Andeans Macro Daily(Beta Mode)

BCCh Holds at 4.5% as Copper Lifts CLP

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 41.56 | +0.10% |

| MSCI Peru | 88.11 | +0.66% |

| USD/COP | 3,418.00 | -2.05% |

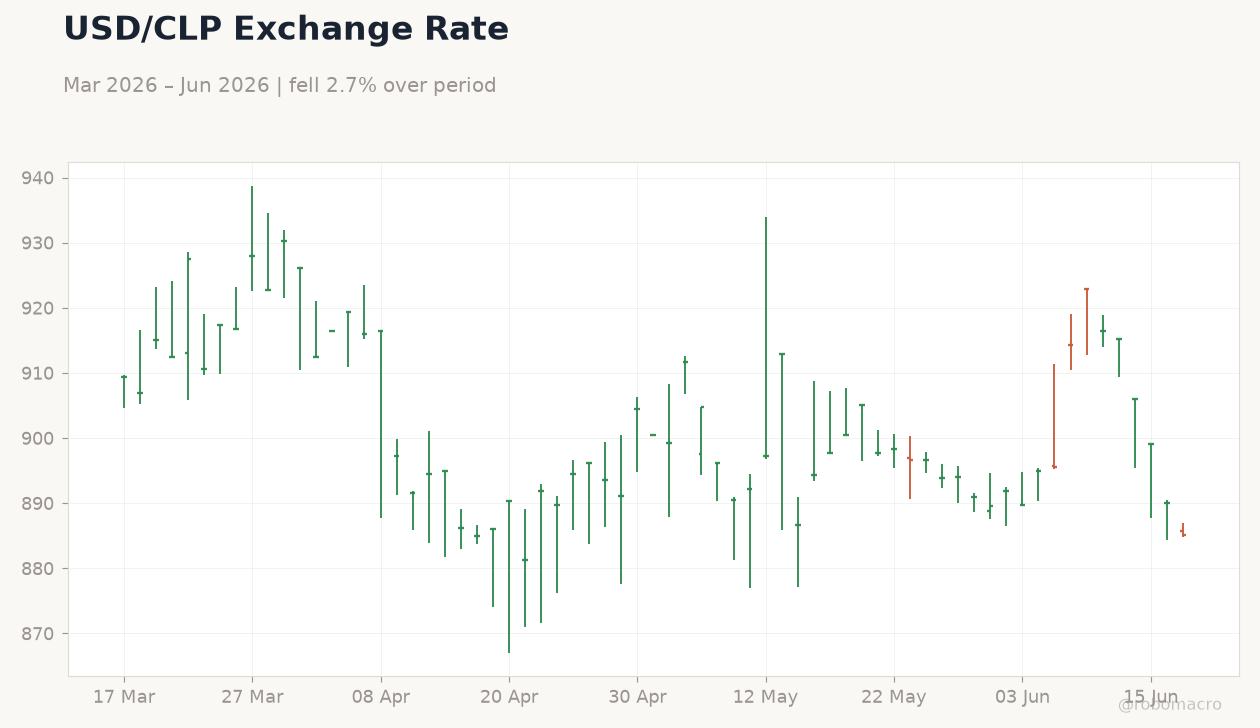

| USD/CLP | 885.12 | -0.54% |

| USD/PEN | 3.41 | +2.38% |

| Copper | 6.51 | +0.39% |

| Gold | 4,343.00 | +0.28% |

| Brent Crude | 79.50 | +0.68% |

| Bitcoin | 64,687.99 | -1.39% |

| Colombia 10Y Govt Yield | - | - |

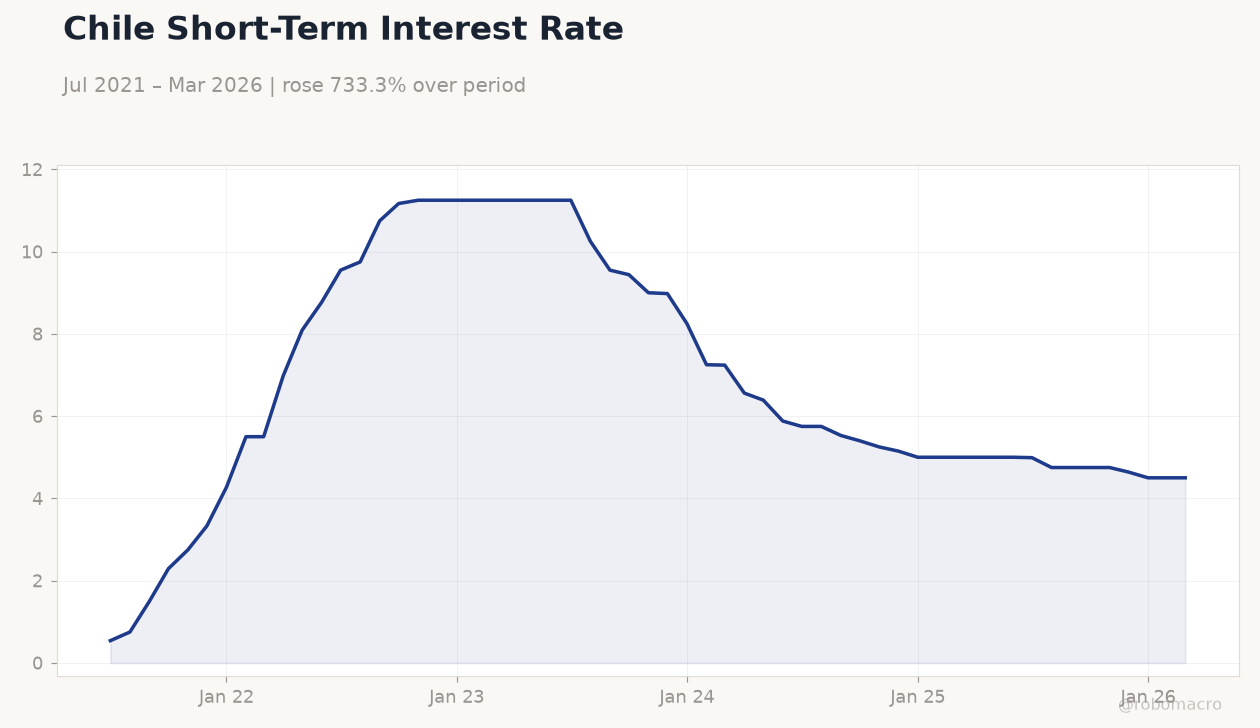

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Short-Term Interest Rate | Type: macro_line | Rate %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Chile Short-Term Interest Rate | Type: macro_line | Rate %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Chile’s central bank held its policy rate at 4.5% with risks now viewed as balanced.

- Andean equity markets posted modest gains led by Peru’s MSCI index on commodity strength.

- COP strengthened sharply while PEN depreciated against a firm USD.

Yesterday's Recap

Chile’s central bank kept its benchmark rate unchanged at 4.5% for the fourth consecutive meeting, noting more balanced inflation risks after May CPI printed 0.3% m/m. MSCI Peru rose 0.66% to 88.11 while MSCI Chile added 0.10% to 41.56, supported by copper’s 0.39% gain to 6.51. MSCI Colombia closed flat at 9.02.

USD/COP fell 2.05% to 3,418 while USD/CLP eased 0.54% to 885.12; USD/PEN rose 2.38% to 3.41. Brent crude advanced 0.68% to 79.50, offering limited immediate relief to Colombia’s fiscal accounts given Ecopetrol hedging. Gold’s 0.28% increase to 4,343 provided marginal support to Peru’s external accounts.

