Andeans Macro Daily(Beta Mode)

Chile, Peru Stocks Rise on Copper, Gold Gains

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 41.50 | +1.32% |

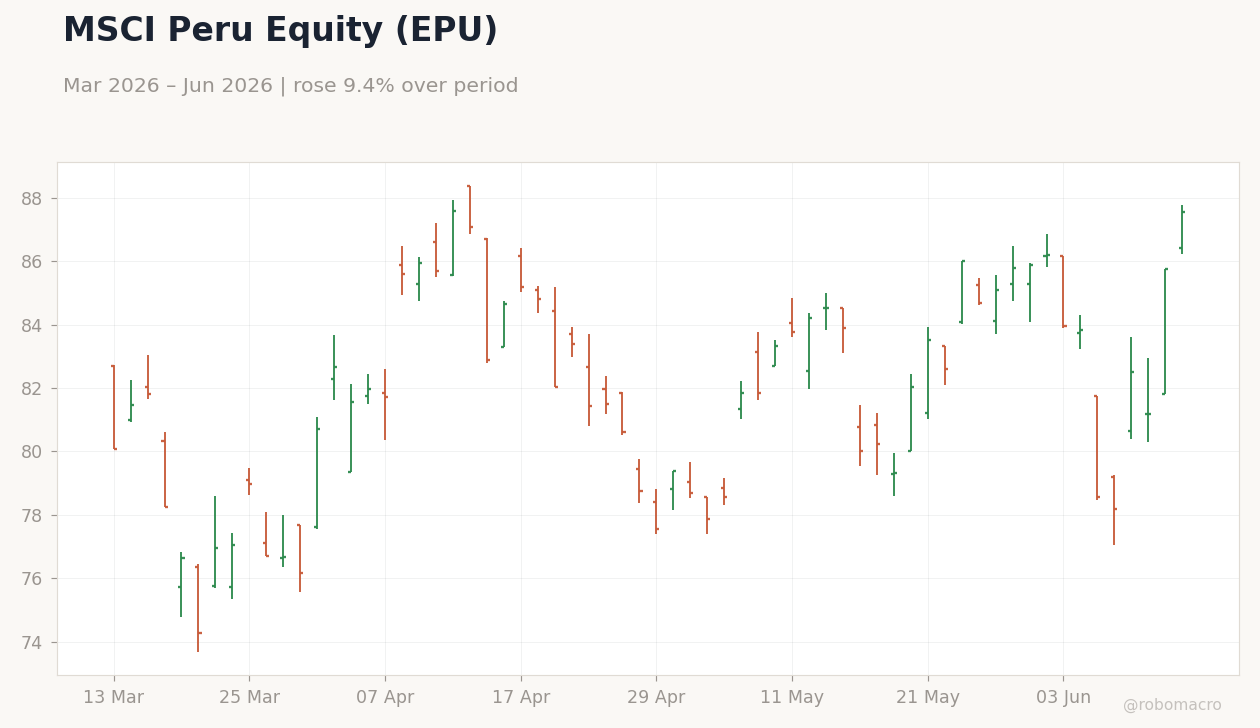

| MSCI Peru | 87.56 | +2.12% |

| USD/COP | 3,454.45 | -1.31% |

| USD/CLP | 898.70 | -0.81% |

| USD/PEN | 3.40 | +2.08% |

| Copper | 6.49 | +0.98% |

| Gold | 4,359.30 | +3.42% |

| Brent Crude | 82.98 | -4.98% |

| Bitcoin | 66,183.77 | +0.72% |

| Colombia 10Y Govt Yield | - | - |

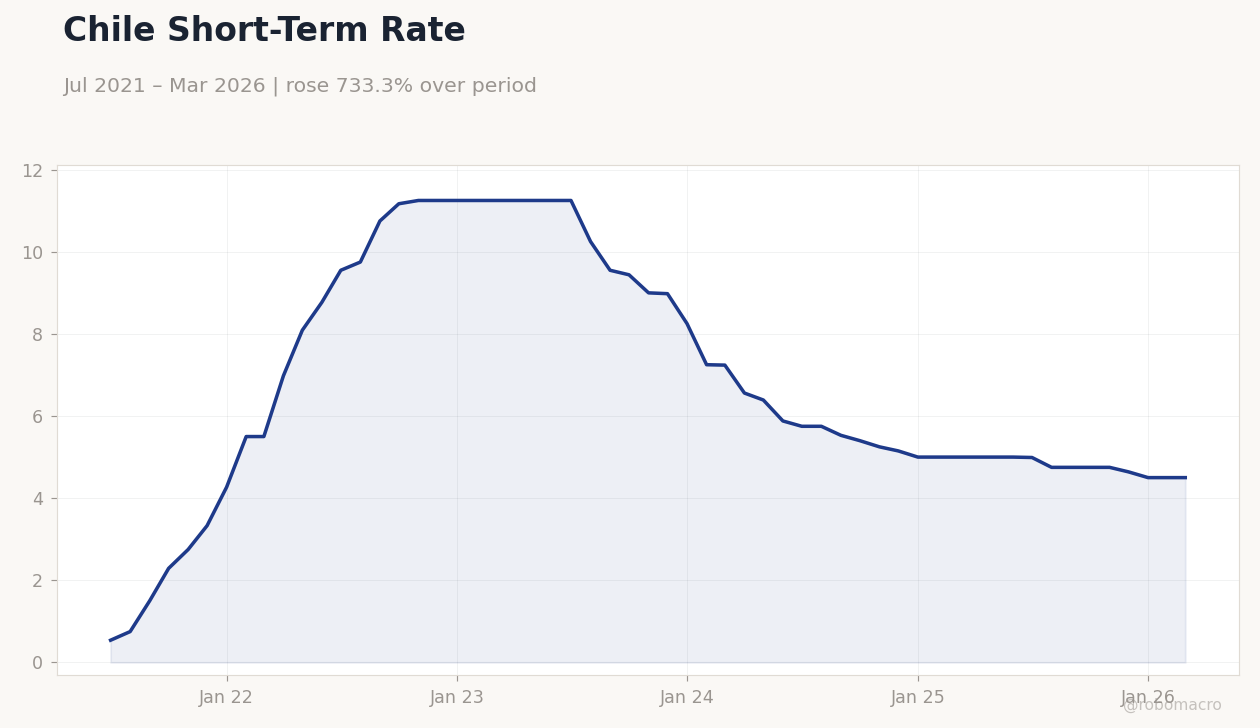

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Short-Term Rate | Type: macro_line | Percent: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Chile Short-Term Rate | Type: macro_line | Percent: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI Chile rose 1.32% and MSCI Peru gained 2.12% on stronger copper and gold prices.

- USD/COP fell 1.31% and USD/CLP declined 0.81% while USD/PEN rose 2.08%.

- Brent crude dropped 4.98% pressuring Colombia’s external accounts.

Yesterday's Recap

Chile and Peru equity markets led Andean gains as copper advanced 0.98% to 6.49 and gold jumped 3.42% to 4,359.30. MSCI Chile closed at 41.50 while MSCI Peru reached 87.56, reflecting direct exposure to mining exports. USD/CLP eased to 898.70 on the commodity strength, supporting Chile’s fiscal receipts.

In Colombia, MSCI Colombia held steady at 9.02 as Brent’s sharp decline offset any oil-related support for the peso, which strengthened to 3,454.45. Peru saw secondary benefits from copper but faced headwinds from the PEN’s 2.08% weakening to 3.40. Chile’s short-term rate remained at 4.50% with no policy shift.

