Andeans Macro Daily(Beta Mode)

Peru, Chile Stocks Rally as FX Diverges

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 41.47 | +2.93% |

| MSCI Peru | 86.01 | +4.13% |

| USD/COP | 3,667.69 | +0.97% |

| USD/CLP | 893.35 | -0.37% |

| USD/PEN | 3.41 | +2.05% |

| Copper | 6.36 | -0.06% |

| Gold | 4,478.70 | -0.48% |

| Brent Crude | 94.31 | -5.29% |

| Bitcoin | 75,848.23 | +0.03% |

| Colombia 10Y Govt Yield | - | - |

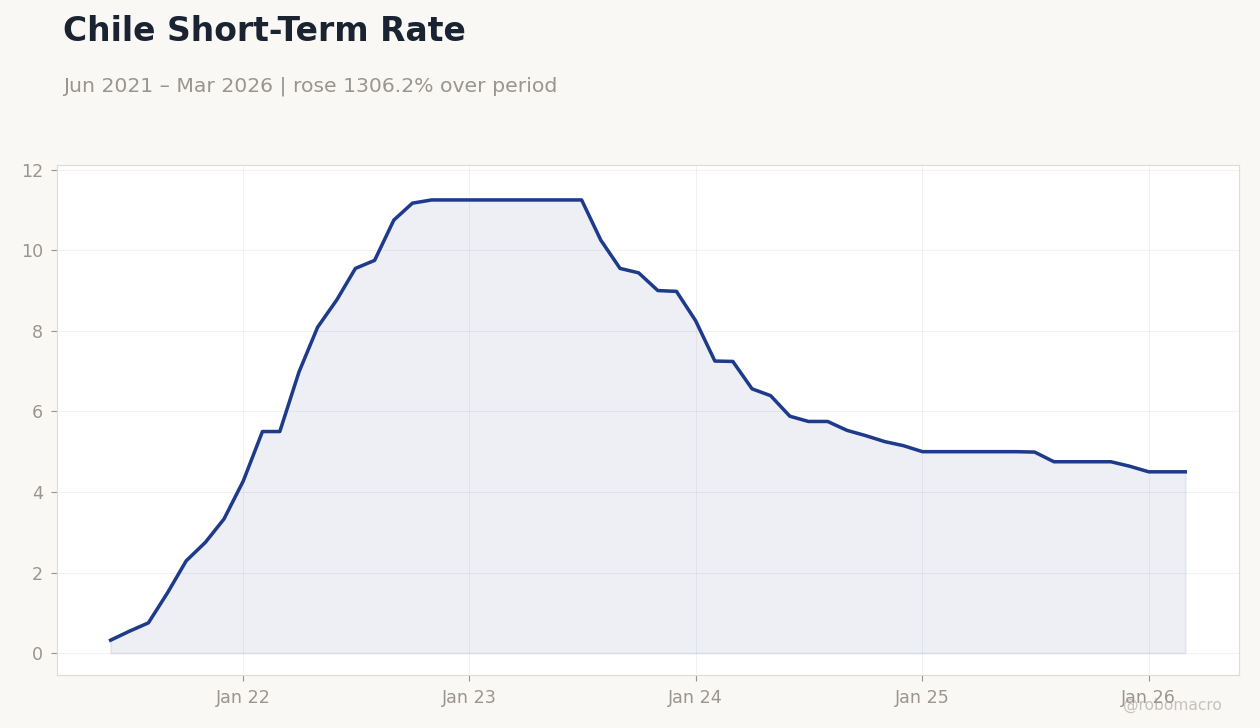

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Short-Term Rate | Type: macro_line | Chile Policy Rate %: 4.5 (2026-03-01) | Range: 0.32–11.25 | Trend(5pt): 0.32,9.75,9.44,5.15,4.5

Chile Short-Term Rate | Type: macro_line | Chile Policy Rate %: 4.5 (2026-03-01) | Range: 0.32–11.25 | Trend(5pt): 0.32,9.75,9.44,5.15,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI Peru jumped 4.13% and MSCI Chile rose 2.93% while MSCI Colombia stayed flat at 9.02.

- USD/PEN climbed 2.05% to 3.41 and USD/COP gained 0.97% to 3,667.69; USD/CLP eased 0.37% to 893.35.

- Brent crude plunged 5.29% to 94.31, pressuring Colombia’s fiscal outlook while copper held near 6.36.

Yesterday's Recap

Andean equity markets showed clear divergence on May 26. Peru’s MSCI index surged 4.13% to 86.01, supported by mining names. Chile’s MSCI index advanced 2.93% to 41.47 on steady copper prices at 6.36.

Colombia’s MSCI index remained unchanged at 9.02. Currencies moved sharply: the PEN weakened 2.05% against the dollar while the COP depreciated 0.97%. The CLP strengthened 0.37%.

Brent’s 5.29% drop to 94.31 weighed on Colombian oil-linked revenues with no major data releases reported across the three countries. Ecopetrol launched an OPA to acquire control of Brava at R$23 per share, which would give it 51% ownership if successful. An earthquake in Chile was felt in parts of São Paulo.

The Day Ahead

The Andean calendar remains empty through May 28. Markets will track global commodity flows and any follow-through from yesterday’s equity gains. Copper stability near 6.36 continues to support Chile and Peru fiscal projections.

Colombia faces pressure from lower Brent at 94.31 on Ecopetrol royalty estimates. Investors will monitor USD/COP at 3,667.69 and USD/PEN at 3.41 for signs of further depreciation. Central bank communications remain the next potential catalyst.

Other Economic Notes

Copper prices near 6.36 underpin external balances in Chile and Peru. Gold at 4,478.70 offers limited fiscal upside for Peru and Colombia despite recent strength. Lithium market softness persists in Chile with no change to SQM or Albemarle guidance.

Regional equities remain sensitive to global risk sentiment given high commodity dependence. Fiscal revenues in Chile and Peru stay closely tied to mining output and prices. Chile’s short-term rate held at 4.50%.

Global Macro News

Brent’s sharp 5.29% decline to 94.31 raises Colombia’s external and fiscal risks. Copper holding at 6.36 limits downside for Chile and Peru trade surpluses. Energy price shocks from Gulf tensions are feeding global inflation concerns that could delay rate cuts elsewhere.

<i>↓ p.2</i>