Andeans Macro Daily(Beta Mode)

Copper Surge Powers Chile, Peru Gains

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 40.96 | +4.60% |

| MSCI Peru | 85.74 | +5.60% |

| USD/COP | 3,490.01 | -1.93% |

| USD/CLP | 904.40 | -1.18% |

| USD/PEN | 3.40 | +1.99% |

| Copper | 6.39 | +2.09% |

| Gold | 4,227.50 | +3.35% |

| Brent Crude | 87.23 | -3.49% |

| Bitcoin | 63,721.62 | +0.25% |

| Colombia 10Y Govt Yield | - | - |

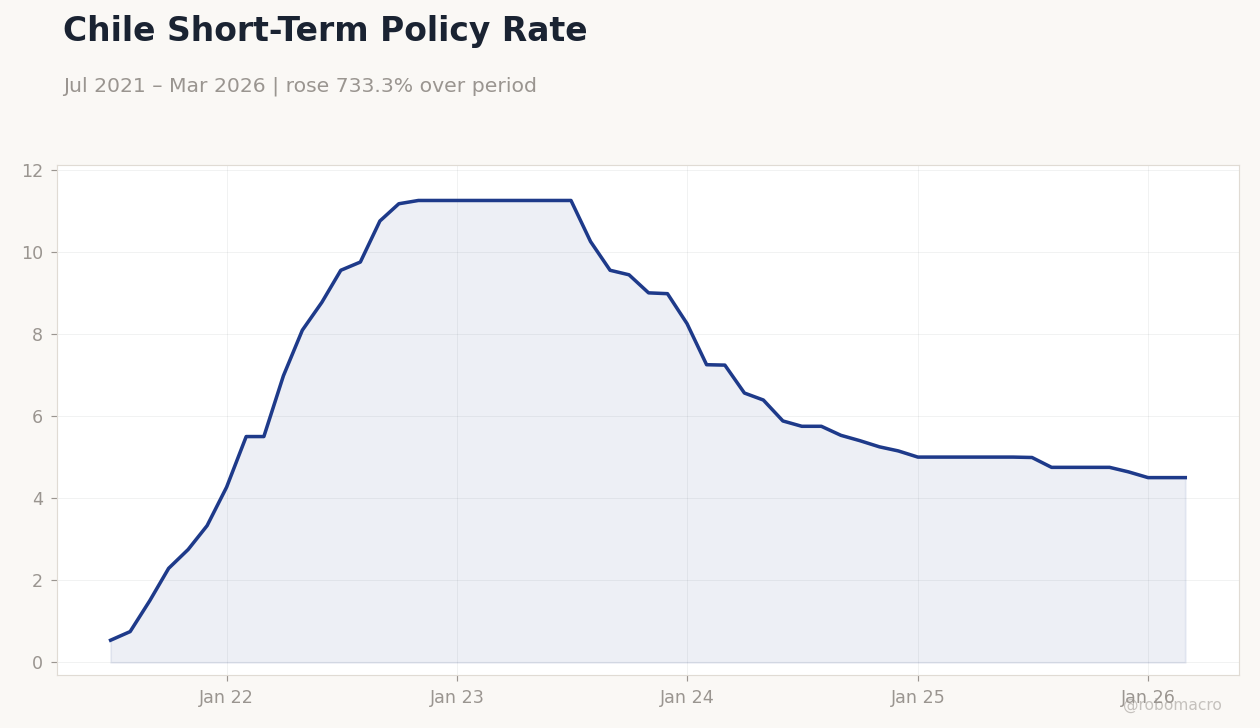

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Short-Term Policy Rate | Type: macro_line | Policy Rate %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Chile Short-Term Policy Rate | Type: macro_line | Policy Rate %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI Chile jumps 4.60% and MSCI Peru rises 5.60% as copper climbs 2.09% to 6.39

- USD/COP falls 1.93% while USD/PEN rises 1.99% on divergent commodity exposures

- Brent crude drops 3.49% to 87.23, adding fiscal pressure on Colombia

Yesterday's Recap

Andean equity markets posted sharp gains on June 11 driven by commodity strength. MSCI Chile advanced 4.60% to 40.96 while MSCI Peru climbed 5.60% to 85.74, tracking copper’s 2.09% advance to 6.39 amid supply concerns and stronger Chinese demand signals. Gold’s 3.35% rise to 4,227.50 further supported Peru’s external accounts.

The Colombian peso strengthened 1.93% to 3,490.01 against the dollar, whereas the Chilean peso gained 1.18% to 904.40; the Peruvian sol weakened 1.99% to 3.40. No macroeconomic data releases occurred across the three countries. Chile’s short-term rate held steady at 4.50%.

Brent’s 3.49% decline to 87.23 weighed on Colombia’s fiscal revenue outlook via lower Ecopetrol dividends.

The Day Ahead

The Andean calendar remains empty of scheduled releases through June 13. Markets will instead track global commodity prices and external risk sentiment. Copper and gold moves will continue to dominate Chile and Peru equity and currency performance.

Colombia’s fiscal balance remains sensitive to Brent crude fluctuations. Investors will monitor any updates on Peru’s ongoing electoral vote count for potential policy signals. Regional central banks are not expected to announce decisions in the immediate term.

Other Economic Notes

Chile’s fiscal position benefits directly from elevated copper prices through higher CODELCO royalties, narrowing the projected deficit. Peru’s copper export volumes grew modestly despite lower ore grades at major mines. Colombia faces widening deficit risks from softer oil receipts, keeping USD/COP structurally supported.

Lithium production guidance from Chilean operators stayed unchanged, limiting near-term price impact. Broader mining equity strength reflects global supply tightness rather than domestic demand shifts.

Global Macro News

The UK economy contracted 0.1% in April as Iran-related disruptions weighed on activity. The ECB maintained its deposit rate at 2.00% despite softer Eurozone growth, with unemployment at 6.70%. Copper prices surged after signals of a potential US-Iran deal, boosting mining equities worldwide.

Inflation pressures continued to erode real incomes across major economies. <i>↓ p.2</i>