Andeans Macro Daily(Beta Mode)

Copper Drop Hits Chile, Peru; COP Gains

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

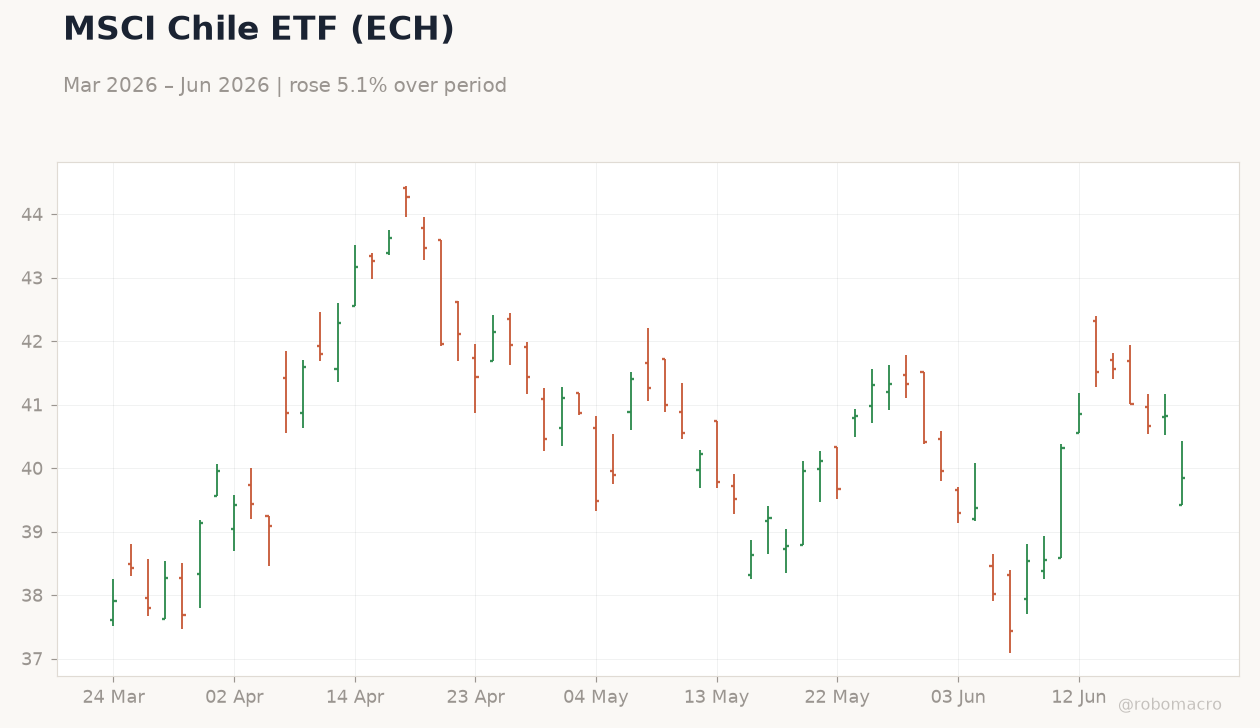

| MSCI Chile | 40.99 | -0.05% |

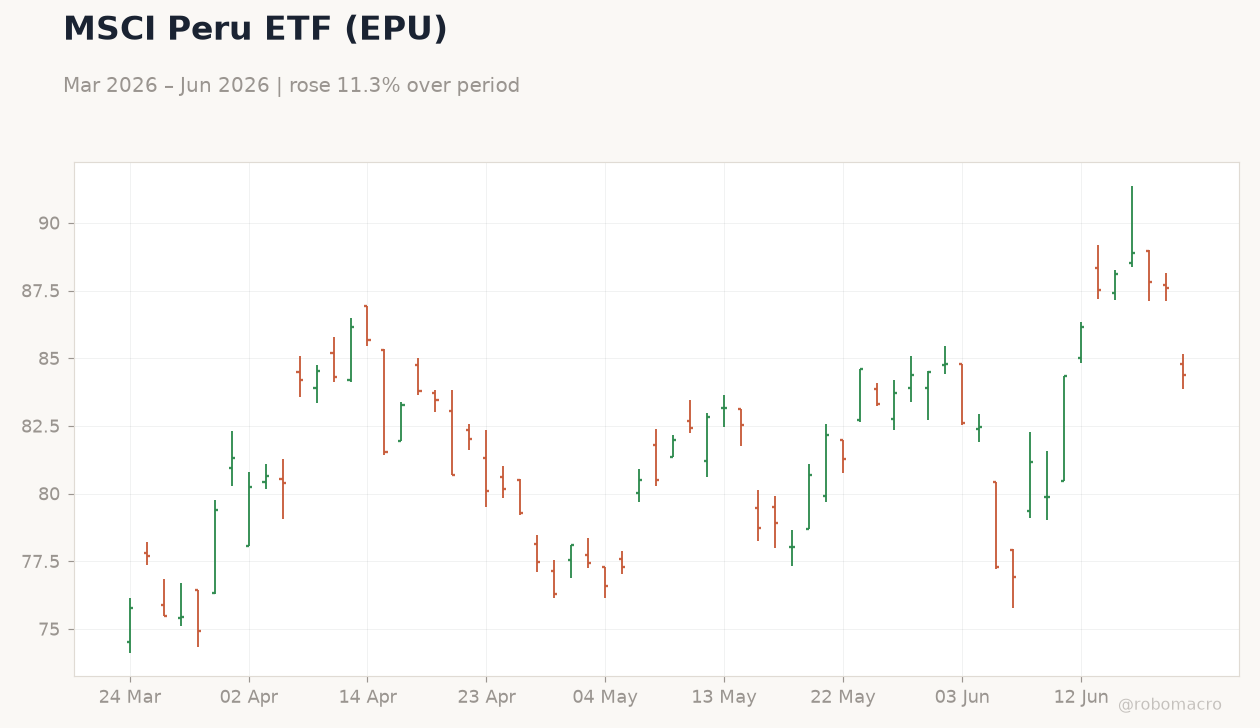

| MSCI Peru | 88.75 | -0.15% |

| USD/COP | 3,413.16 | -0.88% |

| USD/CLP | 913.39 | +0.82% |

| USD/PEN | 3.39 | +0.24% |

| Copper | 6.06 | -1.27% |

| Gold | 4,066.20 | -1.54% |

| Brent Crude | 75.63 | -1.88% |

| Bitcoin | 62,269.66 | -0.64% |

| Colombia 10Y Govt Yield | - | - |

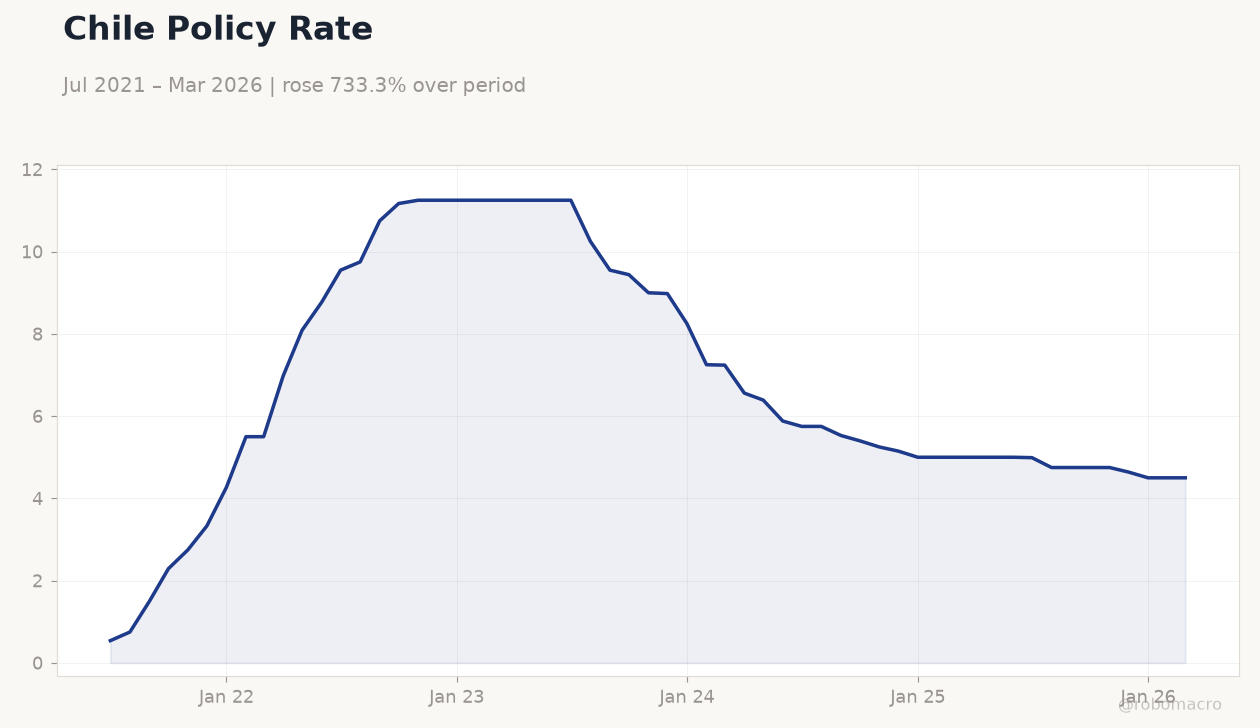

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Policy Rate | Type: macro_line | Rate %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Chile Policy Rate | Type: macro_line | Rate %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI Chile and Peru edge lower as copper falls 1.27% to $6.06/lb

- Colombian peso gains 0.88% to 3,413.16 per dollar on political stability hopes

- No major economic releases reported across Colombia, Chile or Peru yesterday

