Andeans Macro Daily(Beta Mode)

Espriella's Win Steers Colombia Toward Markets

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 40.99 | -0.05% |

| MSCI Peru | 88.75 | -0.15% |

| USD/COP | 3,436.08 | -0.24% |

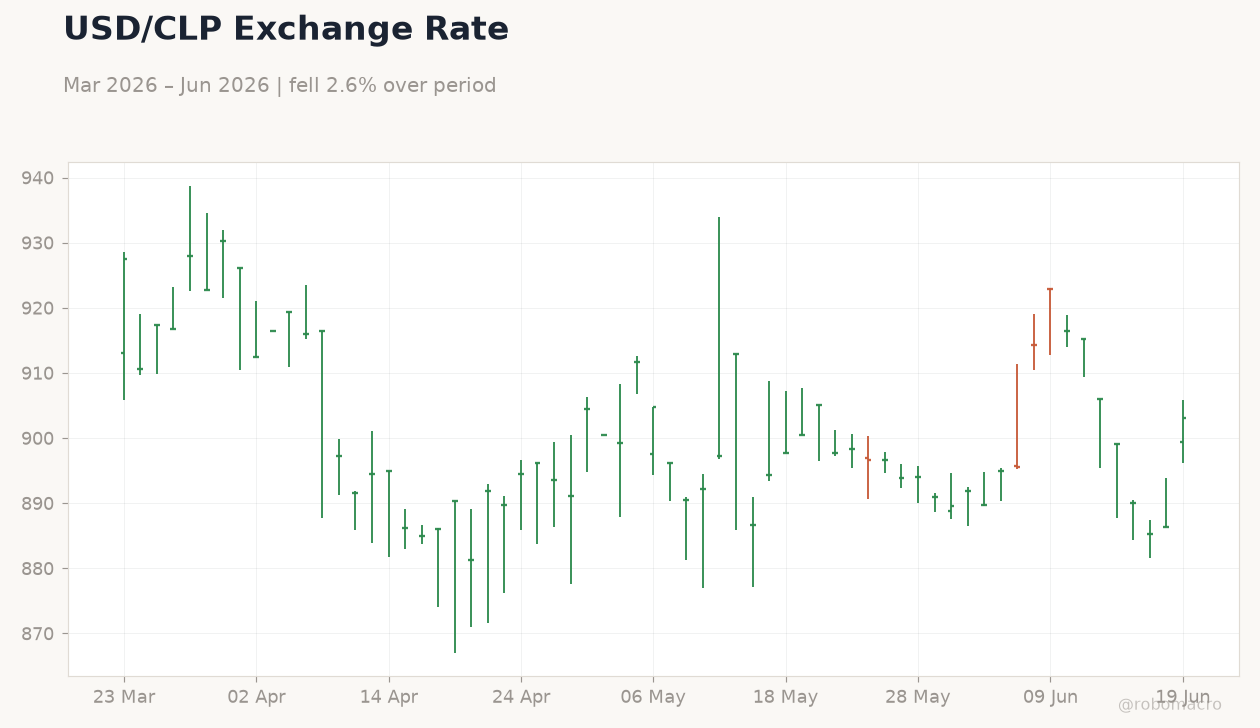

| USD/CLP | 903.15 | +1.90% |

| USD/PEN | 3.38 | +0.02% |

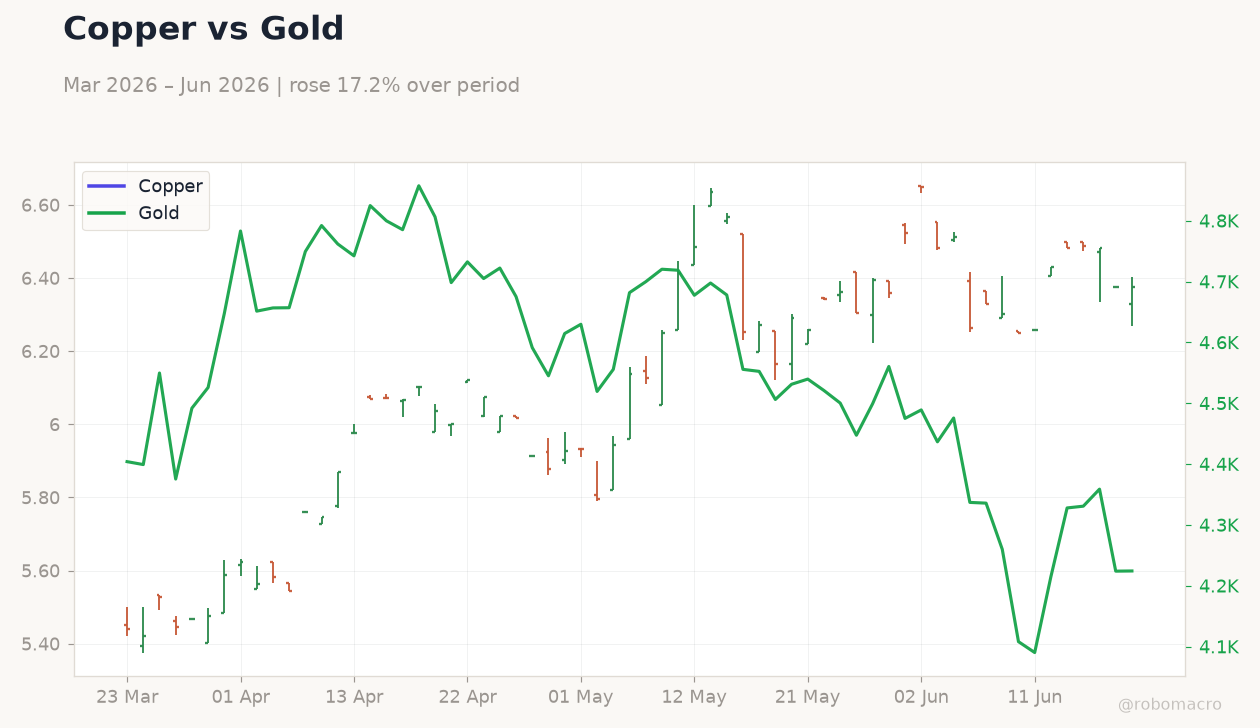

| Copper | 6.39 | +0.16% |

| Gold | 4,229.20 | +0.12% |

| Brent Crude | 78.96 | -1.11% |

| Bitcoin | 64,204.79 | +1.53% |

| Colombia 10Y Govt Yield | - | - |

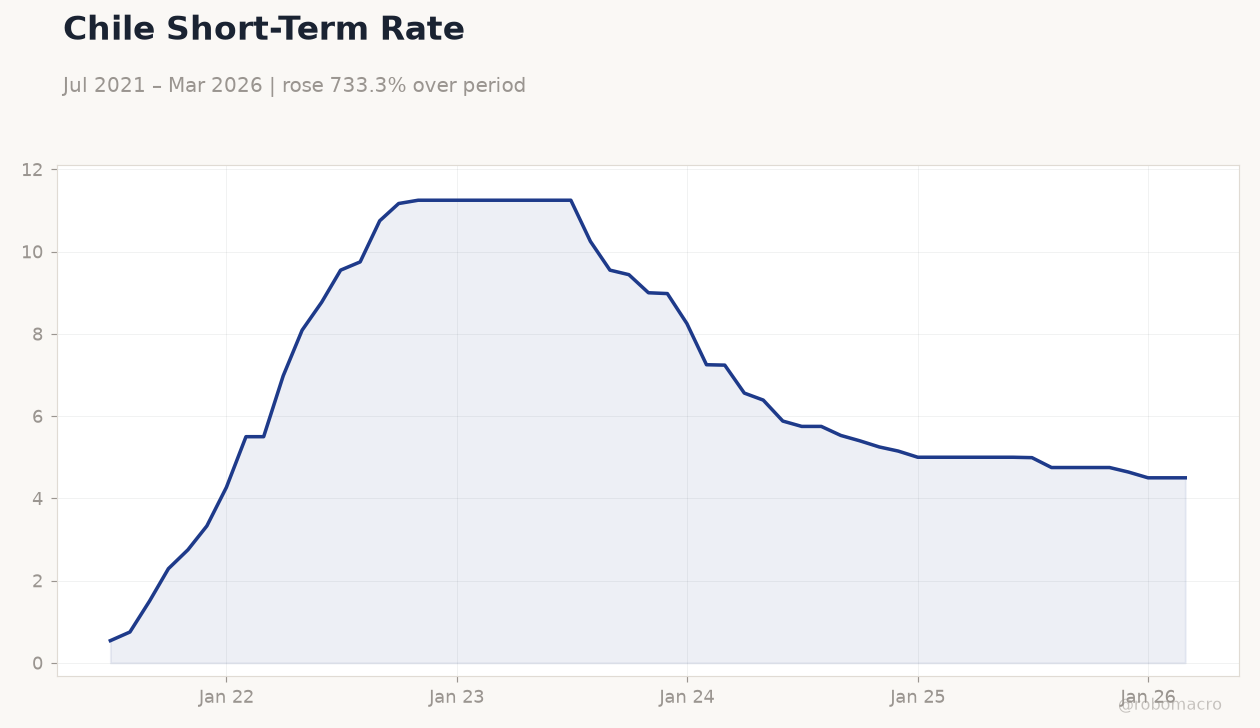

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Short-Term Rate | Type: macro_line | %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Chile Short-Term Rate | Type: macro_line | %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Colombia elects conservative Abelardo de la Espriella president, pointing to pro-market and pro-US policy reversal.

- MSCI Chile slips 0.05% and MSCI Peru falls 0.15% while USD/CLP jumps 1.90% on copper-led moves.

