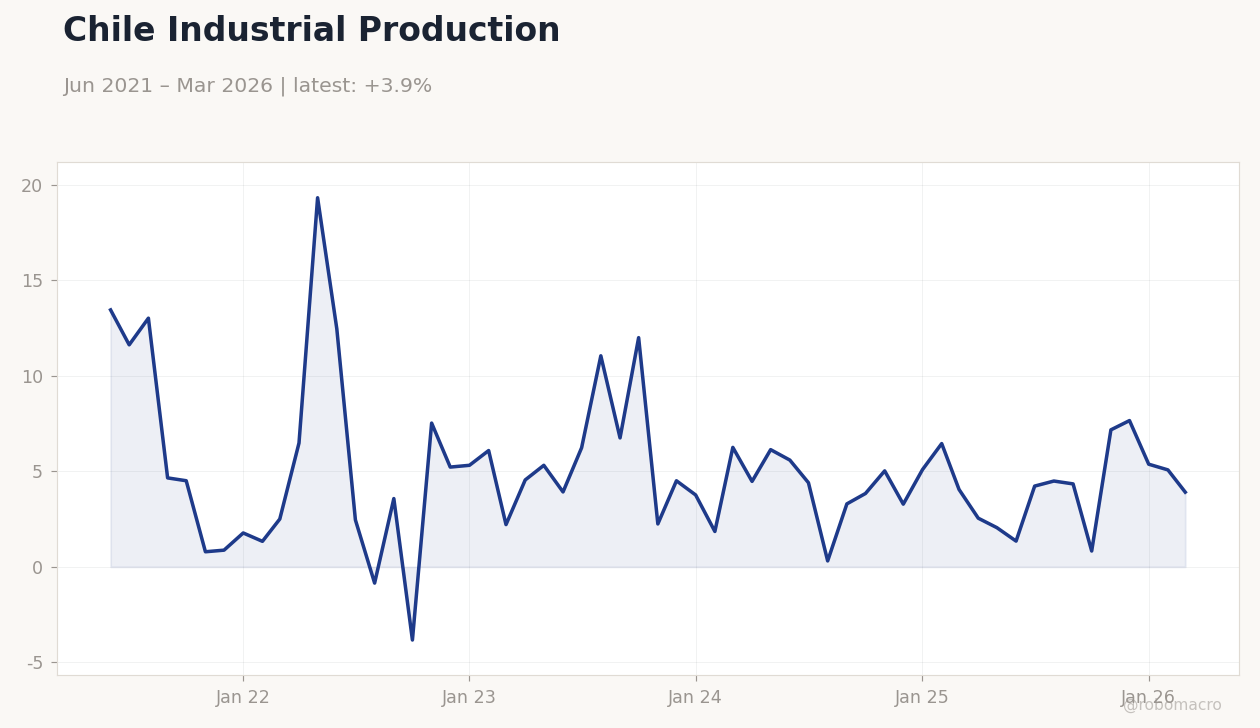

Chile Industrial Production | Type: macro_line | YoY %: 3.911 (2026-03-01) | Range: -3.835–19.33 | Trend(6pt): 13.46,-0.8528,12,3.282,5.077,3.911

Chile Industrial Production | Type: macro_line | YoY %: 3.911 (2026-03-01) | Range: -3.835–19.33 | Trend(6pt): 13.46,-0.8528,12,3.282,5.077,3.911

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Copper advanced 1.16% to $6.24/lb, supporting Chile and Peru fiscal balances while Brent crude fell 2.51%.

- MSCI Chile and MSCI Peru each declined 1.13%, whereas MSCI Colombia held flat at 9.02.

- COP strengthened 0.65% to 3,772.75; CLP weakened 0.67% to 906.50 and PEN edged up 0.03%.

Yesterday's Recap

Andean equity markets closed mixed on May 19. MSCI Chile fell 1.13% to 39.38 and MSCI Peru dropped 1.13% to 79.31 despite copper’s 1.16% gain to 6.24. MSCI Colombia remained unchanged at 9.02 amid range-bound Brent crude that settled 2.51% lower at 108.49.

In FX, USD/COP declined 0.65% to 3,772.75 while USD/CLP rose 0.67% to 906.50 and USD/PEN inched 0.03% higher to 3.42. Chile’s short-term rate held at 4.50%. No major data releases occurred across the three economies, leaving commodity price action as the dominant driver of daily moves.

The Day Ahead

Markets enter a quiet period with no scheduled releases for Colombia, Chile or Peru on May 20-21. Attention will remain on copper and oil price developments that directly affect fiscal revenues and current-account balances. Traders will also monitor any follow-through in CLP and COP after yesterday’s commodity-led moves.

Central-bank speakers from BCCh and BanRep could provide incremental guidance on the pace of easing. Thin data calendars typically amplify the market impact of any surprise global risk signals.

Other Economic Notes

Elevated copper prices continue to widen Chile’s trade surplus and bolster royalty collections that ease compliance with the fiscal rule. Peru benefits similarly from firm gold and copper realizations that support reserve accumulation and keep the current account in surplus. Colombia’s external position remains more sensitive to Brent crude swings given its heavier oil dependence.

Lithium price softness exerts only marginal pressure on Chilean revenues at present. Regional equities remain correlated with global commodity sentiment rather than domestic policy surprises.

Global Macro News

Stronger Chinese industrial readings lifted copper and reinforced terms-of-trade gains for Chile and Peru. Brent’s sharp decline weighed on Colombia’s fiscal outlook and kept COP relatively bid. Global equity volatility stayed contained, limiting spillovers into Andean credit spreads.

The ECB Deposit Rate stood at 2.00% and Eurozone unemployment at 6.70%, providing a stable external backdrop that reduced pressure on emerging-market currencies. <i>↓ p.2</i>