The Day Ahead

Markets anticipate a quiet session with no major Andean data releases scheduled. Attention will center on global copper and oil price action given their direct fiscal and FX implications for Chile, Peru and Colombia. Political headlines surrounding Colombia’s upcoming electoral contest may continue to influence COP volatility.

Participants will also monitor any follow-up comments from BCCh officials after yesterday’s hold decision.

Other Economic Notes

Copper prices near multi-year highs continue to widen Chile’s and Peru’s current-account surpluses and bolster fiscal revenues through royalties and taxes. Colombia’s external position remains more exposed to Brent swings, though hedging by the state oil company caps near-term revenue volatility. Regional equity flows stay selective, favoring commodity-exposed names in Chile and Peru over Colombian assets amid lingering political uncertainty.

Global Macro News

The Eurozone economy showed resilience with unemployment holding at 6.7%, supporting external demand for Andean metals. ECB deposit rate at 2.25% keeps global monetary conditions relatively accommodative, aiding carry trades into CLP and COP. Copper supply disruptions at major mines outside the region added upward pressure on prices, benefiting Chile and Peru’s terms of trade.

Brent’s modest advance reflected steady global demand and limited OPEC+ supply response. Broader risk sentiment remained constructive for emerging-market assets despite mixed equity closes in Asia.