- USD/COP eases 0.24% to 3,436.08 as markets price reduced political risk after the runoff.

Yesterday's Recap

Colombia’s presidential runoff delivered a narrow victory for Trump-endorsed lawyer Abelardo de la Espriella, triggering immediate market repricing of policy direction. MSCI Colombia held flat at 9.02 while the peso strengthened modestly against the dollar. In Chile, MSCI Chile eased 0.05% to 40.99 as USD/CLP surged 1.90% to 903.15 amid a 0.16% copper gain to 6.39.

Peru’s MSCI index declined 0.15% to 88.75 with USD/PEN little changed at 3.38. Brent crude fell 1.11% to 78.96, limiting support for Colombian fiscal accounts, while gold rose 0.12% to 4,229.20. Bitcoin advanced 1.53% to 64,204.79, providing peripheral risk-on sentiment for the region.

The Day Ahead

No major economic releases are scheduled across the Andean bloc for the next session. Markets will monitor post-election positioning in Colombian assets and any early signals from the incoming administration on fiscal and security policy. Chile’s short-term rate remains at 4.50% with no BCCh meeting imminent.

Peru’s stable macro backdrop leaves BCRP on hold. Traders will track copper and oil price action for daily FX guidance in CLP and COP.

Other Economic Notes

Copper’s modest advance supports Chile and Peru external accounts though lithium oversupply continues to weigh on Chilean royalty projections. Colombia’s oil-linked fiscal position stays in surplus territory at current Brent levels near 79. Regional equity indices remain range-bound as investors assess the durability of the Colombian political shift.

Broader commodity stability limits immediate pressure on Andean current accounts.

Global Macro News

The ECB Deposit Rate sits at 2.25%, keeping euro-area financial conditions tighter than Andean peers and supporting carry flows into COP and CLP. Eurozone unemployment at 6.70% signals steady external demand for Chilean and Peruvian copper exports. US dollar strength continues to influence CLP more than COP or PEN given Chile’s higher commodity beta.

Global risk sentiment, reflected in Bitcoin’s gain, provides a mild tailwind for Andean equities. <i>↓ p.2</i>