Andeans Macro Daily(Beta Mode)

Colombia Swings Right With de la Espriella Win

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 40.99 | -0.05% |

| MSCI Peru | 88.75 | -0.15% |

| USD/COP | 3,421.47 | -0.69% |

| USD/CLP | 906.24 | +0.56% |

| USD/PEN | 3.38 | +2.16% |

| Copper | 6.16 | -3.01% |

| Gold | 4,143.80 | -0.91% |

| Brent Crude | 77.94 | +0.05% |

| Bitcoin | 62,354.07 | -2.50% |

| Colombia 10Y Govt Yield | - | - |

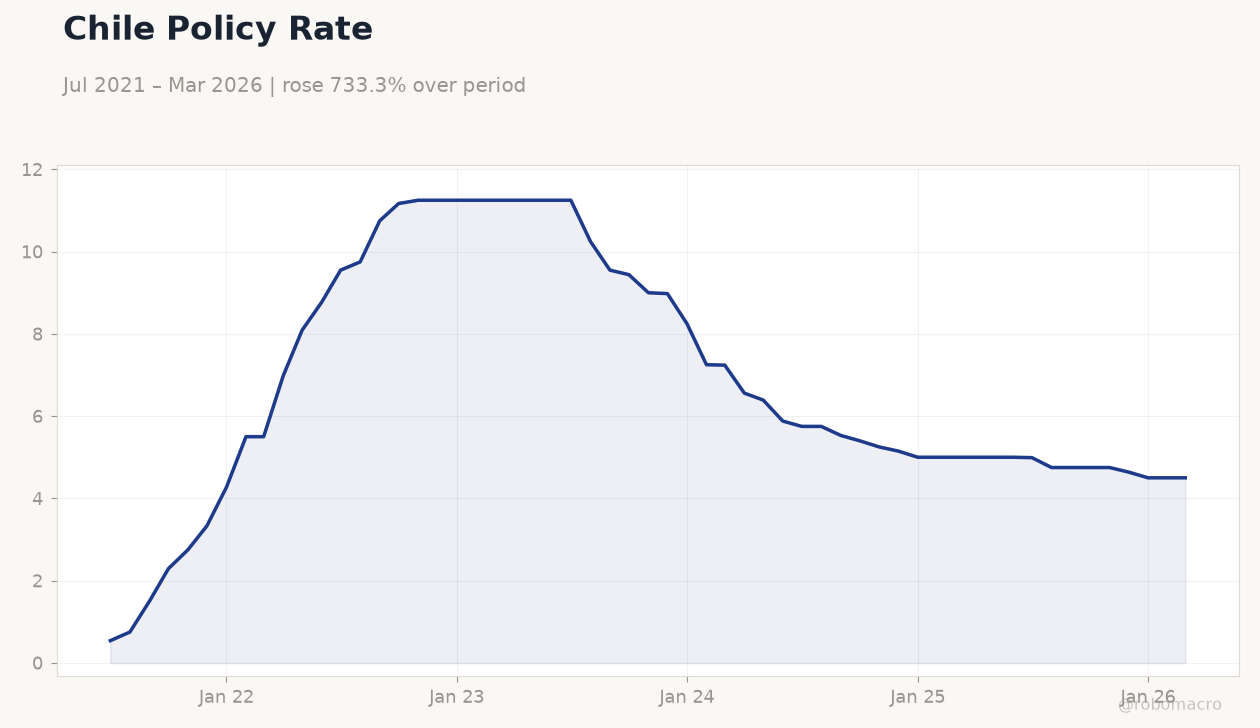

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Policy Rate | Type: macro_line | Percent: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Chile Policy Rate | Type: macro_line | Percent: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Trump-backed Abelardo de la Espriella wins Colombia presidency, signaling pro-market and pro-US pivot.

- Andean equities flat to softer while COP strengthens and PEN weakens sharply on election and commodity moves.

- Copper drops 3.01% to 6.16, pressuring Chile and Peru fiscal and external accounts.

Yesterday's Recap

Colombia’s razor-thin presidential election dominated regional attention as preliminary results showed Abelardo de la Espriella defeating Iván Cepeda and securing a narrow majority. MSCI Colombia closed unchanged at 9.02 while USD/COP fell 0.69% to 3,421.47, reflecting initial market relief over the pro-business outcome. MSCI Chile slipped 0.05% to 40.99 and MSCI Peru declined 0.15% to 88.75 as copper fell 3.01% to 6.16, weighing on mining-exposed equities.

USD/CLP rose 0.56% to 906.24 and USD/PEN jumped 2.16% to 3.38 amid the broader commodity sell-off. Gold declined 0.91% to 4,143.80 while Brent crude held near flat at 77.94, offering little offset for Colombia’s oil-linked revenues. No Tier-1 data releases occurred across the three countries.

Bitcoin fell 2.50% to 62,354.07, adding to risk-off sentiment in the region.

The Day Ahead

Markets will focus on post-election positioning in Colombia with no major data releases scheduled. Investors await any early signals from the incoming administration on fiscal and regulatory policy. BCCh and BCRP face continued commodity volatility that could shape near-term rate decisions.

Global USD moves driven by external central-bank commentary may pressure CLP and PEN further. Attention also turns to any certification updates on the Colombian vote count that could affect sovereign spreads.

Other Economic Notes

Persistent copper weakness threatens to widen Chile’s and Peru’s current-account gaps and slow royalty inflows. Colombia’s stronger COP and pro-market election result improve near-term fiscal optics and reduce external financing risks. The 14.50% ECB deposit rate keeps global rate differentials elevated, sustaining pressure on emerging-market currencies.

Eurozone unemployment at 6.70% points to subdued external demand that could cap Andean export growth.

Global Macro News

Global risk sentiment softened on mixed commodity and equity moves that spilled into Andean assets. The eurozone’s high policy rate continues to anchor USD strength and weigh on PEN and CLP. <i>↓ p.2</i>