Andeans Macro Daily(Beta Mode)

MSCI Chile Climbs as Copper Holds Steady

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 40.70 | +1.95% |

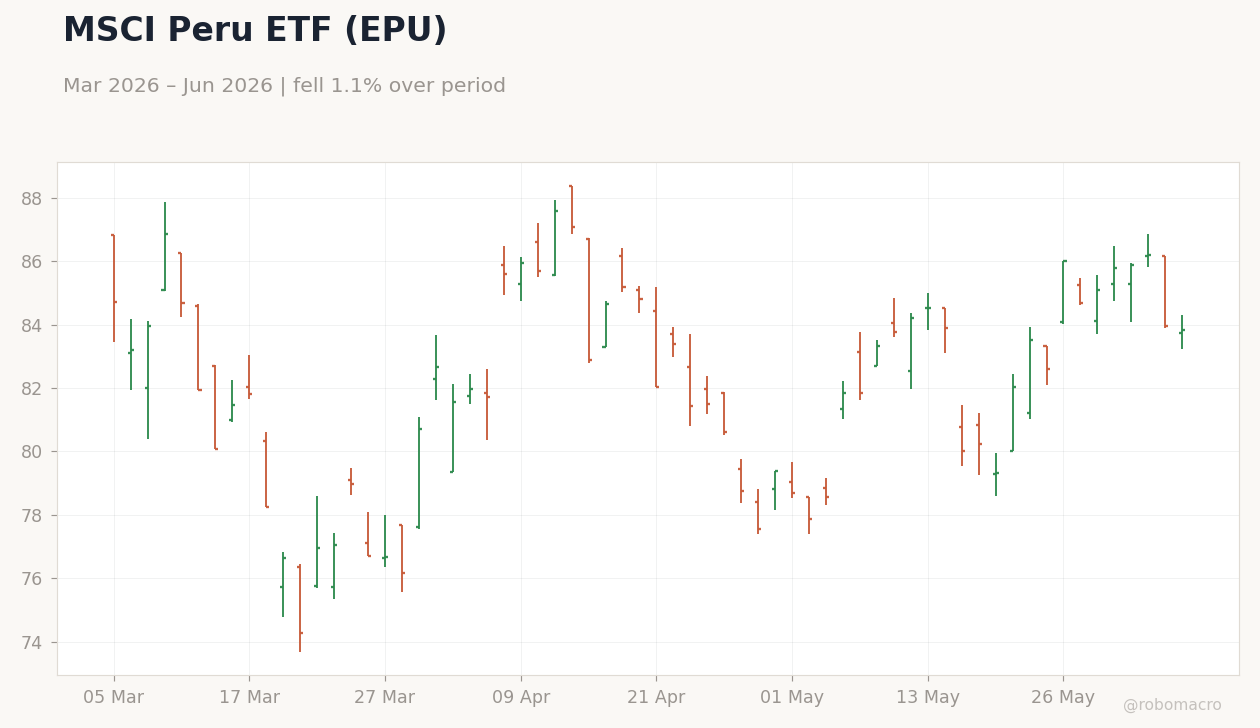

| MSCI Peru | 84.29 | +0.39% |

| USD/COP | 3,558.76 | -0.46% |

| USD/CLP | 894.81 | -0.02% |

| USD/PEN | 3.41 | +0.13% |

| Copper | 6.44 | -1.14% |

| Gold | 4,489.50 | +0.31% |

| Brent Crude | 94.96 | -0.07% |

| Bitcoin | 62,411.20 | -2.18% |

| Colombia 10Y Govt Yield | - | - |

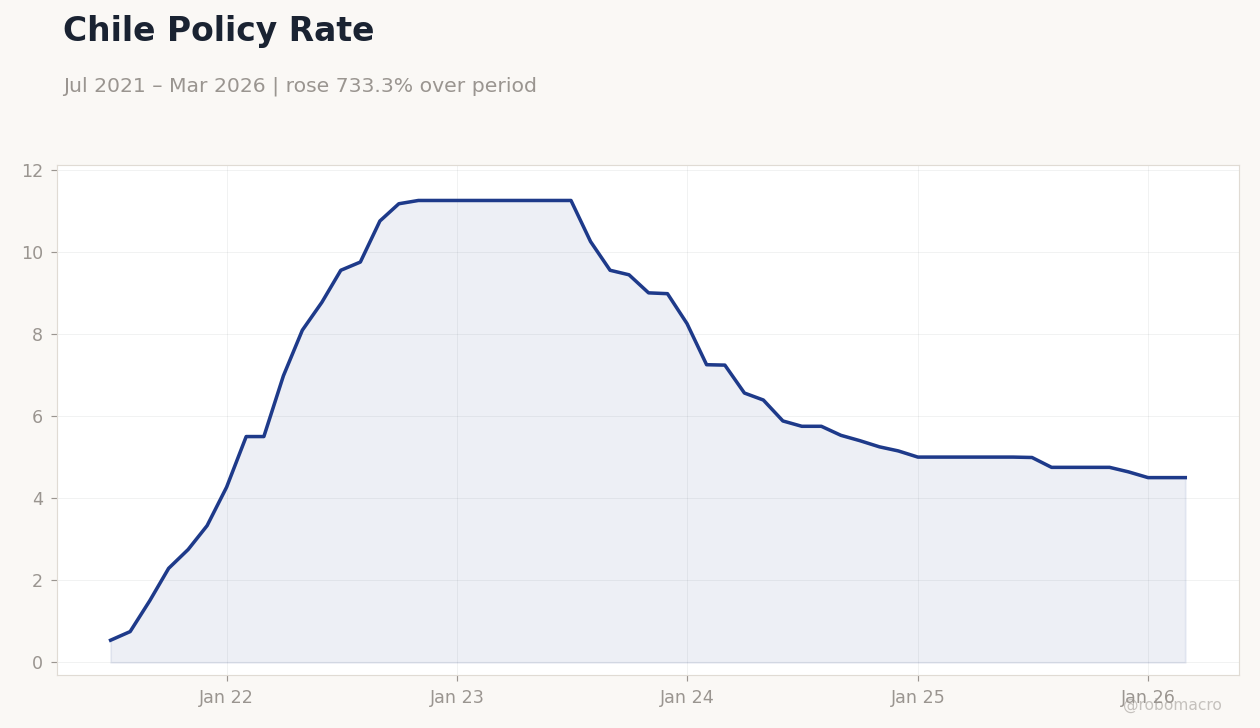

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Policy Rate | Type: macro_line | %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Chile Policy Rate | Type: macro_line | %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI Chile rose 1.95% while Colombia and Peru indices posted minimal gains amid thin data flow.

- COP strengthened 0.46% to 3,558.76 as Brent held near $95; CLP and PEN saw negligible moves.

- Chile short-term rate stayed at 4.50% with no policy shift signaled by BCCh.

Yesterday's Recap

Andean markets recorded modest equity gains on June 4 with limited macro releases across the region. MSCI Chile advanced 1.95% to 40.70, supported by copper near $6.44 per pound despite a 1.14% daily decline. MSCI Peru edged up 0.39% to 84.29 while MSCI Colombia remained flat at 9.02.

USD/COP fell 0.46% to 3,558.76, reflecting steady Brent crude at $94.96. USD/CLP held virtually unchanged at 894.81 and USD/PEN rose 0.13% to 3.41. Gold at $4,489.50 offered minor support to Peru’s external accounts.

