Andeans Macro Daily(Beta Mode)

Andean Stocks Climb on Copper, Oil Rallies

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 40.75 | +0.39% |

| MSCI Peru | 83.51 | +1.80% |

| USD/COP | 3,680.50 | -1.19% |

| USD/CLP | 897.73 | -0.81% |

| USD/PEN | 3.41 | -0.11% |

| Copper | 6.33 | +1.19% |

| Gold | 4,515.70 | -0.53% |

| Brent Crude | 105.44 | +2.79% |

| Bitcoin | 77,137.99 | -0.52% |

| Colombia 10Y Govt Yield | - | - |

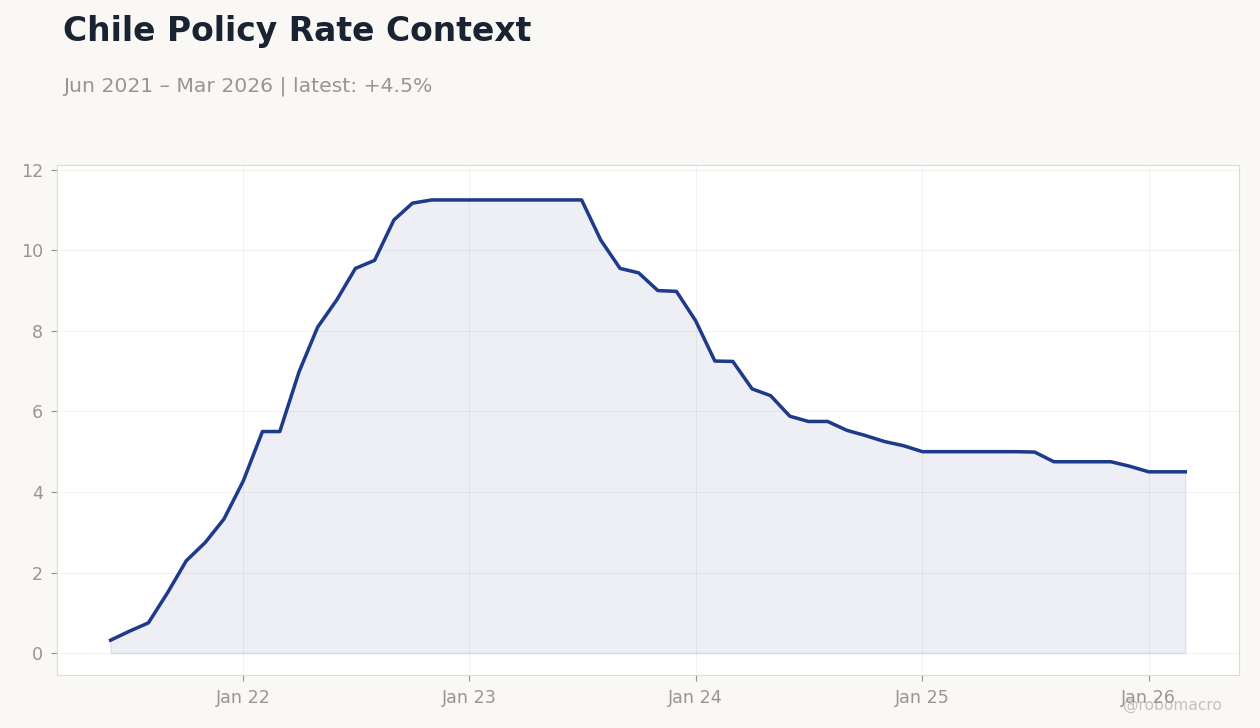

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Policy Rate Context | Type: macro_line | Short Rate %: 4.5 (2026-03-01) | Range: 0.32–11.25 | Trend(5pt): 0.32,9.75,9.44,5.15,4.5

Chile Policy Rate Context | Type: macro_line | Short Rate %: 4.5 (2026-03-01) | Range: 0.32–11.25 | Trend(5pt): 0.32,9.75,9.44,5.15,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI Peru surges 1.80% to 83.51 as copper advances.

- Regional currencies strengthen with USD/COP down 1.19%.

- Brent crude jumps 2.79%, supporting Colombia’s fiscal position.

Yesterday's Recap

No economic data releases occurred in Colombia, Chile or Peru on May 21. Equity markets posted gains led by Peru. MSCI Peru climbed 1.80% to 83.51 while MSCI Chile advanced 0.39% to 40.75 on firmer mining shares.

MSCI Colombia remained flat at 9.02. The Colombian peso led regional FX moves, with USD/COP falling 1.19% to 3,680.50. USD/CLP fell 0.81% to 897.73 and USD/PEN eased 0.11% to 3.41.

Copper rose 1.19% to 6.33, lifting export revenue expectations for Chile and Peru, while Brent crude surged 2.79% to 105.44, narrowing Colombia’s projected current-account gap. Gold slipped 0.53% to 4,515.70 and Bitcoin fell 0.52% to 77,137.99. Chile’s short-term rate held steady at 4.50%.

The Day Ahead

The economic calendar stays empty through May 23 with no releases scheduled in any Andean country. Market participants will track central-bank speeches and global commodity signals. BCRP officials may comment on recent activity strength that supports holding the policy rate.

BCCh minutes could clarify the pace of further easing. Colombia’s BanRep will likely stay in wait-and-see mode pending fresh inflation prints. Traders will also monitor US-China trade headlines for their impact on copper demand.

Other Economic Notes

Copper and oil price swings continue to dominate fiscal and external accounts in the region. Chile’s short-term rate held at 4.50%, consistent with ongoing monetary easing. Peru’s stronger mining volumes are widening the current-account surplus while supporting royalty income.

Colombia benefits from higher oil receipts that ease pressure on the fiscal deficit. Lithium market softness remains a secondary concern for Chilean producers.

Global Macro News

Global commodity markets provided the main external impulse for Andean assets. Copper prices climbed on supply concerns and AI-driven demand, directly supporting Chile and Peru. Brent crude strength aided Colombia’s trade balance and sovereign spreads.

The ECB kept its deposit rate at 2.00%, leaving euro-area financial conditions steady. Eurozone unemployment stood at 6.70%, indicating limited imported disinflation pressure. <i>↓ p.2</i>