Andeans Macro Daily(Beta Mode)

Chile, Peru Stocks Rise as Copper Climbs

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 41.50 | +1.32% |

| MSCI Peru | 87.56 | +2.12% |

| USD/COP | 3,428.50 | -1.78% |

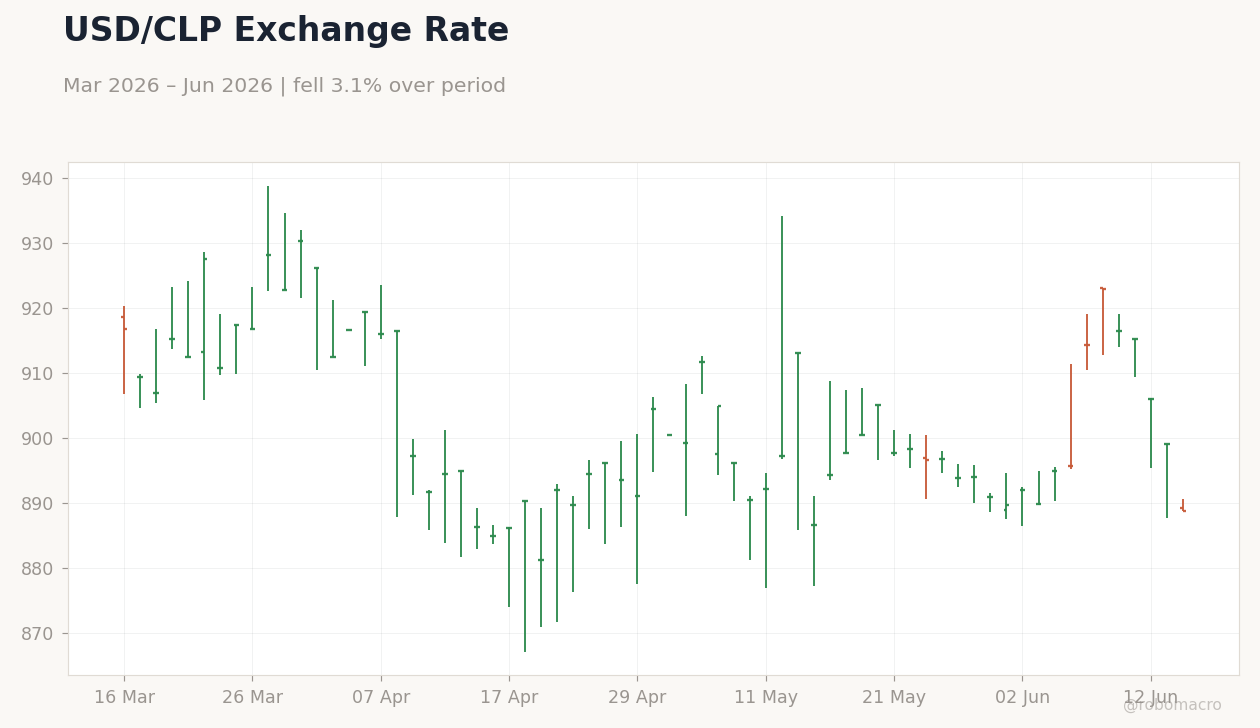

| USD/CLP | 888.73 | -1.15% |

| USD/PEN | 3.41 | +2.24% |

| Copper | 6.49 | +0.15% |

| Gold | 4,362.20 | +0.79% |

| Brent Crude | 81.06 | -2.54% |

| Bitcoin | 66,515.23 | +0.34% |

| Colombia 10Y Govt Yield | - | - |

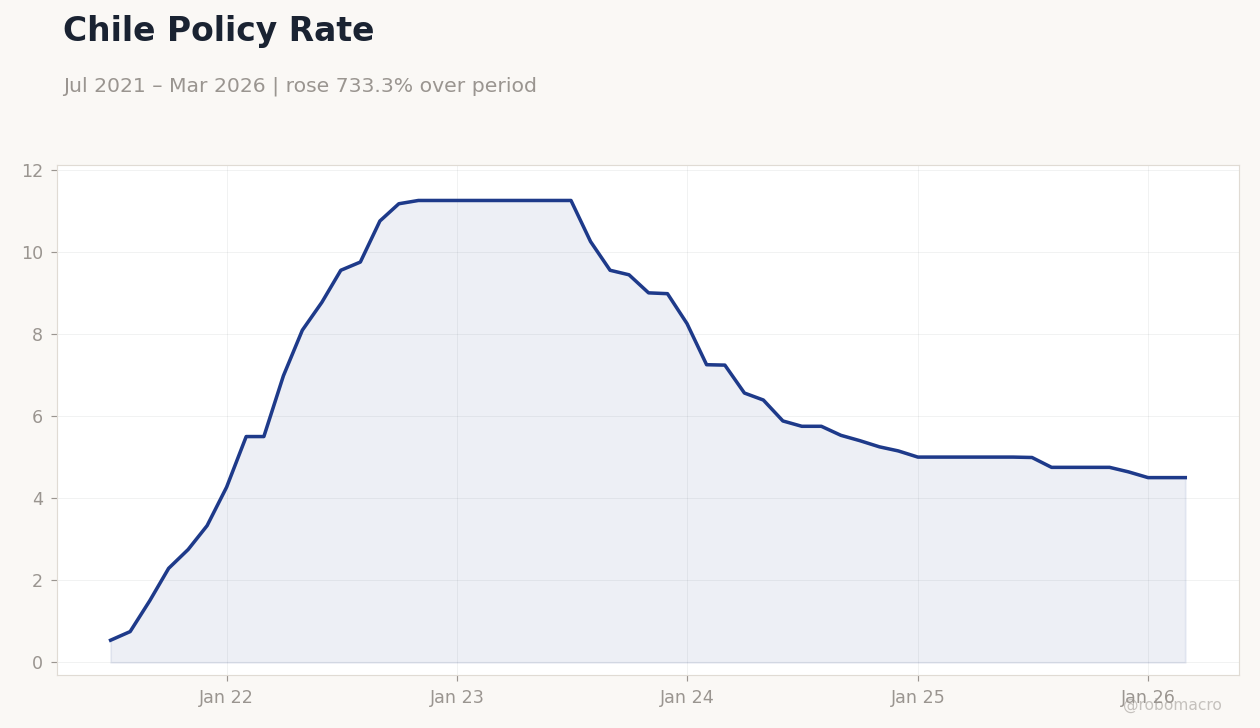

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Policy Rate | Type: macro_line | Rate %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Chile Policy Rate | Type: macro_line | Rate %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI Chile and Peru rose 1.32% and 2.12% respectively while Colombia remained flat amid commodity moves

- CLP and COP strengthened against the USD as copper edged higher and Brent crude declined

- BCCh widely expected to hold its benchmark rate at 4.50% following recent activity data

Yesterday's Recap

MSCI Chile climbed 1.32% to 41.50 and MSCI Peru gained 2.12% to 87.56 on modest copper strength, while MSCI Colombia held steady at 9.02. USD/CLP fell 1.15% to 888.73 and USD/COP declined 1.78% to 3,428.50, reflecting improved sentiment toward Chilean and Colombian assets. USD/PEN rose 2.24% to 3.41 as the sol underperformed.

Copper advanced 0.15% to 6.49, supporting Chile and Peru mining revenues, whereas Brent crude dropped 2.54% to 81.06, trimming Colombia’s near-term fiscal oil receipts. Gold rose 0.79% to 4,362.20, offering limited support to Peru’s external accounts. Chile’s short-term rate remained at 4.50% with no policy shift signaled in market pricing.

No major economic releases occurred across the region.

The Day Ahead

Markets face a thin economic calendar across the Andean region with no major releases scheduled. Attention centers on any follow-up commentary from BCCh officials after the widely anticipated hold decision. Traders will monitor copper price action for further signals on Chile’s fiscal and Peru’s trade balances.

Broader global developments, including G7 discussions, may influence regional FX flows. Peruvian political developments around the incoming administration could add volatility to PEN trading.

Other Economic Notes

Andean economies remain tightly linked to commodity cycles, with Chile and Peru highly sensitive to copper price swings that directly affect fiscal balances and current-account positions. Colombia’s oil exposure creates divergence when energy prices soften. Regional equity performance continues to track mining output trends and external demand indicators.

Stable policy rates in Chile underscore a cautious approach amid mixed growth signals. The ECB deposit rate stands at 2.00%.

Global Macro News

The G7 summit is set to address global growth risks with participation from India, Brazil and additional partners, carrying implications for trade and capital flows into Latin America. Australia’s Reserve Bank held its cash rate at 4.35% citing cooling economic momentum. ECB President Lagarde noted that energy-price increases are transmitting through the euro-area economy.

<i>↓ p.2</i>