No inflation, GDP or fiscal prints were scheduled in Colombia, Chile or Peru.

The Day Ahead

The calendar remains empty for June 5–6 with zero high-impact releases listed for the three Andean economies. Traders will monitor copper and Brent price action for signals on Chile’s fiscal revenue and Peru’s trade balance. Colombia’s 10-year TES curve may see limited secondary-market flow absent new supply.

BCCh’s next policy decision is not expected before late June. Regional FX desks anticipate range-bound trading in COP, CLP and PEN given the data vacuum.

Other Economic Notes

Copper price stability near multi-year highs continues to underpin Chile’s royalty receipts and Peru’s current-account surplus. Colombia’s fiscal position remains sensitive to Brent fluctuations around $95, with each sustained move altering revenue projections. Lithium development in Chile shows no immediate FX or inflation impact.

Bitcoin’s 2.18% drop to $62,411 carries negligible direct effect on Andean capital flows. Broader commodity resilience supports external balances in Chile and Peru more than in oil-reliant Colombia.

Global Macro News

Global risk appetite stayed constructive, lifting emerging-market equities and supporting selective Andean currency strength. Brent crude near $95 limited downside pressure on Colombia’s terms of trade. Copper’s resilience despite a modest daily dip reinforced positive growth revisions for Chile and Peru.

<i>↓ p.2</i>