Andeans Macro Daily(Beta Mode)

Copper Rally Lifts Chile; Peru Equities Slide

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 39.87 | +0.04% |

| MSCI Peru | 83.24 | -1.34% |

| USD/COP | 3,426.31 | -0.08% |

| USD/CLP | 919.04 | +0.61% |

| USD/PEN | 3.42 | +3.01% |

| Copper | 6.09 | +2.39% |

| Gold | 3,998.80 | +0.21% |

| Brent Crude | 72.89 | -1.15% |

| Bitcoin | 61,266.39 | +0.44% |

| Colombia 10Y Govt Yield | - | - |

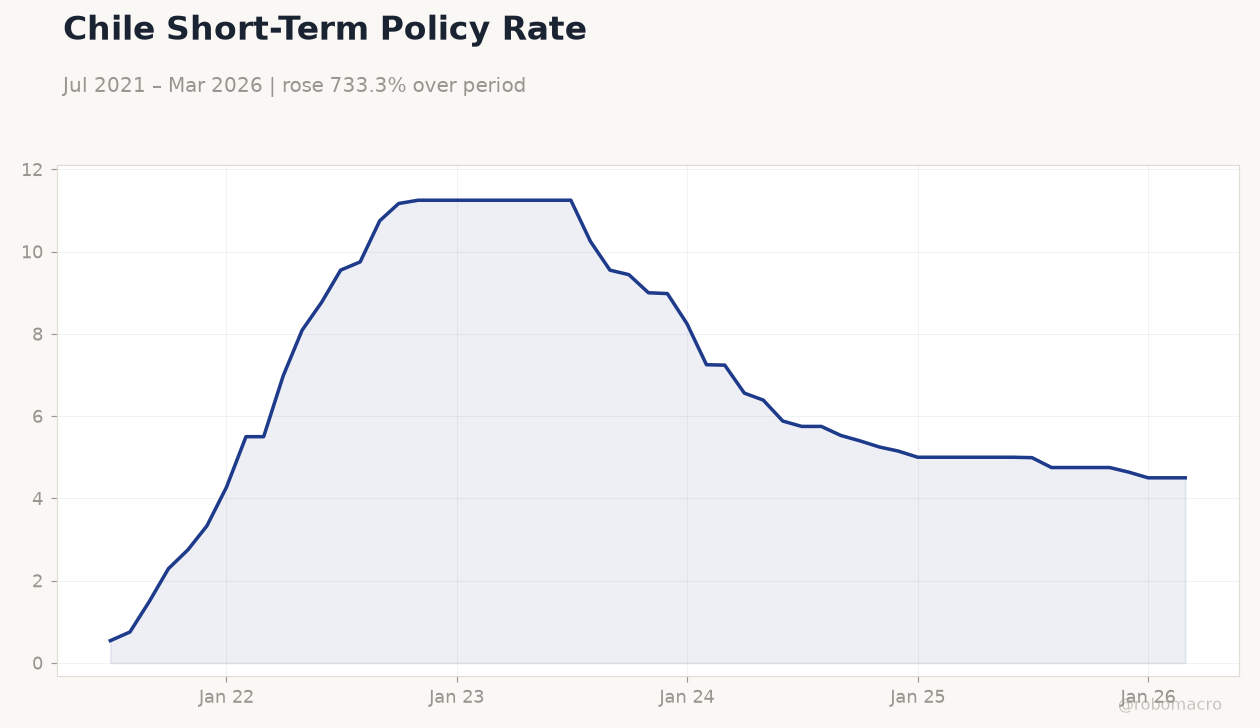

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Short-Term Policy Rate | Type: macro_line | %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Chile Short-Term Policy Rate | Type: macro_line | %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI Chile edges up 0.04% as copper jumps 2.39% to $6.09/lb.

- USD/PEN surges 3.01% while USD/CLP rises 0.61% on mixed commodity flows.

- Colombia’s right-wing victory reduces political risk premium for COP.

Yesterday's Recap

MSCI Peru fell 1.34% to 83.24 amid broad regional equity weakness despite higher copper prices. USD/COP eased 0.08% to 3,426.31 as markets digested Abelardo de la Espriella’s razor-thin election win and the concession by leftist Iván Cepeda. Chile’s short-term rate held at 4.50% with no change signaled.

Brent crude slipped 1.15% to $72.89, offering limited fiscal relief for Colombia. Gold rose modestly to $3,998.80, providing minor support to Peruvian and Colombian mining output. Overall Andean FX showed CLP and PEN under pressure while COP proved more resilient on the political outcome.

MSCI Colombia was flat at 9.02. Bitcoin added 0.44% to 61,266.39 with negligible regional impact. No economic releases occurred across the three markets.

The Day Ahead

Markets enter a data-light session with no major Andean releases scheduled. Focus remains on follow-through in copper after the sharp advance and any early signals from incoming Colombian policymakers. Chile’s mining sector will monitor Codelco production updates for fiscal revenue implications.

Peru’s trade balance trajectory may draw attention given recent PEN volatility. Traders will also watch for any BanRep or BCRP commentary on reserve management. Brent near $73 keeps Colombian fiscal sensitivity elevated while copper strength supports Chile and Peru external accounts.

Other Economic Notes

Elevated copper prices continue to underpin Chile’s external accounts and fiscal copper receipts. Peru’s mining export volumes remain a key swing factor for the trade surplus and PEN stability. Colombia’s fiscal outlook stays sensitive to Brent levels near $73 despite the political shift.

Regional equity performance diverged sharply, highlighting commodity differentiation across the three economies. Chile short-term rate stability at 4.50% leaves room for later easing if inflation moderates further.

Global Macro News

Stronger copper readings reflect ongoing Chinese demand signals that benefit Chile and Peru disproportionately. Brent weakness caps upside for Colombian fiscal balances and Ecopetrol dividends. <i>↓ p.2</i>