Andeans Macro Daily(Beta Mode)

Chile Stocks Rise as Peso Strengthens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 39.49 | +0.87% |

| MSCI Peru | 81.69 | -0.98% |

| USD/COP | 3,547.27 | -0.77% |

| USD/CLP | 916.46 | +0.00% |

| USD/PEN | 3.41 | +0.49% |

| Copper | 6.23 | -0.31% |

| Gold | 4,112.20 | +0.10% |

| Brent Crude | 92.07 | -1.11% |

| Bitcoin | 63,044.65 | +2.60% |

| Colombia 10Y Govt Yield | - | - |

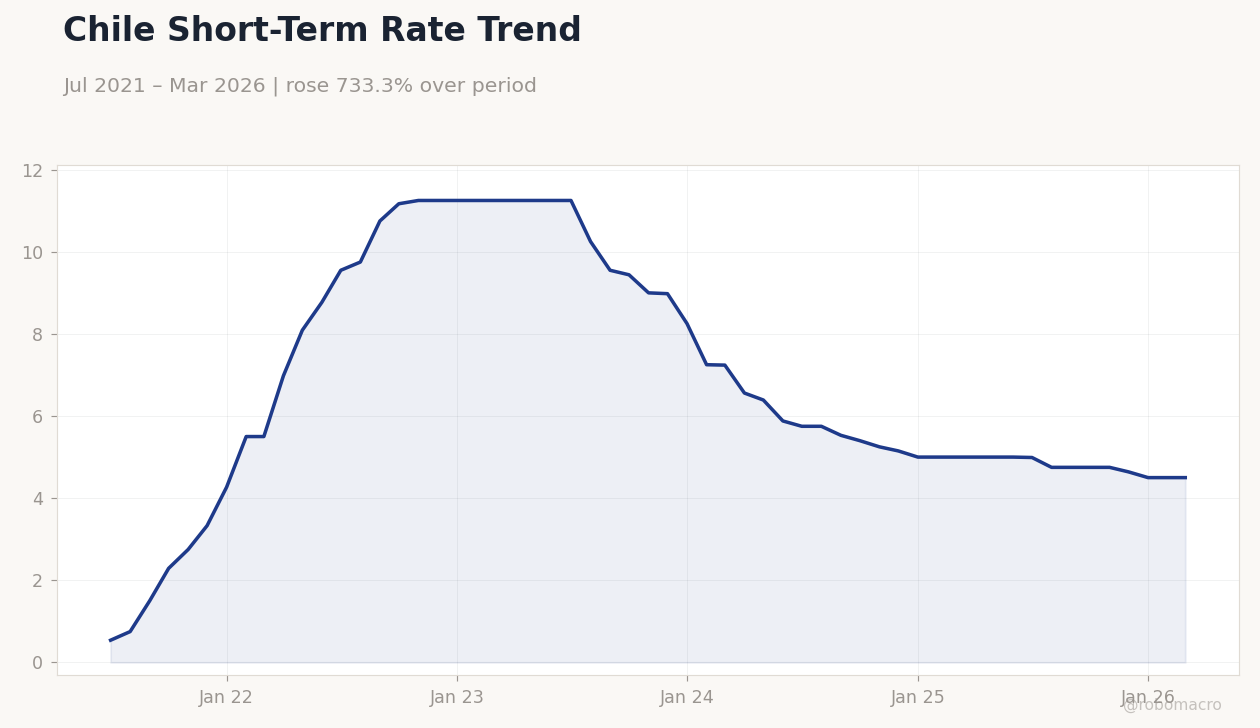

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Short-Term Rate Trend | Type: macro_line | %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Chile Short-Term Rate Trend | Type: macro_line | %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI Chile rises 0.87% while Peru slips 0.98% amid flat copper prices.

- Colombian peso strengthens to 3,547.27 per USD on reduced oil pressure.

- BCCh holds short-term rate at 4.50% with no immediate policy shift signaled.

Yesterday's Recap

Andean equity markets showed mixed performance on June 10. MSCI Chile gained 0.87% to 39.49, supported by mining sector exposure despite copper edging down 0.31% to 6.23. MSCI Peru declined 0.98% to 81.69 as local currency weakness weighed on sentiment.

USD/COP fell 0.77% to 3,547.27, reflecting peso strength, while USD/PEN rose 0.49% to 3.41. Brent crude declined 1.11% to 92.07, limiting upside for Colombian fiscal revenues. Gold held steady near 4,112.20, offering minor support to Peru’s external accounts.

Chile’s short-term rate remained unchanged at 4.50%. MSCI Colombia closed flat at 9.02. USD/CLP was unchanged at 916.46.

Bitcoin rose 2.60% to 63,044.65.

The Day Ahead

No major data releases are scheduled across Colombia, Chile, or Peru for June 11-12. Markets will likely focus on external drivers including copper and oil price movements. Any follow-through in Chinese demand indicators could influence CLP and PEN.

BanRep’s next policy meeting remains weeks away, keeping attention on incoming inflation prints. Regional FX volatility may stay contained absent fresh commodity shocks.

Other Economic Notes

Copper remains central to Chile and Peru fiscal balances, with even modest price dips trimming projected royalty inflows. Colombia’s oil sensitivity continues to pressure its current-account gap when Brent eases. Lithium export volumes from Chile posted modest gains, adding a secondary revenue stream.

Broader commodity stability supports external surpluses in the copper producers while leaving Colombia more exposed to energy price swings. A Chilean copper project changed hands in a $55M deal, underscoring ongoing investor interest in the sector.

Global Macro News

U.S. inflation concerns resurfaced after gasoline prices surged, raising the risk of delayed Fed easing. Bank of Canada held its policy rate at 2.25% amid slowing domestic growth.

Japan’s prime minister signaled intent to defend the yen through economic strengthening rather than direct intervention. <i>↓ p.2</i>