No major data releases occurred across the three countries on June 14.

The Day Ahead

The calendar shows no scheduled releases for June 15 across Colombia, Chile or Peru. Markets will monitor ongoing commodity trends, particularly copper and gold, for further equity and FX direction. Chile’s mining production figures and lithium export volumes are due mid-week and could influence BCCh sentiment.

Peru’s Q1 GDP print is expected later in the week with consensus around modest expansion. Colombia retail sales data follow shortly after. No central bank meetings or sovereign debt auctions are planned in the next 48 hours.

Other Economic Notes

Copper’s sustained advance above 6.40 bolsters Chile’s structural fiscal balance and royalty collections, adding potential GDP support near 0.8% if prices hold. Peru benefits indirectly through mining volumes at operations such as Escondida and Antamina. Colombia faces pressure on Ecopetrol cash flows and the current account from Brent’s decline below 83.

Lithium developments in Chile remain in focus ahead of production updates from SQM and Albemarle. Regional equities show divergence, with Chile and Peru outperforming Colombia amid commodity differentiation.

Global Macro News

Stronger Chinese industrial data lifted copper and supported Chilean and Peruvian assets. Gold’s surge to 4,359.30 reflected safe-haven demand amid geopolitical uncertainty. Brent’s 4.98% drop weighed on Colombia’s oil-linked revenues and widened external imbalances.

<i>↓ p.2</i>