Yesterday's Recap

Andean equity markets posted modest declines, with MSCI Chile falling 0.05% to 40.99 and MSCI Peru slipping 0.15% to 88.75 amid weaker copper prices. MSCI Colombia held steady at 9.02. The Colombian peso outperformed regional peers, strengthening 0.88% as USD/COP dropped to 3,413.16, while USD/CLP rose 0.82% to 913.39 and USD/PEN gained 0.24% to 3.39.

Preliminary election results pointing to Abelardo de la Espriella as Colombia’s next president, backed by U.S. support, supported local assets. Brent crude declined 1.88% to $75.63/bbl, limiting fiscal upside for Colombia’s energy sector, while gold fell 1.54% to $4,066.20/oz.

Chile’s short-term rate remained unchanged at 4.50%. Overall regional moves reflected commodity sensitivity rather than domestic data surprises.

The Day Ahead

Markets face a quiet session with no major Andean data releases scheduled. Investors will monitor global copper and oil price action for direction on Chile and Colombia. Colombian 10-year TES yields may see limited movement absent fresh supply.

Peru’s sol could remain range-bound near 3.39 per dollar given stable fundamentals. Broader sentiment will hinge on U.S. dollar strength and any China demand signals affecting mining revenues.

Other Economic Notes

Copper’s 1.27% decline trims near-term fiscal revenue projections for both Chile and Peru through lower royalties. Colombia’s external accounts benefit from peso strength, narrowing the current-account gap. Regional equity underperformance versus global benchmarks highlights ongoing commodity beta.

Lithium price stability continues to support Chile’s longer-term export outlook despite flat volumes at major producers.

Global Macro News

Global commodity markets weighed on Andean currencies and equities as risk sentiment softened. A stronger U.S. dollar pressured emerging-market flows, with the peso’s outperformance standing out.

Brent’s 1.88% drop reduced Colombia’s oil-linked fiscal buffer. Copper weakness signals softer Chinese industrial demand, directly hitting Chile’s terms of trade. <i>↓ p.2</i>